Management Accounting Assignment: Process Of Balance Scorecard Approach

Question

Task: To prepare this management accounting assignment, you should select a contemporary management accounting topic of his/her choice.

Answer

Introduction

A company can succeed when the strategic planning is adequately done and aligned with the vision and mission. The aim of the management accounting assignment report is to emphasize on the process of balance scorecard approach. Balance scorecard is a strategic management tool that enables the companies to translate the mission and vision of the organization into real actions (Cheowsuwan 2016). To conduct the study, one of the pioneer banks that are the Westpac Banking is selected. The research is conducted in the segment to provide an in-depth analysis on the benefits of the BSC in attaining the strategic aim of the bank. The report even discusses regarding the issue in the implementation and the common barriers that comes in the way of implementation.

Topic/process overview

Westpac banking corporation, a pioneer in the banking sector with the headquarters located in Sydney and one of the oldest banking giant operates with a customer base of 14 million and an employee base of 40,000 people. The core business is divided into five main divisions that is the business, wealth management, institutional bank and Westpac New Zealand. The report is prepared considering the theoretical base of the four pillars of the balance scorecard, a method that even influences the sustainability reporting. The four perspectives of the bank are correlated with the structure of the bank and the operations of the bank for social and environmental reporting.

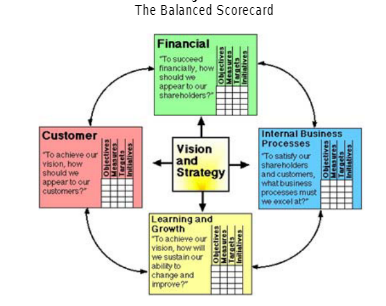

The Balance scorecard initiatives were coined in the year 1992 by Kalpan and Norton that helps in assisting the performance management followed by the measurement. It is a well defined structured mechanism that comprises of financial and non-financial aims. It supports in the stakeholder expectation evaluation and generates the strategic possibilities for attaining such demands. The main aim was to shift the company’s focus from the sole financial perspective. The balance scorecard provides the framework for setting the performance in four parameters that is the financial, customer, internal process and growth.

The methodology followed is to shift the performance from the performance management tool to the tool of the strategic decision making. The BSC model is increasingly popular and used by the corporate as it helps in the performance management. To implement the balance scorecard, the vision is clarified followed by the vision, core competencies and strategies. Further, these plans are converted into the four perspectives of the BSC that is the financial, customer, internal business, learning and growth (Cheowsuwan 2016). The scorecard is refined because it is communicated throughout the organization so that department can be linked with the total objectives of the organization. At the department level, the performance targets, as well as action plans are developed. Data is collected and performance is attained using the measures of performance. Furthermore, the employees are rewarded and results evaluated. The sustainability report of Westpac over the past 5 years has been evaluated. The total indicators are assessed with the reporting, as well as disclosure in every category. This measurement is needed to stress upon every category of reporting. Thereafter the sensitive issues are identified and legitimate tools are established for resolving the issue.

Overview of a Company (that has implemented the process)

Westpac aims to design the balance scorecard in line with the category of SBSC. The desired outcome from the analysis has helped the company to attain the goals

• Financial perspective

This pertains to the assessment from the strategy of the profitability. Though there appears no direct link with the sustainability reporting and profitability, the financial results can be forecasted and used for planning such as reduction of cost and compliance with the needs of sustainability (Roussas & McCaskill 2015). Further financial perspectives contain the assets management and the investment done in link to the sustainability management. This perspective even surrounds within itself that enhances the value of the shareholder and provides a positive influence for the stakeholders (Sting & Loch 2016).

• Customer perspective

This perspective helps the bank to identify the customer groups and segment and even the market share (Fattah & Syaripudin 2016). The strength and weakness of every customer group and segment is evaluated, as well as assesses. The aim is to move the focus of the customer to the supply chain so that sustainability management practises can be increased.

