International Finance Assignment Examining Financial Performance Of Volvo

Question

Task:

You are required to prepare/submit an international finance assignmentreport discussing the following:

Choose a Multinational Enterprise (MNE) listed on an internationally recognised Stock Exchange (including for example, London, Dublin, New York or Paris).

It should be different than the company you have used previously for the first sit.

You are required to:

a. Critically discuss two recent developments in the international financial environment which appear to have impacted on your chosen company’s recent performance and development. Analyse how these two developments are likely to impact on the company in the near future.

b. Discuss the following key elements of the MNE’s international financial and/or risk management strategy (and how they appear to have affected the financial performance of your chosen company):

• Sources of finance

• Dividend policy

c. With reference to your chosen Multinational Enterprise (and using the most recent annual report published), analyse the financial performance (in terms of profitability, liquidity, efficiency and investment) of the company in the two most recent consecutive financial periods( e.g. 2018/19 or 2019/20, ) using 8 different accounting ratios (prior year comparative figures will be available in the annual report).

Answer

Introduction

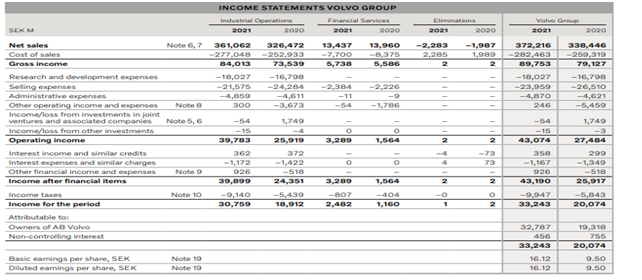

The Volvo Group, undertaken for the analysis on international finance assignment, is a multinational company, operating in Sweden. While the company’s main function is the production, sale and distribution of buses, trucks, and construction equipment, it also supplies industrial and marine drive systems and financial services (Volvogroup.com, 2022). Volvo was positioned as the second biggest manufacturer of huge-load trucks in 2016. The company recorded its strongest financial performance in 2021. Volvo reported net sales of SEK 372 billion, up from SEK 338 billion in 2020. Its operating income in 2021 amounted to SEK 41.0 billion. Volvo’s net income increased to SEK 33 billion in 2021 from SEK 20 billion in 2020 (Volvogroup.com, 2022).

The main objective of this report is to analyse the financial position of Volvo. This report sheds light on the two recent developments impacting the financial performance on Volvo. Furthermore, it discusses how the company manages risks related to its dividend policy and finance source. Finally, this report conducts a ratio analysis to interpret the financial position of chosen company.

Critically discussing two recent development in the international environment appear to have impacted on Volvo and how these developments arelikely to impact on the company in the near future

Development one: Cyber Security Breach

A data breach was reported on 1th December, 2021 by Volvo. The organisation claimed one of its file and documents had been accessed unlawfully by a third party.

Describing the development

As per the investigation, it was found that less number of the firm’s R&D property was stolen (Gatlan, 2021). A report by Digital Risk Protection Company CybelAngel claimed that the automotive sector is at greater threat of ransomware attacks because of the availability of thousands of exposed credentials online.

The investigation conducted by the company showed that highly sensitive data was leaked, such as blueprints of production facilities and engines, trade secrets, human resource documents, and personally identifiable data (Korosec, 2021). This threat mainly occurred because of the external security vulnerabilities and employee internal threats across the automotive supply chain.

Impact of the development on Volvo’s financial performance

As claimed by the Volvo group, the event of cyber security breach had no impact on its financial performance. The group did not specify the impact of such cyber security on the organisational operation. For example, its net sales increased to SEK 102 billion in the 4th quarter of 2021 compared to SEK 96 billion during the same period in 2020. However, its operating income decreased to SEK 10 billon in the 4th quarter of 2021 than SEK 12 billion during the same period in 2020 (Volvogroup.com, 2022). Its net income also reduced to SEK 10 billion the 4th quarter of 2021 compared to SEK 11 billion in 2020. EPS reduced to SEK 3.93 than 4.53.

However, Juma'h and Alnsour (2020) stated that the occurrence of data breach negatively impacts the financial performance of a business organisation. As a result of data breach, the companies generally become liable to their investors, customers, and employees. The same applies to the Volvo Group. In order to mitigate the losses and risks related to data breaches, the business organisational may utilise their reserved funds.

