Stott’s Pty Ltd Case Study Critically Analysing The Financial Management

Question

Task: Project Instructions

For this assessment you are required to:

Complete Project Tasks One/Two

|

Project -Task One - Part A |

|

Read and analyse the case study information (including business plan summary and previous financial data) in Appendices 1–3 and complete the following tasks: · Develop a sales budget, profit budget, cash flow budget and debtor ageing summary by using electronic spreadsheets (as separate worksheets) making sure each budget is divided into quarterly periods and that you use previous financial data to determine allocations for resources. (You can use the templates as designed in the Project) Ensure each budget you prepare complies with the organisational policies and procedures as provided. · Develop budget notes that include: i. identification of reasons for previous profits and losses ii. your comment on the effectiveness of existing financial management approaches iii. all assumptions and bases that have been made or used to form budgets iv. any relevant notes regarding implementation and monitoring of budget expenditure v. an explanation of the required legislative requirements of financial management (and outline statutory requirements of ATO, GST, company tax, PAYG) vi. review of two types of digital technology that can be used for financial management. Make a recommendation in the budget notes as to which you would suggest using for the case study. |

|

Evidence Required to Submit |

|

1. A completed annual budget in a single spread sheet (MS-Office Excel) with a separate sheet for each budget component (use the templates supplied) 2. All budget notes and assumptions |

|

Project - Task One – Part B |

|

Communicate information regarding the budget and answer a series of eight questions (see Appendix 3) in written form as agreed with your assessor |

|

Evidence Required to Submit |

|

8 question answers in a written format (Appendix 3) |

|

Project – Task Two |

|

You will need to review the provided current case study information and compare it to the budget you established in Part A. After evaluating these you will need to report on the following: Significant issues Variances from budget Comparative performances Recommendations for ongoing financial viability Evaluation of financial management processes. Follow the Procedures below: 1. Read the case study provided in this task. 2. Develop an actual to budget variance report based on the format and template provided by Stott’s. 3. Complete a cash flow analysis on the average length of time it takes Stott’s to collect funds from its debtors to determine the trend based on the financial reports in Project (Section A). 4. Examine the sales budget, profit budget, cash flow budget and debtor ageing summary to identify the following in a report: a. Issues: i. Identify, describe and prioritise significant issues that are evidenced in Stott’s College Pty Ltd information and describe reasons or causes of these issues. Include in this issue of financial probability that you have identified or considered when monitoring these budgets. b. Variances: i. Complete an actual-to-budget variance report, using the template provided in the case study. ii. Identify variances by comparing actual results with the established budget and provide reasons why these variances may have occurred. c. Performance: i. Compare financial performance of the organisation (according to financial information provided) to industry benchmarks for this organisation in line with the retail trade sector. ii. Respond to the performance questions provided by the CEO, as provided by the board of Stott’s, iii. Determine a trend of the average debtor days and the impact to the cash flow of Stott’s. d. Recommendations: i. Outline your recommendations for ongoing financial viability for the organisation, based on your assessment of the issues, reasons for variances and organisational performance you have identified (Steps 1–3). ii. Include in this section your plans for a revised budget, effectively managing contingencies and issues that have been identified in feedback and monitoring of the budgets. e. Evaluation: i. Provide a summary review of the financial management processes in place for the organisation, in light of your assessment of the issues, reasons for variances and organisational performance you have identified. Include in this section any recommendations you have for modifying management processes. ii. analyse the effectiveness of existing financial management approaches including reviewing financial management software, managing risks of misappropriation of funds, ensuring systems are in place to record all transactions, maintaining an audit trail and complying with due diligence |

|

Evidence Required to Submit |

|

· a complete actual-to-budget variance report detailing the issues, variances, performance, recommendations and evaluations identified from the financial information for Stott’s Pty Ltd. (1500 - 2000Words) |