• Internal Business Process perspective

This category strives for the measurement of the success of the internal processes and system towards the creation of value. Service innovation must be in tune with the indicators of sustainability and must comprise of the organizational policies development to back up the traditional management followed by the sustainability development and reporting practises (Roussas & McCaskill 2015).

• Learning and Growth perspective

This perspective depends upon the ability of the organization to refresh the processes for leading a major ability. It helps in the development, as well as preservation of the capabilities followed by the employee morale as the sustainability view comprises consists of various disclosures in terms of employee profile, workload and rewards (Roussas & McCaskill 2015).

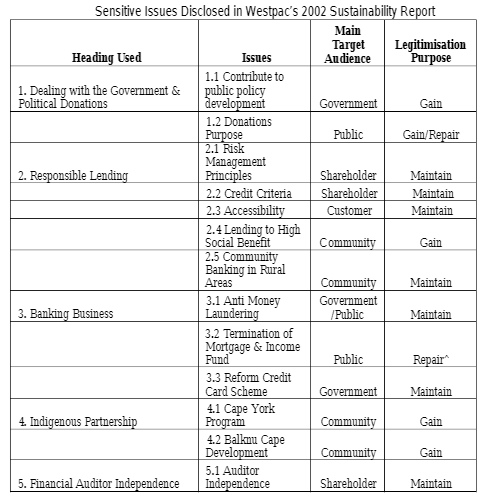

As compared to the initial balance scorecard view provided by Westpac in 2002, the focus has moved from the sustainability reporting and thereby the indicators classification has been altered that must be in tune with the SCGC rules. The tabular presentation is as follows:

The classification and a strong insight on each segment ha helped Westpac to focus on the major issues that is linked to the organization and hence it has undetaken measures of real time to resolve the issues using the technique of BSC and attain the target of sustainbaility for a greater extent.

Issues in implementation of Balanced scorecard in Westpac

The process of sustainability was introduced in the year 2002 and disclosures were made to the five major issues. The potential results of the same used by Westpac have been disclosed. Hence, it has followed the policies of risk mitigation followed by the defensive disclosures and response made to the criticism for the promotion of social value change. A reflection for the same is presented:

In the year 2008, the CEO of Westpac left the organization and hence resulted to the major change in the management. The reporting of the stakeholder impact was altered and new indicators were added to the sustainability reporting additionally to the indicators that was existing. Such were unexpected and contained valid information. For example, utilizing suppliers with a trading policy that is fair is included in the social perspective of the SSCM strategy. The system of providing coffee to the trading suppliers through the cafeterias of the company was initiated. It was done for the communication of the value of the company towards the transalation of the sustainability pricniples in everyday’s bank activities.

There was a major change in the management in the year 2008 and higher number of issues were reported. Theese were highlighted in the balance scorecard framework under particular caegories and learnig and growth indicators were updated for resolving the same.

The Global financial crisis together with the CEO departure affected the sustainability reporting and hence BSC was altered to ensure a balance to the changing needs. The disclosure of sensitive issue during this time frame doubled. Safeguarding the public from the global financial crisis became a top priority for Westpac and issues relating to the lending and risk management followed by employee development were properly incorporated. As every element requires proper attention, the BSC implementation is a tidy task (Westpac 2021).

The disclosures pertaining to the internal business processes perspective lead to higher importance but the reporting reduced during the crisis period. Westpac developed, as well as implemented policies of proper structure at the initial course but as years passed by lower disclosures were seen.

From the overall analysis of the BSC, it can be commented that the indicators used in the learning, as well as growth perspective contains less or the same matter with little innovation. Hence, addressing the perspectives is difficult. With higher sensitive issues being addressed, the stakeholder expectations increased comprehensively. This led to the performance of Westpac in difficult situation.

Assessment of the process

The indicators, as well as the contents has undergone change, the reports are imbalanced if the comparison is done over a period of time. The indicators percentage even differs referring to the fact that every organization might select the disclosure parameters where it has succeeded and eliminate the others (Dyduch 2019).