Strategy used by Volvo to mitigate the impact of the development

The company responded immediately to the development and implemented effective security countermeasures, such as the steps to stop further admittance to its R&D property and also notified the pertinent authorities. Volvo conducted an enquiry into the cyber security breach and engaged a cybersecurityexpert (Hope, 2021).

The organisation also claimed that cyber security is a priority. In order to prevent this type of development in future, Volvo actively engages in global work on best practices and standardisation, using and contributing to the cybersecurity suggestions acknowledged by the industry.

Development two: Covid-19

The second development that had a severe impact on the financial performance of Volvo is covid-19.

Describing the development

The automotive industry is critical for the global economy Due to the covid-19 pandemic; the automotive industry faces different challenges. For instance, Kufelová and Raková (2020) stated that because of the pandemic, sales of new vehicles in Russia decreased by 72.4% in April 2020 in comparison to the past year. On the other hand, the sales of new cars in Germany decreased by 61% to 120840 units because of the pandemic restrictions.

A report by Accenture shows that the automotive sector is heavily threatened by the covid-19 pandemic. After the initial manufacturing and supply disruption, the automotive industry is now facing a demand shock because of the travel restrictions imposed by the government. With limited opportunity to cut the fixed costs, some companies have lower liquidity to power through a long period of missing sales or revenues (Accenture.com, 2020). In addition to that, the pandemic had an adverse impact on the market capitalisation.

As the Volvo group is a key market player in the automotive sector, its operations and financial performance have been severely impacted by the pandemic.

Impact of the development on Volvo’s financial performance

In 2020, the covid-1 pandemic presented the Volvo Group with several challenges. In 2020, the net sales of Volvo decreased to SEK 338 billion compared to SEK 431 billion in 2019. Its operating income also reduced to SEK 27 billion in 2020 compared to SEK 49 billion in the past year. It operating margin reduced by 3.4% to 8.1% in 2020 (Volvogroup.com, 2021). The Volvo Group’s net income was reduced by a huge margin to SEK 20 billion in 2020 by SEK 36 billion in 2019.

Strategy used by Volvo to mitigate the impact of the development

Volvo continues to respond to the pandemic and adapts the measures on continuous basis. The company has undertaken several cost cutting initiatives to deal with the severe impact of the pandemic on its financial performance (Volvogroup.com, 2022). The company’s first priority was safety and security of its employees and society. The firm increase sanitisation and cleaning throughout its facilities. Volvo is also financing services and programs, which can be tailored specifically for its customers, whether they need help with existing buses, trucks, and construction equipment.

Dividend policy

According to Chauhanet al. (2019), dividend policy refers to the financial policies associated with paying cash dividend at present or spending an enhanced dividend at the later stage. It is a financial decision, which includes deciding on frequency of dividends, dividend payout ratio, and whether a company should pay the dividend or not.

Application of dividend theory to Volvo

The relevance theory of dividend applies here. As opined by Nguyen et al. (2019), the relevance theory of dividend suggests that the dividend decision influences the market worth of the company. Thus, dividend is important. As per this hypothesis, the investors of Volvo are risk averse. In addition to that, the Walter approach o dividend model applies to the company. For example, reinvestment rate of Volvo Company is greater than the cost of equity. The reinvestment rate refers to the return rate that a firm can earn on its retained earnings. Because of higher reinvestment rate than the cost of equity, it would be interest of Volvo to retain the earnings.

Dividend for last years

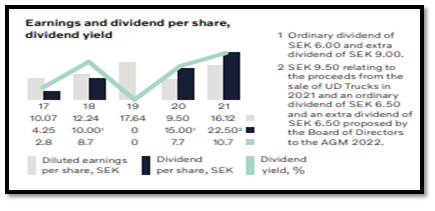

The Volvo group aims toproduce greater value for its shareholders. It is basically attained by a positive share price and payout of dividends. During 2016-2021, the price for the firms share increased by 9.7. The shareholders of this company collect a certain portfolio of retained earnings in form of dividend (Volvogroup.com, 2022). In 2021, the shareholders collected dividends of SEK 49820 million, involving the processes from divestment of UD trucks. During the annual meeting 2022, Volvo’s board of directors declared ordinary dividend of SEK6.50 per share and also extra dividend of SEK 6.50 per share. The Volvo Group paid the dividend of SEK 49.8 billion in 2021.