Answer

Project Task One: Part A

Developing different budgets

Sales Budget based on the Stott’s Pty Ltd case study

|

AGED DEBTORS BUDGET |

TOTAL |

Qtr 1 |

Qtr 2 |

Qtr 3 |

Qtr 4 |

|

Sales |

33,71,200 |

37,71,386 |

40,85,668 |

47,14,232 |

|

|

% Debtors Sales |

22% |

22% |

22% |

22% |

|

|

Total Debtors |

7,41,664 |

829704.92 |

898846.96 |

1037131.04 |

|

|

Current |

5,85,915 |

5,85,915 |

585915 |

585915 |

|

|

30 Days |

1,11,250 |

2,43,790 |

312931.96 |

451216.04 |

|

|

60 Days |

37,083 |

3,42,125 |

272983.04 |

134698.96 |

|

|

90 Days |

7,417 |

98,335 |

39948.92 |

316517.08 |

|

|

Total Debtors |

7,41,664 |

829704.92 |

898846.96 |

1037131.04 |

|

|

Stott’s Pty Ltd |

|||||

|

Actual Results |

Qtr 1 |

Qtr 2 |

Qtr 3 |

Qtr 4 |

|

|

Revenue |

|||||

|

Sales |

33,71,200 |

37,71,386 |

40,85,668 |

47,14,232 |

|

|

– Cost Of Goods Sold |

19,55,296 |

1783834.3 |

17,83,834 |

17,83,834 |

|

|

Gross Profit |

14,15,904 |

19,87,552 |

23,01,834 |

29,30,398 |

|

|

Gross Profit % |

42% |

53% |

1 |

1 |

|

|

Expenses |

0 |

0 |

|||

|

– Accounting Fees |

2,500 |

2500 |

0 |

0 |

|

|

– Interest Expense |

28,150 |

21127 |

21,127 |

21,127 |

|

|

– Bank Charges |

380 |

400 |

400 |

400 |

|

|

– Depreciation |

42,500 |

2500 |

2,500 |

2,500 |

|

|

– Insurance |

3,348 |

3347.5 |

3,348 |

3,348 |

|

|

– Store Supplies |

790 |

0 |

0 |

0 |

|

|

– Advertising |

1,50,000 |

0 |

0 |

0 |

|

|

– Cleaning |

3,325 |

4815.25 |

4,815 |

4,815 |

|

|

– Repairs & Maintenance |

16,150 |

16068 |

16,068 |

16,068 |

|

|

– Rent |

6,60,127 |

660127 |

6,60,127 |

6,60,127 |

|

|

– Telephone |

3,100 |

3749.2 |

3,749 |

3,749 |

|

|

– Electricity Expense |

5,245 |

6695 |

6,695 |

6,695 |

|

|

– Luxury Car Tax |

12,000 |

3224 |

3,224 |

3,224 |

|

|

– Fringe Benefits Tax |

7,000 |

7000 |

7,000 |

7,000 |

|

|

– Superannuation |

37,404 |

521630.63 |

5,21,631 |

5,21,631 |

|

|

– Wages & Salaries |

4,10,500 |

476375 |

4,76,375 |

4,76,375 |

|

|

– Payroll Tax |

19,741 |

499002.81 |

4,99,003 |

4,99,003 |

|

|

– Workers’ Compensation |

8,312 |

485902.5 |

4,85,903 |

4,85,903 |

|

|

Total Expenses |

14,10,572 |

2711963.9 |

27,11,964 |

27,11,964 |

|

|

Net Profit (before tax) |

5,333 |

724412.15 |

4,10,130 |

-2,18,434 |

|

|

Income Tax |

1,600 |

217323.64 |

1,23,039 |

-65,530 |

|

|

Net Profit |

3,733 |

507088.5 |

2,87,091 |

-1,52,904 |

|

Table 1: Sales budget of the company examined in the Stott’s Pty Ltd case study

(Source: Created by me)

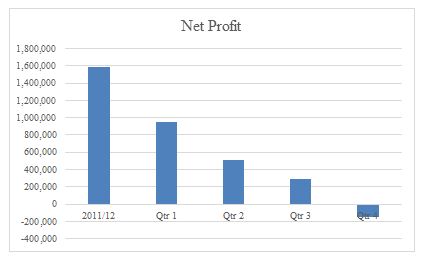

Profit Budget

|

PROFIT BUDGET |

2011/12 |

Qtr 1 |

Qtr 2 |

Qtr 3 |

Qtr 4 |

|

Revenue |

|||||

|

Sales |

31,42,822 |

37,71,386 |

40,85,668 |

47,14,232 |

|

|

– Cost of Goods Sold |

7135337.04 |

1783834.26 |

1783834.26 |

1783834.26 |

1783834.26 |

|

Gross Profit |

85,78,771 |

13,58,988 |

19,87,552 |

23,01,834 |

29,30,398 |

|

Gross Profit % |

43% |

53% |

56% |

62% |

|

|

Expenses |

|||||

|

– Accounting Fees |

|||||

|

– Interest Expense |

84,508 |

21127 |

21127 |

21127 |

21127 |

|

– Bank Charges |

1,600 |

400 |

400 |

400 |

400 |

|

– Depreciation |

10000 |

2500 |

2500 |

2500 |

2500 |

|

– Insurance |

13390 |

3347.5 |

3347.5 |

3347.5 |

3347.5 |

|

– Store Supplies |

|||||

|

– Advertising |

|||||

|

– Cleaning |

19,261 |

4815.25 |

4815.25 |

4815.25 |

4815.25 |

|

– Repairs & Maintenance |

64,272 |

16068 |

16068 |

16068 |

16068 |

|

– Rent |

2640508 |

660127 |

660127 |

660127 |

660127 |

|

– Telephone |

14996.8 |

3749.2 |

3749.2 |

3749.2 |

3749.2 |

|

– Electricity Expense |

26780 |

6695 |

6695 |

6695 |

6695 |

|

– Luxury Car Tax |

12896 |

3224 |

3224 |

3224 |

3224 |

|

– Fringe Benefits Tax |

28,000 |

7000 |

7000 |

7000 |

7000 |

|

– Superannuation |

521630.625 |

521630.625 |

521630.625 |

521630.625 |

|

|

– Wages & Salaries |

19,05,500 |

476375 |

476375 |

476375 |

476375 |

|

– Payroll Tax |

499002.81 |

499002.81 |

499002.81 |

499002.81 |

|

|

– Workers’ Compensation |

485902.5 |

485902.5 |

485902.5 |

485902.5 |

|

|

Total Expenses |

10847855.6 |

2711963.888 |

2711963.888 |

2711963.888 |

2711963.888 |

|

Net Profit (Before Tax) |

22,69,085 |

13,52,976 |

7,24,412 |

4,10,130 |

-2,18,434 |

|

Income Tax |

680725.377 |

405892.8443 |

217323.6443 |

123039.0443 |

-65530.1558 |

|

Net Profit |

15,88,359 |

9,47,083 |

5,07,089 |

2,87,091 |

-1,52,904 |

Table 2: Profit Budget

(Source: Created by me)

