Taxation Law Assignment Analyze & Synthesize Complex Tax Law Issues

Question

Task:

The questions to be answered through this taxation law assignmentare:

Question 1: John is a sole trader working in his small business as a carpenter. His brother Paul is mentally disabled, who lives with John and is receiving disability support pension.

Required:

Work out John’s invalid tax offset for his brother Paul who is an invalid under the following three scenarios:

Scenario 1 - John has $120,000 taxable income in the 2018-2019 financial year from his small business. Paul has $4,000 as an adjusted taxable income.

Scenario 2 - John has adjusted taxable income of $63,000. Paul has adjusted taxable income of $900.

Scenario 3 - John has an adjusted taxable income of $41,000. Paul was severely sick this year and had zero adjusted taxable income.

Question 2: Oliver wanted to repay his loan of $12,000, which he borrowed from National Australia Bank (NAB). He approached his employer on 4th October 2019 and received $12,000 from him at no interest. On 15th February 2020, Oliver had a performance review with his employer when they told him that he was only required to repay half of the loan as he is a good performing employee.

Required:

With reference to the relevant laws, advise Oliver and his employer of the tax consequences of this transaction.

Question 3: David and Emma are married and have some investment properties jointly in Sydney. To structurally manage their investment properties, they signed a formal partnership agreement, and agreed that the net profits from their rental properties would be distributed 95% to Emma and 5% to David. They also agreed that David bear the total losses from the investments.

Required:

With reference to the relevant laws, critically discuss whether David and Emma are in a partnership as investors Also, discuss whether they are required to lodge a partnership tax return

Question 4: Anna works for the Eastern Medical Centre as admin officer with a marginal tax rate of 47%. She has just turned 48 in June 2020. Eastern Medical Centre contributed $13,000 under the Superannuation Guarantee Charge. Anna entered into a salary sacrifice agreement with Eastern Medical Centre to sacrifice 10% of her salary into her Superannuation fund. This extra contribution has resulted in an additional contribution of $17,000 for the current income year.

Required:

With reference to the relevant laws, discuss the effect of these arrangements for both Anna and the Eastern Medical Centre. Determine the total tax levied on the contributions to Anna's superannuation fund and the tax effect on Anna's employer.

Question 5: Darryl Kerrigan is the director of DK Pty Ltd, which is a property investment company in Sydney and the company is registered for Goods and Services Tax (GST). Due to the COVID-19 impact, DK Pty Ltd has decided to rent out their twenty (20) existing office units that they finished in a building project in February 2020.

To negotiate rental contracts, DK Pty Ltd employs a property lawyer, Mr. Dennis Denuto. Dennis is a busy lawyer and his practice income is $300,000 per year. DK Pty Ltd offered Dennis a rent-free office in the city of Sydney in exchange for his service to DK Pty Ltd. The market rental value of the office provided to Dennis is $38,000 per year.

Required:

Advise of the GST obligations and the input tax credit of this arrangement to DK Pty Ltd and Mr. Dennis Denuto.

Answer

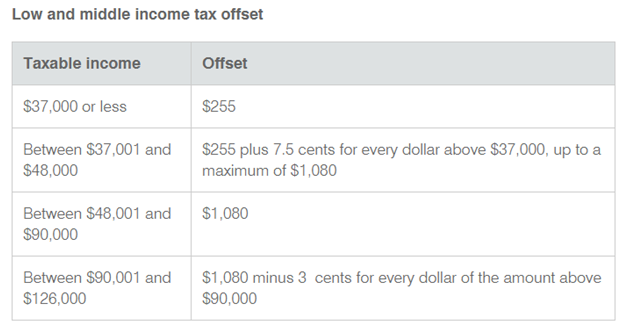

A1:According to the rules of ATO and ITAA 1997 undertaken in this taxation law assignment, it has been identified that the income test of an individual is an important matter for evaluating tax offsets and other benefits. According to the ITAA 1997, it is found that a disabled person or an individual who cares a disable person is eligible for certain tax offsets (Low and middle-income earners, 2020). In this case, the invalid tax offset can be availed by a disabled person or a carer of a disabled individual. According to scenario 1, John would avail tax offset based on taxable income during 2018-19. As the income of John is between 37001 to 126000 AUD, low and middle both invalid tax offset can be availed. Scenario 2 and 3 reveals adjusted taxable income of John and it is considered for identifying dependant tax offset.

Scenario 1: the tax offset amount = 1080 AUD + 30000*.03 = 1080 AUD - 900 AUD =180 AUD (Income slab between 90001 to 126000 AUD)

Scenario 2: tax offset = 1080 AUD (Income between 48001 AUD to 90000 AUD)

Scenario 3: tax offset = 255 AUD + 4000*0.075 = (255 + 300) AUD = 555 AUD

Hence, total invalid tax offset of John for his brother = (180 + 1080 + 555) AUD = 1815 AUD

A2: The tax has not been charged according to the rules of ATO on the borrower for the loan amount unless the money has been used in personal purpose. However, if the loan amount has been used to increase debt amount of an individual, it is needed to be shown in the income tax return. The employer of Oliver is liable to pay tax on interest amount while the interest would be received. The exemption can be availed by employer 50% of the aggregate loan amount as it is intimated to Oliver that 50% interest on the loan amount is needed to pay. Hence, according to the section 25.25 of ITAA 1997, it is identified that borrowed money can be deducted from the assessable income if that has a relationship with the taxable income of an individual (Income tax assessment act 1997 - sect 25.25, 2020). Hence, it is completely clear from the case of Oliver that employee of Oliver can avail tax exemption on the 50% interest amount and the balance interest, the tax payment is mandatory while the interest amount would be received actually. On the other hand, Oliver has to produce evidence to the ATO that the loan has been taken for income generation and it has no relationship with the personal requirements. If that has been lodged, Oliver can get exemption of the amount and section 25.25 is applicable in this case. If the loan is a personal loan, Oliver is liable to pay tax on aggregate loan amount based on the rules of ATO. In this case, Oliver and her employer both have to produce proper evidence to provide information regarding the loan amount to ATO.