Figure 1: Dividends of Volvo, 2021

Source: (Volvogroup.com., 2022)

As per the above figure, dividend earnings of Volvo increased to SEK 16.12 per share compared to SEK 9.50 per share in 2020. In 2019, their dividend earnings per share wereSEK 9.50 per share. On other hand, it dividend yield rose to 10.7% in 2021 compared to 7.7% in 2020.

In 2021, the dividend per share was SEK 22.50. In 2020, the company’s dividend per share was SEK 15.50. Therefore, the dividend of the company is growing. The company mainly pays final dividend. There is no special dividend paid by the Volvo Group. Finally, it should be noted that the Volvo Group pays the dividend to its shareholders on an annual basis.

Influence in decision and capacity to pay dividends

Prior to the cyber security breach and covid-19 pandemic, the corporate management of Volvo consistently paid dividends to its shareholders. However, both the developments had a severe impact on the company’s capacity to pay dividends. The dividend to AB Volvo shareholders of SEK 20.3 billion had an adverse impact. For instance, its dividend yield decreased to 8.3% in 2019 compared to 8.7% in 2018.

Sources of Finance

A source of finance refers to where a business organisation gets money from to fund their business operations (Polzinet al. 2021). An organisation can gain finance from either external or internal sources.

Identification of finance sources for Volvo

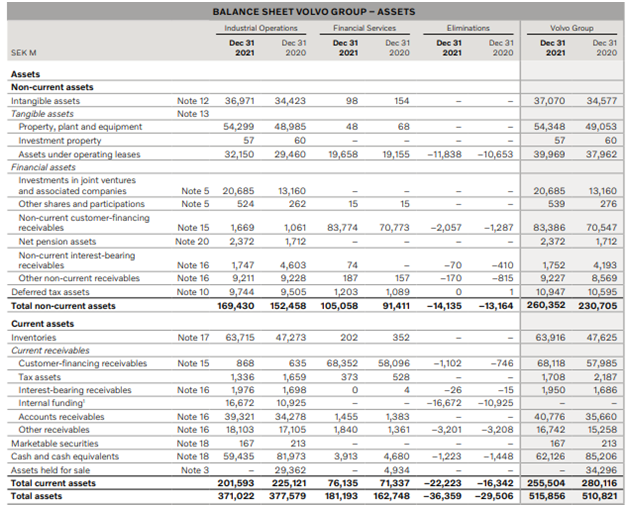

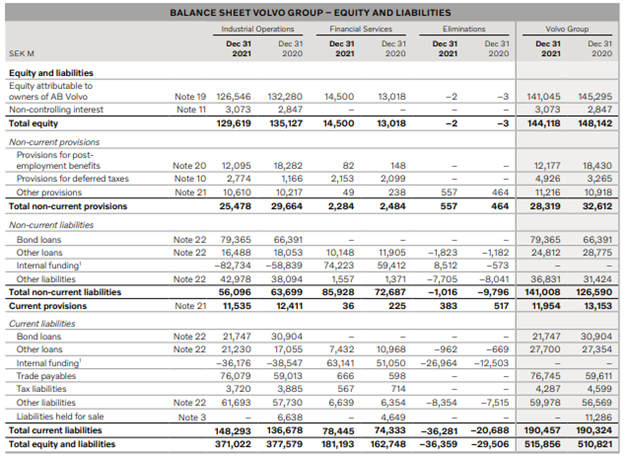

The Volvo group uses both debt and equity financing as its financing sources. The company had a total shareholder’s equity of SEK 148 billion and SEK 144 billion in 2020 and 2021 respectively. On the other hand, the company used both current and non-current liabilities as its financing source. Volvo had short-term debt of SEK 190 billion in 2020 and 2021. It had long-term debt of SEK 141 billion in 2021 and SEK 126 billion in 2020.

Component of each financing source

Equity

The balance sheet of Volvo for 2020-2021 shows that its equity attributable to the owners decreased to SEK 141 billion in 2021 compared to SEK 145 billion in 2020.