GST Cash Flow budget

|

CASH FLOW ANALYSIS – GST |

2011/12 |

Qtr 1 |

Qtr 2 |

Qtr 3 |

Qtr 4 |

|

GST Collected |

3,37,120 |

377138.60 |

408566.8 |

471423.2 |

|

|

Less GST Paid |

2,79,988 |

271196.389 |

271196.389 |

271196.39 |

|

|

GST Payable |

57,132 |

105942.21 |

137370.411 |

200226.81 |

Table 3: GST Cash flow Budget

(Source: Created by me)

Debtors Ageing

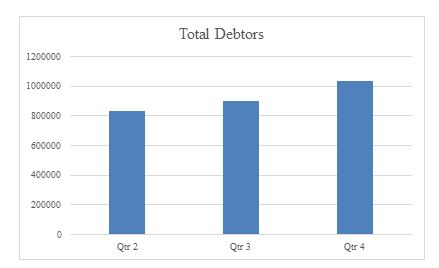

|

AGED DEBTORS BUDGET |

TOTAL |

Qtr. 1 |

Qtr. 2 |

Qtr. 3 |

Qtr. 4 |

|

Sales |

33,71,200 |

37,71,386 |

40,85,668 |

47,14,232 |

|

|

% Debtors Sales |

22% |

22% |

22% |

22% |

|

|

Total Debtors |

7,41,664 |

829704.92 |

898846.96 |

1037131.04 |

|

|

Current |

5,85,915 |

5,85,915 |

585915 |

585915 |

|

|

30 Days |

1,11,250 |

2,43,790 |

312931.96 |

451216.04 |

|

|

60 Days |

37,083 |

3,42,125 |

272983.04 |

134698.96 |

|

|

90 Days |

7,417 |

98,335 |

39948.92 |

316517.08 |

|

|

Total Debtors |

7,41,664 |

829704.92 |

898846.96 |

1037131.04 |

Table 4: Debtors Ageing

(Source: Created by me)

Developing budget notes

Identification of reasons for previous profits and losses

It can be seen in the Stott’s Pty Ltd case study that the entire profit and loss for the year is divided into four quarters. In the last quarter the net profit has become negative in the company. It shows that the budget of the last period is not much effective for the company.

The net profit obtained in the Stott’s Pty Ltd case study for each quarter is 3,733, 507088.5, 2,87,091, -1,52,904 and it denotes that the assumptions of fourth quarter is not properly fit in the situation. Cost of the company should be reduced to increase the profit. The reasons of loss are equal division of the costing in four quarters.

The costing is increasing but the sales have not been assumed to increase. It is the main reason for the company to acquire losses in the last quarter. This budget is not much favourable for the company examined in the Stott’s Pty Ltd case study and the costing should be managed more effectively. As the rate of inflation is considered high, the sales should be assumed to be higher in order to cover up the entre costing by the company. In the other quarters, the company has got profit as the expenses have been covered up but the expenses were increasing with every quarter and it is the most important reason for the company to acquire loss.

Comment on the effectiveness of existing financial management approaches within this Stott’s Pty Ltd case study

Existing financial management approach explored in the Stott’s Pty Ltd case study is capable enough to calculate the budgets in different forms but the process is time consuming. Chances of doing mistakes in between the calculation are high for the employees of the company. These limitations of the existing methods of financial management making the process in—effective for the company. Though this process is effective for understanding the entire methods of the budgeting and calculation easier and it can help the management to understand easily still the process is highly time-consuming and it is not possible for the employees to provide so much time for preparing budget. Using modern technology can help the company to adapt more effective systems for budgeting and financial management.

Assumptions and bases that have been made or used to form budgets

The assumptions of sales of the budget have been assumed to be the same as the last year. The cost allotted for every quarter in this Stott’s Pty Ltd case study is 14,10,572, 2711963.9, 27,11,964, 27,11,964 and it denotes that cost should be reduced to manage the profitability of the company. Mostly the expenses and the income of the budget are equally divided in four quarters. Inflation is assumed to be 23% in next year which is a high rate and the expenses will increase due to the high inflation. The Board reviewed and approved the business plan that covered the budget year to highlight some of the key goals.

As per the research carried on this Stott’s Pty Ltd case study, it is noted that in 2010/2011 the Stott’s Pty Ltd considered the number of the previous year’s profits which should be retained for the maintenance and development of Stott’s Pty Ltd’s business and the amount which could be distributed to Partners as Stott’s Pty Ltd Bonus. The Stott’s Pty Ltd decided that the expectation that 2011/12 would be a difficult trading year but that the budget net profit should target the same result as achieved in the 2010/11. The value used in the calculation within this Stott’s Pty Ltd case study is based on three-year cash flow projections using the latest budget and forecast data. Any changes in sales performance and costs are based on experience and expectations of future changes in the market. The forecasts are then extrapolated beyond the three years using a long-term growth rate. The discount rate is derived from the Partnership’s pre-tax weighted average cost of capital of 8% (2011: 8%)

Relevant notes regarding implementation and monitoring of budget expenditure

Before implementing the budget within this Stott’s Pty Ltd case study, new strategies should be implemented in the company tom increase the sales. Otherwise, the company will run in loss after the fourth quarter. Otherwise, the expenditure of the budget should be revised once again and it must be reduced in order to gain profit at the same amount of sales. Total amount of debt should be reduced to make more assets and the current budget should be revised accordingly to make profit. Assumption of expenditure is very high with compared to the assumptions of sales of the company in four quarters. It is the main fault observed in the context of this Stott’s Pty Ltd case study within the current budget of the company that needs to be improved using different strategies.

