Economics Assignment Discussing Cases Using Managerial Economic Concepts

Question

Task: This economics assignmenthas two parts. Part (A) is problem solving and short answer. Part (B) is a mini project. Answer all questions and do not exceed 3300 words in total.

Part A- Each question carries 9 marks.

1. Cola and pizza are complements. Suppose that the cost of producing cola increases. Explain, using appropriate diagrams, how this will impact the equilibrium price and quantity of cola and how this will impact the equilibrium price and quantity of pizza.

2. Discuss 2 determinants each of the price elasticity of demand and the price elasticity of supply.

3. For lunch, Misha eats only salads or fruit & yogurt smoothies. Her weekly food budget is $48. Each salad costs $8 and each smoothie costs $3.

a. Draw Misha’s budget constraint.

b. What is the opportunity cost of purchasing one more smoothie What is the opportunity cost of purchasing one more salad

c. Describe intuitively how Misha should make the optimal consumption decision.

d. Suppose that Misha income falls from $48 to $24. Show what happens to the budget constraint. Is it possible that Misha will consume more salad as a result of this

4. Refer to the table below. Fill in the missing values in the table.

|

Quantity |

Price |

Total Cost |

Total Revenue |

Marginal Revenue |

Marginal Cost |

Profit |

|

0 |

$6 |

$9 |

|

|

|

|

|

1 |

$6 |

$11 |

|

|

|

|

|

2 |

$6 |

$13 |

|

|

|

|

|

3 |

$6 |

$16 |

|

|

|

|

|

4 |

$6 |

$19 |

|

|

|

|

|

5 |

$6 |

$25 |

|

|

|

|

|

6 |

$6 |

$30 |

|

|

|

|

|

7 |

$6 |

$45 |

|

|

|

|

5. The following questions relate to a firm’s costs.

a. Briefly explain what is meant by the term "fixed costs" and provide an example of a fixed cost.

b. Briefly explain what is meant by the term "variable costs” and provide an example of a variable cost.

c. Explain how fixed and variable costs play a role in the decision for a firm to shut down in the short run and in the long run.

6. The following figure shows the average cost curve, demand curve, and marginal revenue curve for a monopolist. After maximizing profits, what does the firm’s total profit equal Indicate the area of the rectangle (e.g. ABGH, BDEG, etc…)

Part B- Each question carries 6 marks.

These following questions are fairly open-ended. We have discussed various market structures in this module, and we are looking for you to apply what you have learned to real-world data.

8. Select a single news article which discusses prices in a particular market. Provide a brief summary of this news article using your own words.

• You are free to select any market and news article of your choosing. For example, it could be an article which discusses the price of gasoline in a country, or an article which discusses the price of housing in a city. It is up to you.

• Some articles will give you a lot more to discuss than others. Searching on google news is a good starting point.

9. Describe the structure of the market, and relate what is discussed in the article to the concepts discussed in this course.

• For example, can you describe a sudden price jump by a cartel breaking apart, or by a demand shock Or can you describe a gradual decline in prices by a gradual change in consumer tastes

Answer

Economics AssignmentPart A

Answer to question 1:>

Complementary goods are products or service which are consumed together and the product or service adds value to each other. In case of the complementary good, products or services are related to each other negatively, which means, if the price of one good change then the demand of the other good or service changes in the opposite direction. This relation between the complementary goods exists as the three is negative cross elasticity of demand operating that leads to negative association between two complementary good or service. For instance, if the given case is considered where pizza and cola are complemented to each other, then a rise in the price of cola will lead to fall in the demand of the pizza. However, it is also important to mention that, complement goods can be connected with each other at high or low level of association (Pasha and Shahbazi 2019). This means, if the products are strong complement, then a change in price of one product will reflect higher change in demand of the other goods. In case of the weak complement goods, change in price will lead to lower demand change for the complementary good.

Underpinning the theory of the complementary good, if the given case is considered where the cola and pizza are complementary, then it can be seen that as the cost of producing cola increase, it will increase the price of cola. Due to the negative cross elasticity of demand, with the increase in the price of cola, there will be fall in the demand of the pizza too.