Figure 2: Balance Sheet Data of Volvo, 2020-2021

Source: (Volvogroup.com., 2022)

Debt

The elements of Volvo’s non-current liabilities are shown below. Its non-current liabilities include bond loans, internal funding, other loans and liabilities. Its non-current liabilities rose to SEK 141 billion as a result of increased bond loans of SEK 79 billion in 2021.

Figure 3: Balance Sheet Data of Volvo, 2020-2021

Source: (Volvogroup.com., 2022)

The gearing ratio of Volvo has been calculated in below table for the last three years:

|

|

2021 |

2020 |

2019 |

|

|

49.54% |

46.08% |

49.33% |

The calculation shows that the gearing ratios of Volvo were 49.54% in 2021, 46.08% in 2020, and 49.33 % in 2019. It means the company is less leveraged as its liabilities constitute less than 50% of its capital structure. The debt level of Volvo decreased gradually in 2020 compared to 2019. However, it gradually increased to 49.54% in 2021.

WACC and application of capital structure theory

Weighted Average Cost of Capital (WACC) refers to weighted average costs of debts and equity where the weights are considered the amount of capital raised from every source. Here, the net income approach of capital structure can be applied. As per the opinion of Wedanaet al. (2020), net income theory of capital structure suggests that can a change in a company’s financial leverage will result in a corresponding change in WACC. Increase in debt proportion causes a reduction in WACC that in turn increases the firm value.

However, the gearing ratio suggests that the capital structure of the Volvo group is optimal.

Influences, cash management, and liquidity risks

In 2020, the operating cash flow in industrial operation of Volvo amounted to SEK 18.5 billion. The reduction in operating cash flow than 2019 was a result of reduced operating income and increased working capital. The operating cash flow in financial services reduced to SEK 0.8 billion in 2020 compared to SEK 14 billion in 2019. The reduction was mainly driven because of lower increase of new business volume. In addition to that, its new borrowings enhanced by SEK 7.3 billion in 2020 to protect its liquidity in the company. No dividend was also paid to the shareholders of AB Volvo in 2020.

Ratio Analysis

Ratio analysis basically compares the line-data from a firm’s financial reports to attain insights regarding liquidity, profitability, solvency, and operational efficiency (Dance and Imade, 2019). Different financial ratios have been computed for Volvo to interpret its financial performance for last three years. A comparison has also been made with its one of the leading competitors, BMW group.

Profitability Ratios

Return On Asset (ROA)

ROA refers to a financial ratio, which interprets how profitable a company is relation to its total assets (Marito and Sjarif, 2020).

|

|

Volvo |

BMW Group |

||||

|

|

2021 (SEK M) |

2020 (SEK M) |

2019 (SEK M) |

2021 (€ million) |

2020 (€ million) |

2019 (€ million) |

|

Net Income |

33,243 |

20,074 |

36,495 |

12,463 |

3,857 |

5,022 |

|

Total Assets |

515,856 |

510,821 |

524,837 |

229,527 |

216,658 |

228,034 |

|

ROA (Net Income / Total Assets) |

6.44% |

3.93% |

6.95% |

5.43% |

1.78% |

2.20% |

Source: (Volvogroup.com, 2022)

Source: (Bmwgroup.com, 2022)

ROA of Volvo reduced to 3.93% in 2020 compared to 6.95% in 2019. However, its ROA increased to 6.44% in 2021; however, BMW’s ROA was much lower with only 5.43%. The reduction in ROA in 2020 was a result of reduction in Volvo’s total assets value.

Several factors account for the reduction and increase in ROA. Total assets value of Volvo decreased to SEK 510 billion in 2020 compared to SEK 524 billion in 2019. However, the value increased to SEK 33 billion in 2021. It means the company was sufficiently capable of generating income from its assets.

Some contextual reasons can be defined for the ratio movement. The travel restrictions imposed by government as a result of pandemic had an adverse impact on the net income of Volvo.