Explanation of the required legislative requirements of financial management (and outline statutory requirements of ATO, GST, company tax, PAYG)

Corporations Act 2001 is the main legislation that needs to be followed for the financial management of the company within this Stott’s Pty Ltd case study. This Act has been compiled on 18th June 2013 (Legislation.gov.au. 2019). All the amendments in the reports of the company should be done as per maintaining the rules of this act. Total sale declined by 3.2% to $3,100.6 million, and were down 2.7% on a similar stores premise. Pleasingly, all out online deals came to $239.4 million. Working gross benefit (OGP) declined by 2.9% to $1,184.4 million, and OGP edge expanded to 38.2%. Rate of Goods and Service Tax is 10% on the services and goods traded within the country. Corporate tax is considered as one of the strongest pillars of the economy and the rate of corporate tax in the country is 30%.

Statutory requirement of Australian Taxation Office is to submit the activity statements of the businesses in three phases in a year that is quarterly, monthly and annually. The activity statement submission of the businesses is needed to pay goods and services tax in the company. Pay as you go instalments can be fulfilled using the activity statements of the businesses (Smallbusiness.wa.gov.au. 2019). The businesses that are registered under GST, should definitely submit its activity statement within proper intervals.

Review of two types of digital technology that can be used for financial management within this Stott’s Pty Ltd case study

XERO

Xero is a strong accounting arrangement with complex bookkeeping highlights, plentiful reports, 700+ reconciliations, and boundless clients. Dissimilar to QuickBooks, Xero additionally has the versatility and present-day UI of cloud-based programming. The product has more than 1,000,000 clients and is the essential bookkeeping answer for more than 16,000 bookkeeping firms. The organization has as of late included a venture the board highlight, which was probably the greatest downside beforehand. It’s an web based solution which is allowing the advance features of accessing this accounting application from anywhere as well as any devices. It is used for invoicing, fulfilling accounts payable, bank feeds, calculating depreciation, bank reconciliation, adjustment of inventory and other accounting processes.

MYOB

The investigation on Stott’s Pty Ltd case study demonstrates that MYOB Essentials is an online accounting application that allows the business organizations for tax management, invoicing, finance, costs and detailing. Through MOYB, organisation can download the MYOB OnTheGo application for Android and iOS gadgets. MYOB enables the users to view income and oversee finance, and entrepreneurs by connecting store bills and solicitations with the suitable records. It is one of the best financial payroll modules that stores employee information that allows business firm to manage their payrolls easily.

From the overall analysis done in the Stott’s Pty Ltd case study, it can be recommended for the company that Xero can be replaced with MYOB to increase the effectiveness of the company and financial management. Chances of internal mistakes will be less that will be highly beneficial for the company.

Project Task One: Part Two

What are the statutory requirements for tax compliance in the context of this Stott’s Pty Ltd case study?

There are certain statutory requirements for tax compliance that are present for any organisation situated in Australia (Ato.gov.au, 2019). These needs to be fulfilled by them before the tax are being paid. The statutory requirements for tax compliances will be provided in the Stott’s Pty Ltd case study below:

- All kinds of receipts related to purchase and sales of the products of the business

- Records of salaries and wages and invoices of tax

- Any documents related to the GST

- All records of the sales and purchase of the assets of the business like office equipment, buildings and land

- Records related to the tax return, returns related to the fringe benefit tax, activity statement and employee super contributions

All the above items are necessary and are termed as the statutory requirements for the tax compliance that needs to be listed by any company situated in Australia.

Income tax from 2007-08 to 2010-11 is provided below

|

Income Tax |

2,52,966 |

3,13,366 |

3,64,795 |

4,36,928 |

Income Tax for 2011-12 for all quarters is provided below:

|

Income Tax |

680725.377 |

405892.8443 |

217323.6443 |

123039.0443 |

-65530.1558 |

The above evaluation done in this Stott’s Pty Ltd case study shows that the company is paying a tax at 30% on the profit that is earned by them. The amount of tax that is paid in the last year is $ 436,928.

Current compliance requirements and liabilities

According to the Corporations Act of 2001, it is noted in the present context of this Stott’s Pty Ltd case study that there are certain documents that are necessary for the organisations like Stott’s Pty Ltd. These are essential for the organisation so that they can show the financial position of the company. It is necessary for the organisation to keep the statement of the position of finance and the statement of the financial performance with them. The records that are necessary to be kept by them are provided below:

- Financial Statements: The role of financial statements discussed in the Stott’s Pty Ltd case study includes the cash flow statement, balance sheet and the income statement. These provide the financial position of the company to the stakeholders of the business.

- Cash Records: The purchases and sales that are performed with cash needs to be provided as a record for the tax officials to check whether the records provided are correct or not.

- Debtor / Sales Records: These are other important documents that are necessary to be provided as a record for the organisation. The sales records provide information related to the sales that are being performed through cash and the debtors records provide information of the sales that are not done through cash / bank.

- Creditors record: As per the research carried on this Stott’s Pty Ltd case study, it is noted that these are important documents that are necessary to be provided as record for the business. This record gives a clear view of the credit purchase that are done by the company at different points of time to perform some activities.

- Wages and superannuation records: All the records related to the wages and superannuation paid to the employees and workers need to be provided so that the tax officials can check the accuracy of the information that are provided in the statement of financial position.