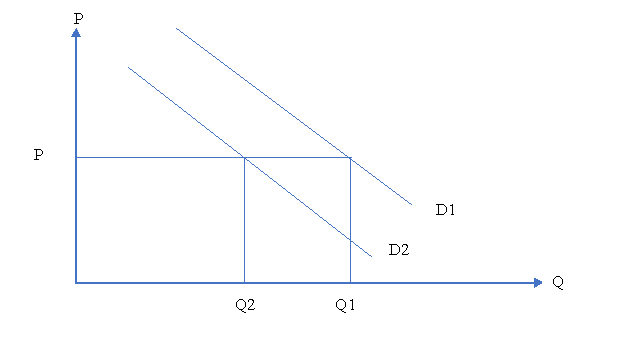

Figure 1: price increase impact on complementary good

As per the figure 1, it can be seen that, if the initial demand is D1, then an increase in the price of cola, lead the demand to fall to D2. Hence, with the rise in production cost, there will be a fall in consumption both the cola and pizza; however, with the available information it is hard to determine what will be the magnitude of fall of consumption for both the product (Rostek and Yoder 2020). Besides, due to change in the demand, new equilibrium price will remain same, whereas, equilibrium demand will fall from Q1 to Q2.

Answer to question 2:

Price elasticity, as the name suggests, is the measure of responsiveness of quantity demanded or supplied of a good or service due to change in the price of the same. As per the demand and supply framework, both the demand and supply curve represent the amount of good or service demanded and supplied at given price (Yashkina 2017). Hence, price elasticity of demand and supply represent the responsiveness of the respective demand and the supply with change in the price. Through a detailed analysis of the respective elasticities, characteristics of them has been mentioned below.

Price elasticity of demand is the change in the percentage demand of quantity of a good or service due to the change in the price. On the other hand, price elasticity of supply is the percentage change in the quantity supplied of a good or service due to the change in price. Hence, price elasticities represent demand and supply change due to the change in price

Considering this, two factors that influence the price elasticity of demand are as follows (Labanderiaet al. 2017):

- Availability of substitutes – if there is substitute available, then the price elasticity of demand will be more than 1. Which means, change in quantity demand will be more than the change in price. This because, people will shift to substitute due to the change in the price.

- Type of good (luxury or necessary) – depending upon the type of good whether they are luxury of necessary, price elasticity of demand is determined. For the necessary goods, price elasticity of good is low as the change in demand is low due to change in price. Whereas, for the luxury goods, they have high elasticity of demand as change in demand is very high due to the change in price.

Two factors that influence the price elasticity of supply are as follows:

- Number of producers – when the number of producers is high, availability of alternatives is high. People can move from one product to another easily making the elasticity of supply high with increasing number of producers in the market (Dadkhah and Vahidi 2018).

- Price of inputs – this determines the amount of goods and services supplied as the supplier get time to respond to price change. When there is change in price of inputs, producers find it difficult to change price instantly in response making the supply of products inelastic. Hence depending upon the price of input and response time, price elasticity of supply is influenced.

Answer to question 3:

Considering the idea of the budget constraint, opportunity cost and consumption decision making, here analysis has been done for Misha who eats salad or fruit and yogurt in her lunch. As per the given scenario, Misha has $48 for her lunch budget and the cost of each salad is $8 and smoothies is $3. Now, as per the given scenario, budget constraint, opportunity cost, optimal consumption decision and change in consumption decision due to change in price has been analysed.

a.Budget constraint: Income = cost of salad + cost of smoothies

48 = 8 * salad + 3 * smoothie

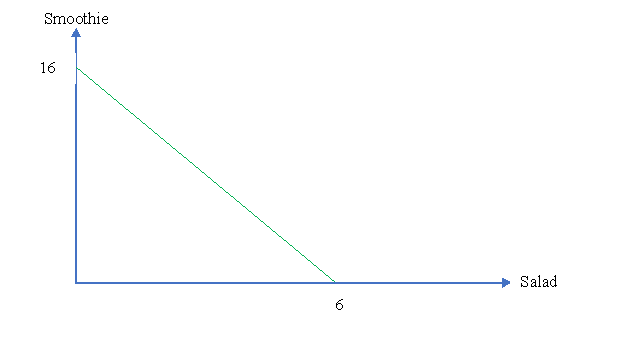

Now, if Misha, allocate all her budget into salad, then she can purchase salad: 48/8 = 6 If Misha, allocate all her budget into smoothie, then she can purchase smoothies: 48/3 = 16

Figure 2: Budget constraint

As per the figure 2, it can be seen that the budget constraint of Misha is represented by the downward sloping straight line in green colour, where she can buy 6 salad or 16 smoothies.

b.Opportunity cost is representation of the lost opportunity due to not doing one action instead of action done.