Return on Equity (ROE)

ROE is a ratio that specifies how much net income can be generated as a result of per dollar of invested capital (Rahmantio, 2018).

|

|

Volvo |

BMW Group |

||||

|

|

2021 (SEK M) |

2020 (SEK M) |

2019 (SEK M) |

2021 (€ million) |

2020 (€ million) |

2019 (€ million) |

|

Net Income |

33,243 |

20,074 |

36,495 |

12,463 |

3,857 |

5,022 |

|

Total shareholders' equity |

144,118 |

148,142 |

141,678 |

75,132 |

61,520 |

59,907 |

|

ROE (Net Income / shareholders equity) |

23.07% |

13.55% |

25.76% |

16.59% |

6.27% |

8.38% |

Source: (Volvogroup.com, 2022)

Source: (Bmwgroup.com, 2022)

ROE of Volvo reduced to 13.55% in 2020 and increased to 23.07% in 2021. However, the ROE of BMW was much lower with 16.59% and 6.27% in 2021 and 2020 respectively. Reduction in ROE was also a result of reduction in Volvo’s net income; however, it performed better than BMW group.

Several factors account for the reduction and increase in ROE. It net income decreased to SEK 20 billion in 2020 compared to SEK 36 billion in 2019. On the other hand, its equity decreased to AED 148 billion in 2020 than SEK 141 billion in 2019 (Volvogroup.com, 2021).

In terms of contextual factors, it can be said that the pandemic negatively impacted the net income of Volvo.

Net Profit Margin

Net profit margin measures the level of net income produced as a percentage of revenue (Nariswari and Nugraha, 2020).

|

|

Volvo |

BMW Group |

||||

|

|

2021 (SEK M) |

2020 (SEK M) |

2019 (SEK M) |

2021 (€ million) |

2020 (€ million) |

2019 (€ million) |

|

Net Income |

33,243 |

20,074 |

36,495 |

12,463 |

3,857 |

5,022 |

|

Net Sales |

372,216 |

338,446 |

431,980 |

111,239 |

98,990 |

104,210 |

|

Net profit margin (net profit / net sales) |

8.93% |

5.93% |

8.45% |

11.20% |

3.90% |

4.82% |

Source: (Volvogroup.com, 2022)

Source: (Bmwgroup.com, 2022)

Net profit margin of Volvo reduced to 5.93% in 2020 and increased to 8.93% in 2021. However, its competitor, such as BMW’s net profit margin was higher with 11.20% in 2021. The increase can be considered a result of improved sales of Volvo.

The reduction and increase in net profit margin is driven by several factors. For instance, Volvo’s net sales decreased to SEK 338 billion in 2020 and increased to SEK 372 billion in 2021.

The reduction in net profit margin in 2020 was a result of travel restrictions imposed by the government to prevent the spread of corona virus (Volvogroup.com, 2021).

Efficiency Ratios

Inventory turnover days

It is the ratio that measures the rate that inventory stock is used, sold, and replaced (Amanda, 2019)

|

|

Volvo |

BMW Group |

||||

|

|

2021 (SEK M) |

2020 (SEK M) |

2019 (SEK M) |

2021 (€ million) |

2020 (€ million) |

2019 (€ million) |

|

Inventory |

63,916 |

47,625 |

56,644 |

15,928 |

14,896 |

15,891 |

|

Cost of Sales |

282,463 |

259,319 |

325,603 |

89,253 |

85,408 |

86,147 |

|

Inventory turnover (inventory / cost of sales * 365) (days) |

82.59 |

67.03 |

63.50 |

65.14 |

63.66 |

67.33 |

Source: (Volvogroup.com, 2022)

Source: (Bmwgroup.com, 2022)

The inventory turnover days of Volvo increased to 67.03 days in 2020 and 82.59 days in 2021 from 63.50 days in 2019. However, BMW’s inventory turnover was only 65 days in 2021.It interprets less effective management of the inventories by Volvo.

The reduction in cost of sales and increase in inventory is the result of increase in inventory days. It indicates that the corporate management of Volvo has an intention to keeping greater level of inventory.

In terms of contextual factors, it can be said that the company has an increasing number of construction equipment in inventory as of both 2020 and 2021. The reduction in demand for road travel and construction caused the inventory turnover days to increase.