Thereby, it is a difficulty to ascertain the learning unless the same is converted into numbers. For the same, the increment in profits is utilized as a mechanism for measurement but the development of direct link between the two factors is difficult to be established.

The financial service sector prioritize on the customer service management and thereby the customers compliant followed by the resolution in the model appears to be high (Dechow 2012). Thereby, the measurement, as well as disclosure of the same remains a challenge.

The indicators linked to employee does not witness any significant changes and thereby the employee linked issues are not considered by the BSC in a proper way as every entity wants to create better image. The BSC in short addresses the compliance followed by the theoretical structure and the details regarding the smaller problems might not be addressed wholly. Furthermore, the company might face considerable challenges in the financial service sector like the weak metrics definition, improper data collection and reporting mechanism.

Higher stress on the internal processes and weak enhancement in the methodology might even appear as a barrier. The time and cost present in the data collection might be higher that the small firms might not be able to afford. The management being engaged with higher objectives and attainment of the financial targets, the ways to develop a perfect BSC might take a second position that results in the system lapse and hence question might appear for the BSC existence.

Conclusion

The BSC have both pros and cons. The BSC might bring every information into a single report and thereby can save time, money and resources. However, the stakeholder, as well as the employee engagement might be a daunting task to buy in as every employee might not act in unison to the ways given by the BSC. As seen Westpac BSC address the issues of the key stakeholder and the effectiveness with which the non-financial indicators are put to use for the benefit of the company. As a regular effort Westpac strives for growth, the practises is a key to the survival and development.

References

Cheowsuwan, T. 2016, ‘The Strategic Performance Measurements in Educational Organizations by Using Balance Scorecard’, International Journal of Modern Education and Computer Science, vol. 8, no. 12, pp. 17

Cheowsuwan, T. 2016, ‘The Strategic Performance Measurements in Educational Organizations by Using Balance Scorecard’, International Journal of Modern Education and Computer Science, vol. 8, no. 12, pp. 17-n/a. Dechow, N. 2012, ‘The balanced scorecard: subjects, concept and objects - a commentary’, Journal of Accounting & Organizational Change, vol. 8, no. 4, pp. 511-527.

Dyduch W 2019, ‘Entrepreneurial Strategy Stimulating Value Creation: Conceptual Findings and Some Empirical Tests’, Entrepreneurial Business and Economics Review, vol. 7, no. 3, pp. 65-82, viewed 9 November 2021, https://search.proquest.com/docview/2312212121/1BCE3A52379F4C58PQ/1accountid=30552 Fattah, D. & Syaripudin, M.A. 2016, ‘Philosophical Business Performance Competition on the Balance Scorecard Approach’, International Journal of Economic Perspectives, vol. 10, no. 4, pp. 541-551. Roussas, S. & McCaskill, A.D. 2015, ‘The Balance Scorecard versus Traditional Measurement System’, American Journal of Management, vol. 15, no. 3, pp. 36-42.

Roussas, S. & McCaskill, A.D. 2015, ‘The Balance Scorecard versus Traditional Measurement System’, Management accounting assignment American Journal of Management, vol. 15, no. 3, pp. 36-42.

Sting FJ & Loch CH 2016, ‘Implementing operations strategy: how vertical and horizontal coordination interact’, Production and Operations Management, vol. 25, no. 7, pp. 1177–1193, viewed 24 May 2020, https://search.proquest.com/docview/1803182568/87B6569D1DAC4ABDPQ/1accountid=30552

Westpac 2012, Westpac 2012 performance report, viewed 9 November 2021, https://www.westpac.com.au/content/dam/public/wbc/documents/pdf/aw/sustainability/2012_ Annual_Review_and_Sustainability_Report.pdf Westpac 2021, Westpac 2021 performance report, viewed 9 November 2021, https://www.westpac.com.au/content/dam/public/wbc/documents/pdf/aw/sustainability/WBC_ 2020_sustainability_performance_report.pdf