Opportunity cost of purchasing one more smoothie is: 6/16 = .375

Opportunity cost of purchasing one more salad is: 16/6 = 2.66

c.Optimal consumption is made when the slope of indifference curves equates with the slope of the budget line.

Slope of indifference curve = Marginal utility of salad / Marginal utility of smoothies

Slope of budget line = Price of salad / Price of smoothies

Hence, optimal consumption decision can be made when,

Marginal utility of salad / Marginal utility of smoothies = Price of salad / Price of smoothies

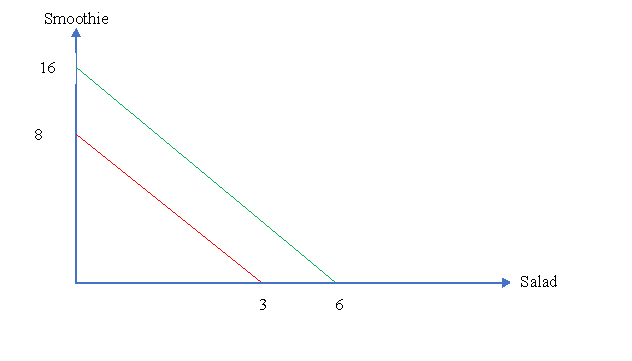

d.If income falls by $24, then new cost of lunch for Misha will be: $48 - $24 = $24

At this budget, Misha can purchase salad = $24/$8 = 3 salads

Misha can buy smoothies = $24/$3 = 8 smoothies

Hence, the new budget constraint will be reduced and will be represented by the red line in figure 2.

Figure 3: change in budget constraint

As per figure 3, budget constraint become halved for Misha as it was initially as the budget has become halved.

At the new budget line, it is not possible that Misha consumer more salad than previous situation as with the new budget, she can afford only 3 salad.

Answer to question 4:

|

Quantity |

Price |

Total Cost |

Total Revenue |

Marginal Revenue |

Marginal Cost |

Profit |

|

0 |

$6 |

$9 |

$ - |

$-9 |

||

|

1 |

$6 |

$11 |

$6 |

$6 |

$ 2 |

$-5 |

|

2 |

$6 |

$13 |

$12 |

$6 |

$ 2 |

$-1 |

|

3 |

$6 |

$16 |

$18 |

$6 |

$ 3 |

$2 |

|

4 |

$6 |

$19 |

$24 |

$6 |

$ 3 |

$5 |

|

5 |

$6 |

$25 |

$30 |

$6 |

$ 6 |

$5 |

|

6 |

$6 |

$30 |

$36 |

$6 |

$ 5 |

$6 |

|

7 |

$6 |

$45 |

$42 |

$6 |

$15 |

$-3 |

Answer to question 5:

a.Fixed costs are the fixed expenditure that do not change over time depending upon the level of the production in the short run. In long run also fixed cost may not change depending upon the nature of business. Fixed cost also does not depend on the level of production rather it changes depending upon the nature of business, change in technology, change in company assets etc. hence, fixed costs, in case of the zero production by the firm can be positive and it is inherent expense of the business and it cannot negative. However, depending upon the business and the asset allocation by the business, fixed cost can be zero.

As the example of the fixed cost, cost of machinery, cost of manufacturing unit operation can be considered for the Coca Cola company.

b.Variable cost as the name suggest is the changeable cost of production that company bears when then produce goods or service. Based on the level of production, variable cost increase and decrease and production level is the only factor that influence the variable cost. If the company produces higher amount of output at any given time compared to other time, then the variable cost will be higher. Hence. Production amount and the variable cost has positive association between them.