Receivable turnover days

This ratio measures the effectiveness with which a firm collects its receivables and extends credit to the customers (Rianyet al. 2021).

|

|

Volvo |

BMW Group |

||||

|

|

2021 (SEK M) |

2020 (SEK M) |

2019 (SEK M) |

2021 (€ million) |

2020 (€ million) |

2019 (€ million) |

|

Receivables |

40,776 |

35,660 |

37,723 |

2,261 |

2,298 |

2,518 |

|

Revenue |

372,216 |

338,446 |

431,980 |

111,239 |

98,990 |

104,210 |

|

Receivable turnover days (receivables / total revenue * 365) |

39.99 |

38.46 |

31.87 |

7.42 |

8.47 |

8.82 |

Source: (Volvogroup.com, 2022)

Source: (Bmwgroup.com, 2022)

Receivable turnover days of Volvo increased to 38 days and 40 days in 2020 and 2021 respectively. However, receivable turnover of BMW was only 7 and 8 days in 2021 and 2020 respectively. It interprets the Volvo’s inefficiency in collecting the receivables.

The decrease in both sales and accounts receivable was the main reason of increasing receivable turnover days in 2020. As a result of the pandemic, the customers were delaying their payments.

The Volvo group claims that there were a huge number of uncollected receivables due to the pandemic.

|

|

Volvo |

BMW Group |

||||

|

|

2021 (SEK M) |

2020 (SEK M) |

2019 (SEK M) |

2021 (€ million) |

2020 (€ million) |

2019 (€ million) |

|

Current asset |

255,504 |

280,116 |

282,187 |

86,173 |

81,807 |

90,630 |

|

Current liabilities |

190,457 |

190,324 |

194,410 |

76,466 |

71,963 |

82,625 |

|

Current ratio (current assets / current liabilities) |

1.34 |

1.47 |

1.45 |

1.13 |

1.14 |

1.10 |

Source: (Volvogroup.com, 2022)

Source: (Bmwgroup.com, 2022)

The current ratio of Volvo increased from 1.45 in 2019 to 1.47 in 2020 and decreased to 1.34 in 2021. BMW’s current ratio was slightly lower with 1.13 and 1.14 in 2021 and 2020 respectively. The higher current ratio indicates that Volvo is more capable of mitigating its current liabilities. The increase or decrease in current ratio was a result of increase or decrease in current assets. In terms of contextual factor, it has been found that that increase in the short-term investments caused an increase in its current ratio.

Quick Ratio

Quick ratio measures the organisational ability to pay off all the debt obligations with most liquid assets (Susanti, 2022).

|

|

Volvo |

BMW Group |

||||

|

|

2021 (SEK M) |

2020 (SEK M) |

2019 (SEK M) |

2021 (€ million) |

2020 (€ million) |

2019 (€ million) |

|

Current asset |

255,504 |

280,116 |

282,187 |

86,173 |

81,807 |

90,630 |

|

Inventory |

63,916 |

47,625 |

56,644 |

15,928 |

14,896 |

15,891 |

|

Current liabilities |

190,457 |

190,324 |

194,410 |

76,466 |

71,963 |

82,625 |

|

Current ratio (current assets-inventory / current liabilities) |

1.01 |

1.22 |

1.16 |

0.92 |

0.93 |

0.90 |

Source: (Volvogroup.com, 2022)

Source: (Bmwgroup.com, 2022)

The reduction in quick ratio from 1.22 to 1.01 in 2021 indicates a decreasing ability of Volvo to pay its debts with its most liquid assets. However, BMW’s quick ratio was lower than the ratio of Volvo. It indicates Volvo has more capacity than BMW to pay its liabilities with help of most liquid assets.

The increase or decrease in the quick ratio was a result of increase or decrease in inventory. In terms of contextual factor, it has been found that that increase in the short-term investments caused an increase in its current ratio.

|

|

Volvo |

BMW Group |

||||

|

|

2021 (SEK M) |

2020 (SEK M) |

2019 (SEK M) |

2021 (€ million) |

2020 (€ million) |

2019 (€ million) |

|

Total debt |

331,465 |

316,914 |

332,337 |

154395 |

155138 |

168127 |

|

Total equity |

144,118 |

148,142 |

141,678 |

75,132 |

61,520 |

59,907 |

|

Debt to equity ratio |

2.30 |

2.14 |

2.35 |

2.05 |

2.52 |

2.81 |

Source: (Volvogroup.com, 2022)

Source: (Bmwgroup.com, 2022)

Debt to equity ratio of Volvo increased 2.30 in 2021 compared to 2.14 in 2020. On the other hand, debt to equity ratio of BMW was lower with 2.05 in 2021. It interprets that Volvo is in more leveraged position. The increase in the debt to equity ratio was a result of increased debt. The debt increased as a result of several contextual factors, such as the pandemic.