Different accounting software

Currently the company is using Advanced Excel for analysing the financial condition of the company. Excel has several limitations and the chance of mistake is higher in this method of financial management. Forecasting is not much accurate under this process. In order to overcome the limitations discussed in the segments of Stott’s Pty Ltd case study the company should use different software.

There are various software that can be used by the company Stott’s Pty Ltd so that they can record all the transactions in one place to get the desired results. These are MYOB, XERO, Recon and Intuit.

Out of this four software, the best would be of using any one from MYOB and XERO. These are very high quality software that are used in the business. These help the business to get the actual results and helps the organisation to perform the activities automatically, that is, when the data is entered the calculations are done automatically and there are no errors found in these software. Thus, it can be stated in the study of Stott’s Pty Ltd case study that using this software will help the organisation to get the exact and accurate results for the business.

Principles of accounting

Matching principles demand the expenses of the same accounting period to be same and match with all the other. Stott’s Pty Limited uses all the principle of accounting and the integrity of this company is high. It helps the company to make a strong financial governance of the company. Account groups are used to collect all the accounts within a same group to increase the flexibility of the financial process. According to the concept of time period explored in the Stott’s Pty Ltd case study, different activities of a company are divided within several period of time. The sales and profit budget of the company has been done maintaining the accounting principles. Account group uses the information of budget and check the variations and controls the actual amount of cost to maintain the budget of the company.

Implications of Probity

Carl Kerns uses the probity principles to protect the rights of auditing in the company. The interests of the management of the organisations during performing the budgets is maintained by implying probity. The audit trails have been done by signing the employee timesheets and authority of the department manager in the company. Depositing cheques and withdrawals have been done as per the rules and regulations of the company. Evidenced transactions have been conducted to protect the rights and prevent misuse of the information in the company.

List of critical dates and initiatives

The Stott’s Pty Ltd case study also mentions that the company need to perform some activities which will help them to perform much better. These need to be done in the next financial year. These are

July- Commencement of the financial year

September- Preparation of the financial report for the 1st quarter

December- Preparation of the financial report for the 2nd quarter

March- Preparation of the financial report for the 3rd quarter

June- Preparation of the financial report for the 4th quarter and final report

Financial Year: 1st July – 30th June

GST quarterly: 4 quarters in a year such as September, December, March and June

List of budget items

The lists of items that are needed to be included in the budget of Stott’s Pty Ltd are as follows:

- Benefits

- Travel

- Meeting expenses

- Fees for training of employees

- Cost of supplies to office

- Services of book keeping and accounting

Internal Controls

There are modified and new internal controls that are present which can help the organisations like Stott’s Pty Ltd to improve their risk management (Journal of Accountancy, 2013). These are essential for the business to attract more shareholders for their business. These will be provided below:

Creating a new plan for a new team

It is noted in the Stott’s Pty Ltd case study that the COSO framework needs to be implemented by the Chief Financial Officer. This needs to be done by creating a new team and then making a new plan for the team and then applying it in the team. The internal auditors need to support the organisation by providing proper guidance to their co-employees so that there are no fraudulent activities.

Use an approach of building block

The building block needs to be applied by the management of the organisation through five components framework. These are risk assessment, environment control, monitoring and communication activities, information and control activities. These will help the organisation to control the risk factor in a proper manner to attract the shareholders of the business.

Focus points to be provided with proper attention

All the focus points need to be provided with proper attention so that the internal auditors can have a thorough look at different activities that are performed by the employees. This also reduces the risk factor for the organisation as well.

Project task 2

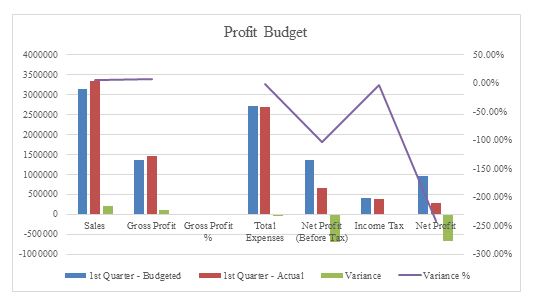

Develop an actual to budget variance report based on the format and template provided by Stott’s.