As the example of the variable cost of the firm, cost of raw materials can be considered for the Coca Cola company. Based on the level of production, firm need to purchase high or low amount of raw materials that results in higher or lower expenditure by the firm which is not fixed over the time rather fluctuate depending upon level of production.

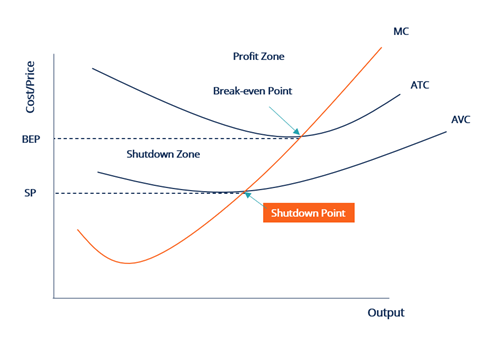

c.Fixed cost and variable costs are crucial element in making shut down decision by the firm. Firms calculate their total cost by summing the fixed cost and the variable cost and based upon the same, firms take decision of shutting down firm. If the firm makes no economic profit through its production and it is not able to cover its Average Variable Cost (AVC) through its operation, then at the point where, lower section of the AVC curve intersect the Marginal Cost (MC) curve, is the shutdown point (Barney and Mackey 2018). As the figure 4 demonstrates; when the firm AVC, intersect the MC curve at lowest point, then that point is shutdown point in short run.

Figure 4: shutdown point

At the shutdown point, firm fails to cover its variable cost also. However, above this point up to breakeven point, firm is able to cover its variable cost, though not able to cover the total cost; at this point firm faces sustainable operation and intersecting point of average total cost curve (ATC) with MC is breakeven point. In the long run, firm shut down its operation when the firm fails to achieve its fixed cost and thus point below break even is considered as the shutdown point (Dean et al. 2020).

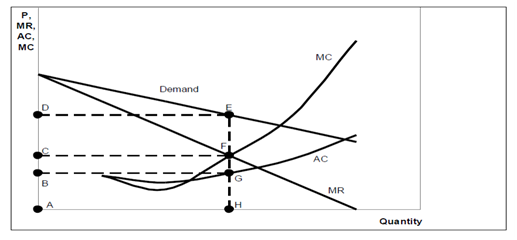

Answer to question 6:

In the monopoly market there is only one firm that operates and serve large number of buyers. Hence, product differentiation is present in the monopoly market and the competition in market is not present. In the monopoly, firms maximise its profit through producing at such a point where the MC equates with the Marginal Revenue (MR) curve (Komleh 2018).

Figure 5: Monopoly market

As per the figure 5, it can be seen that MR and MC equate with each other at point F, and the output produced is presented by the point H. With extension of the output line to demand curve, it intersect at E point. Hence the corresponding price of output is determined at point D. with cost of production at point B where the Average Cost (AC) intersect the output, profit is represented by the BDEG portion of figure 5.

Answer to question 7:

Monopolistic competition is a market situation where large number of sellers and buyers are present, however, each firm sells slightly differentiated product. In monopolistic competition, firms make independent decision and barrier to entry and exit is low (Noccoet al. 2017). Hence, in this type of market, though firms in short run makes supernormal profit, however, in long run they earn normal profit. As the number of competitors in the monopolistic market is high, thus competition is high and as the product are almostidentical but not perfect substitute, thus firms consider advertising as main strategy to demonstrate uniqueness. Moreover, in the monopolistic market, information is readily available, thus firms do not depend on each other to take strategic decision. Due to the nature of the market, firms in monopolistic market are price makers and they a face downward sloping demand curve (Thisse and Ushchev 2018). As the example of the monopolistic competition case of the restaurant can be mentioned. Though all the restaurants provide identical service, however, there is uniqueness due to the price of product, quality, place of restaurant and other factors that differentiate restaurants from each other.

On the other hand, oligopoly competition is a market situation where small number of firms operate in the market and large number of buyers is present. Compared to the monopolistic competition, in oligopoly competition, firms are interdependent. Thus, when one firm takes first move of pricing change, then its closest rivals take steps accordingly to hold consumer and marker concentration (Maisyarah 2018). In case of oligopoly market, market leader takes initial step to change market situation and the other firms follow the path accordingly. As the number of firms is limited, hence market concentration in oligopoly market is high leading to high barrier for entry. Due to the nature of the market, partial information is available in the market and the firms are price makers. In oligopoly market, firms consider predatory pricing and depending upon whether price is increased or decreased, oligopoly firms face kinked demand curve.