Conclusion

The report concludes that the first development of cyber security had no significant impact on Volvo’s financial performance. However, the second development, such as covid-19 pandemic negatively impacted the revenue and dividend payment of the company. The financial ratio analysis indicates the company performed better in 2021 compared to 2020.

References

Accenture.com., 2020. Impact on the Automotive Industry: Navigating the Human and Business Impact of COVID-19. Available at: https://www.accenture.com/_acnmedia/PDF-121/Accenture-Covid-19-Impact-Automotive-Industry.pdf

Amanda, R.I., 2019. The impact of cash turnover, receivable turnover, inventory turnover, current ratio and debt to equity ratio on profitability. Journal of research in management, 2(2). Available at: https://pdfs.semanticscholar.org/8665/844b09d9758fd638a5f3ee63312502b1ebfd.pdf

Bmwgroup.com., 2020. Annual Report 2019. Available at: https://www.bmwgroup.com/content/dam/grpw/websites/bmwgroup_com/ir/downloads/en/2020/gb/BMW-GB19_en_Finanzbericht.pdf

Bmwgroup.com., 2022. BMW Group Report 2021. Available at: https://www.bmwgroup.com/content/dam/grpw/websites/bmwgroup_com/ir/downloads/en/2022/bericht/BMW-Group-Report-2021-en.pdf

Chauhan, J., Ansari, M.S., Taqi, M. and Ajmal, M., 2019.Dividend policy and its impact on performance of Indian information technology companies. International Journal of Finance and Accounting, 8(1), pp.36-42. Available at: https://www.researchgate.net/profile/Mohd-Taqi/publication/341043513_Dividend_Policy_and_Its_Impact_on_Performance_of_Indian_Information_Technology_

Companies/links/5eaaaa7d299bf18b958857fa/Dividend-Policy-and-Its-Impact-on-Performance-of-Indian-

Information-Technology-Companies.pdf

Dance, M. and Imade, S., 2019. Financial ratio analysis in predicting financial conditions distress in indonesia stock exchange. Russian Journal of Agricultural and Socio-Economic Sciences, 86(2). Available at: https://cyberleninka.ru/article/n/financial-ratio-analysis-in-predicting-financial-conditions-distress-in-indonesia-stock-exchange

Gatlan, S., 2021. Volvo Cars discloses security breach leading to R&D data theft. Bleepingcomputer. Available at: https://www.bleepingcomputer.com/news/security/volvo-cars-discloses-security-breach-leading-to-randd-data-theft/ Hope, A., 2021. Volvo Security Breach Led to R&D Data Theft by ‘Snatch’ Threat Actors. CPO Magazine. Available at: https://www.cpomagazine.com/cyber-security/volvo-security-breach-led-to-rd-data-theft-by-snatch-threat-actors/ Juma'h, A.H. and Alnsour, Y., 2020. The effect of data breaches on company performance.international finance assignment International Journal of Accounting & Information Management. Available at: https://www.researchgate.net/profile/Yazan-Alnsour/publication/335002124_The_Effect_of_Data_Breaches_on_Company_Performance/links/ 5da66af54585159bc3d010af/The-Effect-of-Data-Breaches-on-Company-Performance

Korosec, K., 2021. Volvo had some R&D data stolen in security breach. Tech crunch. Available at: https://techcrunch.com/2021/12/10/volvo-had-some-rd-data-stolen-in-security-breach/

Kufelová, I. and Raková, M., 2020.Impact of the Covid-19 pandemic on the automotive industry in Slovakia and selected countries.In SHS Web of Conferences (Vol. 83, p. 01040).EDP Sciences. Available at: https://www.shs-conferences.org/articles/shsconf/pdf/2020/11/shsconf_appsconf2020_01040.pdf

Marito, B.C. and Sjarif, A.D., 2020. The impact of current ratio, debt to equity ratio, return on assets, dividend yield, and market capitalization on stock return (Evidence from listed manufacturing companies in Indonesia Stock Exchange). Economics, 7(1), pp.10-16. Available at: https://core.ac.uk/download/pdf/326785456.pdf

Nariswari, T.N. and Nugraha, N.M., 2020. Profit growth: impact of net profit margin, gross profit margin and total assests turnover. International Journal of Finance & Banking Studies (2147-4486), 9(4), pp.87-96. Available at: https://www.ssbfnet.com/ojs/index.php/ijfbs/article/download/937/712