|

PROFIT BUDGET |

1st Quarter - Budgeted |

1st Quarter - Actual |

Variance |

Variance % |

F / O |

|

Revenue |

|||||

|

Sales |

3142822 |

3347825 |

205003 |

6.12% |

F |

|

– Cost of Goods Sold |

1783834.26 |

1647854 |

-135980 |

-8.25% |

F |

|

Gross Profit |

1358987.74 |

1454789 |

95801.26 |

6.59% |

F |

|

Gross Profit % |

0.432410025 |

||||

|

Expenses |

|||||

|

– Accounting Fees |

|||||

|

– Interest Expense |

21127 |

25145 |

4018 |

15.98% |

U |

|

– Bank Charges |

400 |

450 |

50 |

11.11% |

U |

|

– Depreciation |

2500 |

2200 |

-300 |

-13.64% |

F |

|

– Insurance |

3347.5 |

3500 |

152.5 |

4.36% |

U |

|

– Store Supplies |

|||||

|

– Advertising |

|||||

|

– Cleaning |

4815.25 |

5000 |

184.75 |

3.70% |

U |

|

– Repairs & Maintenance |

16068 |

15000 |

-1068 |

-7.12% |

F |

|

– Rent |

660127 |

660000 |

-127 |

-0.02% |

F |

|

– Telephone |

3749.2 |

3800 |

50.8 |

1.34% |

U |

|

– Electricity Expense |

6695 |

6795 |

100 |

1.47% |

U |

|

– Luxury Car Tax |

3224 |

3340 |

116 |

3.47% |

U |

|

– Fringe Benefits Tax |

7000 |

5000 |

-2000 |

-40.00% |

F |

|

– Superannuation |

521630.625 |

530000 |

8369.375 |

1.58% |

U |

|

– Wages & Salaries |

476375 |

470000 |

-6375 |

-1.36% |

F |

|

– Payroll Tax |

499002.8125 |

470000 |

-29002.8 |

-6.17% |

F |

|

– Workers’ Compensation |

485902.5 |

480000 |

-5902.5 |

-1.23% |

F |

|

Total Expenses |

2711963.888 |

2680230 |

-31733.9 |

-1.18% |

F |

|

Net Profit (Before Tax) |

1352976.148 |

667595 |

-685381 |

-102.66% |

U |

|

Income Tax |

405892.8443 |

390000 |

-15892.8 |

-4.08% |

F |

|

Net Profit |

947083.3033 |

277595 |

-669488 |

-241.17% |

U |

|

PROFIT BUDGET |

2nd Quarter Budgeted |

2nd Quarter Actual |

Variance |

Variance % |

F / O |

|

Revenue |

|||||

|

Sales |

3771386 |

4000000 |

228614 |

5.72% |

F |

|

– Cost of Goods Sold |

1783834.26 |

1500000 |

-283834 |

-18.92% |

F |

|

Gross Profit |

1987551.74 |

2500000 |

512448.3 |

20.50% |

F |

|

Gross Profit % |

0.527008304 |

||||

|

Expenses |

|||||

|

– Accounting Fees |

|||||

|

– Interest Expense |

21127 |

20000 |

-1127 |

-5.64% |

F |

|

– Bank Charges |

400 |

500 |

100 |

20.00% |

U |

|

– Depreciation |

2500 |

2600 |

100 |

3.85% |

U |

|

– Insurance |

3347.5 |

3500 |

152.5 |

4.36% |

U |

|

– Store Supplies |

|||||

|

– Advertising |

|||||

|

– Cleaning |

4815.25 |

5000 |

184.75 |

3.70% |

U |

|

– Repairs & Maintenance |

16068 |

17000 |

932 |

5.48% |

U |

|

– Rent |

660127 |

660000 |

-127 |

-0.02% |

F |

|

– Telephone |

3749.2 |

3800 |

50.8 |

1.34% |

U |

|

– Electricity Expense |

6695 |

6795 |

100 |

1.47% |

U |

|

– Luxury Car Tax |

3224 |

3340 |

116 |

3.47% |

U |

|

– Fringe Benefits Tax |

7000 |

5000 |

-2000 |

-40.00% |

F |

|

– Superannuation |

521630.625 |

520000 |

-1630.63 |

-0.31% |

F |

|

– Wages & Salaries |

476375 |

470000 |

-6375 |

-1.36% |

F |

|

– Payroll Tax |

499002.8125 |

470000 |

-29002.8 |

-6.17% |

F |

|

– Workers’ Compensation |

485902.5 |

480000 |

-5902.5 |

-1.23% |

F |

|

Total Expenses |

2711963.888 |

2667535 |

-44428.9 |

-1.67% |

F |

|

Net Profit (Before Tax) |

724412.1475 |

1332465 |

608052.9 |

45.63% |

F |

|

Income Tax |

217323.6443 |

200000 |

-17323.6 |

-8.66% |

F |

|

Net Profit |

507088.5033 |

1132465 |

625376.5 |

55.22% |

F |

|

PROFIT BUDGET |

3rd Quarter - Budgeted |

3rd Quarter - Actual |

Variance |

Variance % |

F / O |

|

Revenue |

|||||

|

Sales |

4085668 |

5000000 |

914332 |

18% |

F |

|

– Cost of Goods Sold |

1783834.26 |

1500000 |

-283834 |

-19% |

F |

|

Gross Profit |

2301833.74 |

3500000 |

1198166 |

34% |

F |

|

Gross Profit % |

0.563392263 |

-0.56339 |

|||

|

Expenses |

|||||

|

– Accounting Fees |

|||||

|

– Interest Expense |

21127 |

25145 |

4018 |

16% |

U |

|

– Bank Charges |

400 |

450 |

50 |

11% |

U |

|

– Depreciation |

2500 |

2200 |

-300 |

-14% |

F |

|

– Insurance |

3347.5 |

3500 |

152.5 |

4% |

U |

|

– Store Supplies |

|||||

|

– Advertising |

|||||

|

– Cleaning |

4815.25 |

5000 |

184.75 |

4% |

U |

|

– Repairs & Maintenance |

16068 |

15000 |

-1068 |

-7% |

F |

|

– Rent |

660127 |

660000 |

-127 |

0% |

U |

|

– Telephone |

3749.2 |

3800 |

50.8 |

1% |

U |

|

– Electricity Expense |

6695 |

6795 |

100 |

1% |

U |

|

– Luxury Car Tax |

3224 |

3340 |

116 |

3% |

U |

|

– Fringe Benefits Tax |

7000 |

5000 |

-2000 |

-40% |

F |

|

– Superannuation |

521630.625 |

530000 |

8369.375 |

2% |

F |

|

– Wages & Salaries |

476375 |

470000 |

-6375 |

-1% |

F |

|

– Payroll Tax |

499002.8125 |

470000 |

-29002.8 |

-6% |

F |

|

– Workers’ Compensation |

485902.5 |

480000 |

-5902.5 |

-1% |

F |

|

Total Expenses |