As the example of the oligopoly market, case of the airline industry can be considered. In each airline market, there are few service providers and they provide homogenous service, however, differentiated by the unique value proposition in terms of service quality, ticket fare, etc (Zhou and Zhou 2019).

Economics AssignmentPart B:

Answer to question 8:

Article chosen for the present analysis was published on 19th October 2021 by thequint.com and it discusses about the fossil fuel market price situation in present time in India and how it stacks up against the other countries. Through the analysis, here a discussion has been made to produce a summary of the chosen article.

The articles start with setting the backdrop of the rising oil price in India during present time. As the article demonstrated, retail price of the oil and diesel in India has went up sharply in last one-year post Covid19 pandemic and it has crossed $1.33 price in all the cities around the state (Thequint.com 2021). The articles draw a clear depiction of oil price comparison during present time and 2014 when the present government came in charge of the state. With effect from 2017, as per the article, government linked the oil price with the market price and it made the fuel price go up and down on daily basis based on international oil price. At present time, oil price in India as per the article is calculated based on the factors like crude oil price, demand situation, tax and rupee dollar exchange rate. The article has showcased that during 2021 July barrel price of oil was $43.35 in international market and by October, it become $85. Rising international oil price is one of the main reasons of the sharp rise in the present oil price in India (Thequint.com 2021). Besides, central and state taxed has been increased exponentially as well. For instance, petrol price has faced 217% increase in the central tax, whereas, diesel has faced 69% tax increase (Thequint.com 2021). Post Covid19 surge in demand of the fossil fuel has also increased the price of the fossil fuel in the state. India being net importer of the fossil fuel as it imports four fifth of its fossil fuel requirement, depends largely on the international oil market situation. The article has also demonstrated that the inability of the government to handle the oil price increase and now how central taxes on oil has impacted the price of the oil in India.

Answer to question 9:

The article discusses about the oil price situation of the Indian market in present time. As per the article, it has been found that oil market in India during 2014 was controlled by the government, however, presently it is market linked and price is decided by adding cost of purchasing petrol from OMCs, excise duty, commission of dealer and VAT. As per the analysis, it has also been found that there are sellers in the market like BPCL, IOCL, HPCL, CPCL, and private companies like Reliance, Nayara energy ltd which operates in the Indian market. Hence the market is oligopoly in nature where limited number of producers are available whereas the number of buyers is large. As the products each seller sales are identical, there is no price discrimination; however, price varies from state to state depending upon the tax levied by the local government. Moreover, cost of transportation is another factor that influence the local price of the fossil fuel in the Indian market. Compared to the international oil price in different market, it can be seen that oil price in India is slightly on higher side where price varies from $1.33 to $1.5 (Thequint.com 2021). Here the article states that the oil price prior to 2014 was controlled by the government and revised in every 15 days (Thequint.com 2021). During that time though market players were present in moderate number, however, price was largely decided by government considering its socialists approach. Presently, firms consider predatory pricing in case of premium oil where octane number is high leading to higher fuel efficiency. In absence of the government control over the market, firms follow the international pricing of crude oil making the fossil fuel market in India a market driven place. As per the article moving from government control to open market operation-based market, oil price India has started to increase largely. Moreover, post Covid19 surge in the demand, changing oil price international market and increasing tax rate are major reason of steep rise in the price of oil in India. The article has showcased that during 2021 July barrel price of oil was $43.35 in international market and by October, it become $85 (Thequint.com 2021). Rising international oil price is one of the main reasons of the sharp rise in the present oil price in India (Thequint.com 2021). Besides, central and state taxed has been increased exponentially as well. For instance, petrol price has faced 217% increase in the central tax, whereas, diesel has faced 69% tax increase (Thequint.com 2021). Hence, though the oil market in India do not have curtail present, however, lack of government intervention in market and factors influencing demand and supply of oil makes the oil price go high at a high rate post Covid19.