A3: Based on the Tax Ruling 93/32, it has been identified that net rental income or losses of co-owners of investment properties would be distributed according to the agreement among the co-owners (Ato.gov.au, 2019). The case reveals that the net profit from the rental property would be distributed between Emma and David at 95:5 or 19:1. As David and Emma are entered into a partnership agreement, it is mandatory to focus on the rental loss amount as it can be claimed as deduction according to o ITAA 1997. According to the partnership taxation rules of ATO, it has been identified that the following conditions are fulfilled in the current case.

• Rent would be received from jointly owned investment properties in Sydney

• Interest would be received from a jointly held account

Based on the analysis of the above conditions, it can be stated that David and Emma are in a Partnership as investors. According to the ATO regulations, an individual does not need to lodge a return id partnership business is not carried on. On the other hand, in the case of the partnership business, it is mandatory to lodge a partnership tax return to the tax authority.

A4: Based on the case, it can be stated that Anna’ employer Eastern Medical Centre has paid 13000 AUD under the Superannuation Guarantee Charges. It has been paid as the employer did not contribute to the superannuation fund on behalf of Anna. The section 291-25 of the Income Tax Assessment Act 1997 deals with the taxability on superannuation fund. Based on this section, the superannuation charge is not tax-deductible in the hands of an employer as it has been paid as a penalty (Taxation of excess contributions learner guide, 2020). However, a statement regarding SGC is needed to be lodged to the Australian Taxation Authority. Hence, Eastern Medical Centre has no tax liability for the relevant tax year. On the other hand, aggregate superannuation fund contribution of Anna is 17000 AUD + 13000 AUD = 30000 AUD. The 17000 AUD amount is 10% salary sacrifice of Anna for the current income year. Hence, the tax rate that would be charged on 30000 AUD is 15% and the amount is needed to be paid by Anna to ATO in the current income year. Hence, it is identified that SGC is not taxable in the hands of Eastern Medical Centre; it is taxable only in the hands of the employee.

A5: According to the case, it has been identified that Darryl Kerrigan has decided to rent out his existing office units as a result of COVID 19 situation. The Goods and Service Tax Act 1999 in Australia reveals that any residential rent is not taxable under the GST Act. However, the commercial rent is taxable according to the GST Act 1999 at a 10% rate in Australia. The case reveals that the property would be used for commercial purpose and hence, the commercial rent is taxable in the hands of Kerrigan. According to the case, it is also identified that Kerrigan has offered a rent-free property to his lawyer Dennis Denuto for providing legal services. In this context, it can be said that the rent-free property is not taxable under the GST Act 1999. The market rental value of the property provided to Dennis is 38000 AUD per year. However, the GST is payable only on the commercial rent that has been received by Kerrigan in a particular income year. On the other hand, the lawyer is liable to pay tax on the professional service that has been provided to Kerrigan. The GST registration is mandatory according to the Act for an organization or an individual having a yearly turnover of 75000 AUD. Hence, in the case of a lawyer, annual income has been mentioned in the case 300000 AUD and he is liable to pay tax on professional service.

According to paragraph 33-15(1)(b) of the GST Act 1999, it has been identified that input tax credit is available in the year in which the GST liability is created. The GST legislation states that input tax credit can be availed if an individual or an organisation considers the creditable acquisition process (A New Tax System GST Act 1999, 2020). Based on the case, it is found that properties are build by Kerrigan considering a creditable acquisition. Hence, he can avail input tax credit on GST payment if eligibility is fulfilled according to the rule. Office units are used for commercial purposes and hence creditable purpose exists here. On the other hand, in the case of Mr Dennis, it is identified that no question would arise regarding input tax credit. This is because he is only liable to pay tax on his professional service Kerrigan and he does not pay any rent to the client.

References

A New Tax System GST Act 1999, 2020. Available at:

https://www.legislation.gov.au/Details/C2014C00008 (Accessed: 26 June 2020).

Ato.gov.au 2019, Ato.gov.au. Available at: https://www.ato.gov.au/uploadedFiles/Content/IND/downloads/Rental-properties-2019.pdf (Accessed: 26 June 2020).

Income tax assessment act 1997 - sect 25.25 Borrowing expenses, 2020. Available at: http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s25.25.html (Accessed: 26 June 2020).

Low and middle-income earners, 2020.Taxation law assignment Available at: https://www.ato.gov.au/Individuals/Income-and-deductions/Offsets-and-rebates/Low-and-middle-income-earners/ (Accessed: 26 June 2020).

Taxation of excess contributions learner guide, 2020. Available at: https://www.ato.gov.au/Super/APRA-regulated-funds/In-detail/APRA-resources/Learner-guides/Taxation-of-excess-contributions-learner-guide-(from-1-July-2013-to-30-June-2017)/page=2#:~:text=Concessional%20contributions%20are%20defined%20in,income%20of%20the%20super%20fund.&text=certain%20amounts%20transferred%20from%20a,to%20an%20Australian%20super%20fund. (Accessed: 26 June 2020).

Appendices

Appendix 1:

Tax Offset related to Question 1

(Source: Low and middle-income earners, 2020)