2711963.888 |

2680230 |

-31733.9 |

-1% |

F |

|

Net Profit (Before Tax) |

410130.1475 |

819770 |

409639.9 |

50% |

U |

|

Income Tax |

123039.0443 |

100000 |

-23039 |

-23% |

F |

|

Net Profit |

287091.1033 |

719770 |

432678.9 |

60% |

F |

|

PROFIT BUDGET |

4th Quarter - Budgeted |

4th Quarter - Actual |

Variance |

Variance % |

F / O |

|

Revenue |

|||||

|

Sales |

4714232 |

4000000 |

-714232 |

-17.9% |

U |

|

– Cost of Goods Sold |

1783834.26 |

1500000 |

-283834 |

-18.9% |

F |

|

Gross Profit |

2930397.74 |

2500000 |

-430398 |

-17.2% |

U |

|

Gross Profit % |

0.621606603 |

-0.62161 |

|||

|

Expenses |

|||||

|

– Accounting Fees |

|||||

|

– Interest Expense |

21127 |

20000 |

-1127 |

-5.6% |

F |

|

– Bank Charges |

400 |

500 |

100 |

20.0% |

U |

|

– Depreciation |

2500 |

2600 |

100 |

3.8% |

U |

|

– Insurance |

3347.5 |

3500 |

152.5 |

4.4% |

U |

|

– Store Supplies |

|||||

|

– Advertising |

|||||

|

– Cleaning |

4815.25 |

5000 |

184.75 |

3.7% |

U |

|

– Repairs & Maintenance |

16068 |

17000 |

932 |

5.5% |

U |

|

– Rent |

660127 |

660000 |

-127 |

0.0% |

U |

|

– Telephone |

3749.2 |

3800 |

50.8 |

1.3% |

U |

|

– Electricity Expense |

6695 |

6795 |

100 |

1.5% |

U |

|

– Luxury Car Tax |

3224 |

3340 |

116 |

3.5% |

U |

|

– Fringe Benefits Tax |

7000 |

5000 |

-2000 |

-40.0% |

F |

|

– Superannuation |

521630.625 |

520000 |

-1630.63 |

-0.3% |

F |

|

– Wages & Salaries |

476375 |

470000 |

-6375 |

-1.4% |

F |

|

– Payroll Tax |

499002.8125 |

470000 |

-29002.8 |

-6.2% |

F |

|

– Workers’ Compensation |

485902.5 |

480000 |

-5902.5 |

-1.2% |

F |

|

Total Expenses |

2711963.888 |

2667535 |

-44428.9 |

-1.7% |

F |

|

Net Profit (Before Tax) |

-218433.8525 |

1332465 |

1550899 |

116.4% |

F |

|

Income Tax |

-65530.15575 |

200000 |

265530.2 |

132.8% |

U |

|

Net Profit |

-152903.6968 |

1132465 |

1285369 |

113.5% |

F |

Table 5: Profit budget

Complete a cash flow analysis on the average length of time it takes Stott’s to collect funds from its debtors to determine the trend based on the financial reports in Project.

|

AGED DEBTORS BUDGET |

Qtr 1 |

Qtr 2 |

Qtr 3 |

Qtr 4 |

|

Sales |

33,71,200 |

37,71,386 |

40,85,668 |

47,14,232 |

|

% Debtors Sales |

22% |

22% |

22% |

22% |

|

Total Debtors |

7,41,664 |

829704.92 |

898846.96 |

1037131 |

|

Current |

5,85,915 |

5,85,915 |

585915 |

585915 |

|

30 Days |

1,11,250 |

2,43,790 |

312931.96 |

451216.04 |

|

60 Days |

37,083 |

3,42,125 |

272983.04 |

134698.96 |

|

90 Days |

7,417 |

98,335 |

39948.92 |

316517.08 |

|

Total Debtors |

7,41,664 |

829704.9 |

898847 |

1037131 |

Table 6: Debtor's Aging budget

Examine the sales budget, profit budget, cash flow budget and debtor ageing summary to identify the following in a report:

1.Issues

There are various issues mentioned in the Stott’s Pty Ltd case study that was seen in the budgeted and the actual report. These are that the company is unable to control their expenses. This is causing a huge problem in the performance of the company.

It is necessary for them to control their expenses and increase their profits. It is observed in this Stott’s Pty Ltd case study that in the fourth quarter they have performed well despite of a loss in the gross profit level. These are essential for the business so that they can perform well and reduce the risks properly. These are very much important for the business to perform the activities properly.

2. Variances

There are huge changes in the variances that are witnessed from the calculations. It is necessary for the business to check the variances and perform their work according to the performance.

iii. Performance

It is noted in the present Stott’s Pty Ltd case study that the performance of the company is better related to the budget that was prepared by the company. These are very much essential as they have performed beyond the expectations as well.

3. Comparison of the financial performance of the organisation as per the industry benchmark.

As per the calculated budget and the variance of the company within this Stott’s Pty Ltd case study, it can be stated that the company is a good performer in this industry and the financial competence of the company is high. As per the budget, it can be seen that the budgeted cost is higher than the actual cost of the company and it denotes that the management of cost is highly effective in the company. The retail industry is one of the strongest industries in the country and the graph of the performance is upwards. Market size of the industry is $131 billion and as per the size of the market, the company is performing in a highly effective way. Pattern of government funding for this industry is being changed and the amount of allotted fund in the industry by the government is increasing.