Nguyen, D.T., Bui, M.H. and Do, D.H., 2019. The Relationship Of Dividend Policy and Share Price Volatility: A Case in Vietnam. Annals of Economics & Finance, 20(1). Available at: https://www.researchgate.net/profile/Mai-Bui-15/publication/341342659_The_Relationship_Of_Dividend_Policy_and_Share_Price_Volatility_A_Case_

in_Vietnam/links/5ebb7a83a6fdcc90d6723e5a/The-Relationship-Of-Dividend-Policy-and-Share-

Price-Volatility-A-Case-in-Vietnam.pdf

Nuryani, Y. and Sunarsi, D., 2020. The Effect of Current Ratio and Debt to Equity Ratio on Deviding Growth. JASa (JurnalAkuntansi, Audit danSistemInformasiAkuntansi), 4(2), pp.304-312. Available at: https://journalfeb.unla.ac.id/index.php/jasa/article/download/1378/885

Polzin, F., Sanders, M. and Serebriakova, A., 2021. Finance in global transition scenarios: Mapping investments by technology into finance needs by source. Energy Economics, 99, p.105281. Available at: https://www.sciencedirect.com/science/article/pii/S0140988321001869

Rahmantio, I., 2018. Pengaruh Debt to Equity Ratio, Return on Equity, Return on Asset danUkuran Perusahaan TerhadapNilai Perusahaan (Studipada Perusahaan Pertambangan yang Terdaftar di Bursa Efek Indonesia Tahun 2012-2016) (Doctoral dissertation, UniversitasBrawijaya). Available at: http://repository.ub.ac.id/10247/4/BAGIAN%20DEPAN.pdf Riany, D., Norisanti, N. and Komariah, K., 2021. Financial Performance Analysis Using Inventory Turn Over Ratio, Receivable Turn Over Ratio, and Fixed Asset Turn Over Ratio. Almana: JurnalManajemendanBisnis, 5(1), pp.7-13. Available at: https://journalfeb.unla.ac.id/index.php/almana/article/download/1426/968

Susanti, N., 2022. The Influence of Current Ratio, Quick Ratio and Net Profit Margin on Return on Investment at PT. Telekomunikasi Indonesia (Tbk). PINISI Discretion Review, 1(1), pp.127-136. Available at: https://ojs.unm.ac.id/UDR/article/viewFile/13387/7843

Volvogroup.com., 2021. REPORT ON THE FOURTH QUARTER AND FULL YEAR 2020. Available at: https://www.volvogroup.com/content/dam/volvo/volvo-group/markets/global/en-en/news/2021/feb/3880618-volvo-group-q4-2020-report-eng.pdf

Volvogroup.com., 2021. VOLVO GROUP ANNUAL AND SUSTAINABILITY REPORT 2020. Available at: https://www.volvogroup.com/content/dam/volvo/volvo-group/markets/global/en-en/investors/reports-and-presentations/annual-reports/annual-and-sustainability-report-2020.pdf

Volvogroup.com., 2022. Committed to make a difference. Available at: https://www.volvogroup.com/en/covid-19.html#:~:text=We%20have%20contributed%20to%20the,partnership%20with%20Akshaya%20Patra%20NGO.

Volvogroup.com., 2022. Report On The Fourth Quarter And Full Year 2021. Available at: https://www.volvogroup.com/content/dam/volvo-group/markets/master/news/2022/jan/4169226-volvo-q4-2021-eng.pdf

Volvogroup.com., 2022. Volvo Group Annual and Sustainability Report 2021. Available at: https://www.volvogroup.com/content/dam/volvo-group/markets/master/investors/reports-and-presentations/annual-reports/annual-and-sustainability-report-2021.pdf

Volvogroup.com., 2022. What we do. Available at: https://www.volvogroup.com/en/about-us/what-we-do.html

Wedana, Y.A. and Gunarta, I.K., 2020, August.Determination of Business Port Terminal Value Using Income Approach. In IOP Conference Series: Earth and Environmental Science (Vol. 557, No. 1, p. 012063). IOP Publishing. Available at: https://iopscience.iop.org/article/10.1088/1755-1315/557/1/012063/pdf

Appendix