Stott’s is also focussing on increasing the performance with the performance of industry. The findings gained from the critical analysis of the Stott’s Pty Ltd case study mentions that average growth of this industry is 3.3% in Australia (IBISWorld, 2019). The company should give more effort on reduce the costing and maximum costing should be allotted to improve the quality of retailand on the infrastructure. It will help Stott’s to get a remarkable place in the industry and the performance will become a string pillar for the country.

4. Recommendations

As per the critical analysis of the Stott’s Pty Ltd case study, it can be seen that the cost of Stott’s Retail Store is higher compared to the industry performance and it should be reduced by applying effective strategy for costing. For an educational industry, main costing should be for recruiting quality human resources that can provide the right knowledge to the children and secondly the infrastructure should match the current trend of education. Stott’s should imply a modern and smart infrastructure for the company and it can be improved with time. The company discussed in the Stott’s Pty Ltd case study should allot the maximum amount cost for the infrastructure and recruitment.

If the evaluation procedure of the store can be more interesting and interactive, it can help the students to get ore attracted towards the institution. Type of evaluation should be modern and smart that can build the future of students more effectively and it should not only depend on the theoretical examination but the practical evaluation is more important. Practical evaluation can make the students more interested towards studying and it will increase the revenue of the institution. Interactive educational approaches will make the students more comfortable if the curriculum and style of retail can be different and more interesting, it will attract more students towards the organisation.

The readings used to prepare the Stott’s Pty Ltd case study signify that mental health of the students should be more concentrated and the students should feel free in the organisation. The company should provide more concentration and costing to build an infrastructure that will concentrate on the mental health of the students. Technological upgradation of the institution is another most important part of the organisation and it will help the students to get more updated with time. Smart work should be enabled in the institution and it will increase the profitability of the organisation. Process of evaluation can be changed and designed differently that the other organisations to attract more students. Another important factor illustrated in the Stott’s Pty Ltd case study for allocating cost of the company is increasing the capacity of the institution and it will help to attract more students and the quality of retail will be improved by recruiting more eligible resources.

Reduction of costing is the most important factor of the company to be done in order to increase the profitability but only profitability cannot be the option for an educational institution to be improved so the quality of retail should also be increased.

5. Evaluation

As per the Stott’s Pty Ltd case study, company follows the master budget as the financial management planning and a master budget includes different types of budgeting. Sales budget shows the main areas of Stott’s to gather revenue and Stott’s invests in several funds that increase the amount of earnings. The cash flow shows that Stott’s has the highest amount of investments for the investing activities that increase the revenue of the resources. Apart from the investing activities, Stott’s should increase the operating activities that will improve the quality of the organisational processes and more students can be attracted in this way. The recommendations of improving quality and the student management processes will help to increase the revenue of Stott’s. Different styles of studying and infrastructure discussed within this Stott’s Pty Ltd case study will help the company to get more students and the competitiveness of the institution can be increased.

Bibliography

Ato.gov.au. (2019). Keeping business records. Stott’s Pty Ltd case study Retrieved 8 November 2019, from https://www.ato.gov.au/General/Aboriginal-and-Torres-Strait-Islander-people/Tax-for-businesses/Keeping-business-records/

Budget, 2. (2019). 20 Expense Items to Consider When Creating a Budget | Karen Eber Davis Consulting. Kedconsult.com. Retrieved 8 November 2019, from https://www.kedconsult.com/articles-resources/expense-items-to-consider/

Documents.uow.edu.au. (2019). Probity. Retrieved 8 November 2019, from https://documents.uow.edu.au/~bmartin/dissent/documents/health/probity.html#:~:targetText=Probity%20protects%20the%20interests%20and,market%20and%20of%20marketplace%20globalisation.&targetText=When%20the%20community%20becomes%20a,how%20they%20will%20be%20provided.

IBISWorld, I., (2019). Stott’s Pty Ltd case study Market Research Reports & Analysis | IBISWorld AU. Ibisworld.com.au. Retrieved 13 November 2019, from https://www.ibisworld.com.au/industry-trends/market-research-reports/education-training/education-training.html.

Journal of Accountancy. (2013). 8 steps to update internal control. Retrieved 8 November 2019, from https://www.journalofaccountancy.com/news/2013/may/20137983.html

Legislation.gov.au., (2019). Financial Management and Accountability Act 1997. Retrieved 8 November 2019, from https://www.legislation.gov.au/Details/C2013C00282/Controls/.

MYOB Pulse., (2018). Accounting software. Stott’s Pty Ltd case study Retrieved 8 November 2019, from https://www.myob.com/au/blog/accounting-software/.

Schmidgall, R., & Kim, M. (2018). Stott’s Pty Ltd case study Operating budget processes and practices of clubs: a repeated cross-sectional study over four decades. Journal of Quality Assurance in Hospitality & Tourism, 19(4), 476-494.

Smallbusiness.wa.gov.au., (2019). Tax reporting requirements | Small Business. Retrieved 8 November 2019, from https://www.smallbusiness.wa.gov.au/business-advice/taxation/tax-reporting-requirements.

Song, J. H. (2017). Journal of International Trade Law and Policy. Stott’s Pty Ltd case study Law and Policy, 16(2), 92-105.