Reference:

Barney, J.B. and Mackey, A., 2018. Monopoly profits, efficiency profits, and teaching strategic management. Academy of Management Learning & Education, 17(3), pp.359-373. https://sci-hub.se/10.5465/amle.2017.0171

Dadkhah, A. and Vahidi, B., 2018. On the network economic, technical and reliability characteristics improvement through demand-response implementation considering consumers’ behaviour. IET Generation, Transmission & Distribution, 12(2), pp.431-440. https://bmcpublichealth.biomedcentral.com/articles/10.1186/s12889-017-4098-x

Dean, E., Elardo, J., Green, M., Wilson, B. and Berger, S., 2020. How Perfectly Competitive Firms Make Output Decisions. Principles of Economics: Scarcity and Social Provisioning (2nd Ed.). https://openoregon.pressbooks.pub/socialprovisioning2/chapter/11-2-how-perfectly-competitive-firms-make-output-decisions/

Herrera, A.M. and Rangaraju, S.K., 2020. The effect of oil supply shocks on US economic activity: What have we learned. Journal of Applied Econometrics, 35(2), pp.141-159. https://www.cireqmontreal.com/wp-content/uploads/2019/09/herrera.pdf

Komleh, R.A., 2018. A comparison between conditions of perfect competition market and pure monopoly in supply, demand and equilibrium. https://www.researchgate.net/profile/Ramin-Abolghasemi-Komleh/publication/329117859_A_comparison_between_conditions_of_perfect_competition_market_

and_pure_monopoly_in_supply_demand_and_equilibrium/links/5d4090d74585153e59300467/

A-comparison-between-conditions-of-perfect-competition-market-and-pure-monopoly-in-

supply-demand-and-equilibrium.pdf

Labandeira, X., Labeaga, J.M. and López-Otero, X., 2017. A meta-analysis on the price elasticity of energy demand. Energy policy, 102, pp.549-568. http://diana-n.iue.it:8080/bitstream/handle/1814/40870/RSCAS_2016_25.pdfsequence=3&isAllowed=y

Maisyarah, R., 2018. Analysis of the Determinants Competition Oligopoly Market Telecommunication Industry in Indonesia. KnE Social Sciences, pp.760-770. https://knepublishing.com/index.php/Kne-Social/article/download/3170/6720

Nocco, A., Ottaviano, G.I. and Salto, M., 2017. Monopolistic competition and optimum product selection: why and how heterogeneity matters. Research in Economics, 71(4), pp.704-717.

http://eprints.lse.ac.uk/83567/1/Ottaviano_Monopolistic%20competition.pdf

Pasha Zanousi, M. and Shahbazi, K., 2019. Entry into the Complementary Good and Service Markets in a Foreign Country, with Network Effects. Economics assignmentJournal of Economic Research (Tahghighat-E-Eghtesadi), 54(4), pp.847-873. https://jte.ut.ac.ir/article_74170_1a826bb79f0dba2f09e72ef791776d08.pdf Rostek, M. and Yoder, N., 2020. Matching with complementary contracts. Econometrica, 88(5), pp.1793-1827. https://www.ssc.wisc.edu/~mrostek/ECTA16686.pdf

Thequint.com 2021. Fuel Prices at All-Time High: What's Causing the Surge How Is Price Calculated, TheQuint. https://www.thequint.com/news/india/how-are-petrol-prices-calculated-in-india#read-more Thisse, J.F. and Ushchev, P., 2018. Monopolistic competition without apology. In Handbook of Game Theory and Industrial Organization, Volume I. Edward Elgar Publishing. https://www.researchgate.net/profile/Philip-Ushchev/publication/314405154_Monopolistic_Competition_Without_Apology/links/ 5c4926cc458515a4c73c4de1/Monopolistic-Competition-Without-Apology.pdf

Yashkina, O., 2017. The optimal pricing strategy of the novelty product determined by function of price elasticity of demand. , 1(2), pp.123-134. https://mdt-opu.com.ua/index.php/mdt/article/download/20/26

Zhou, H. and Zhou, S., 2019. Pricing strategy of multi-oligopoly airlines based on service quality. Plos one, 14(6), p.e0216651. https://journals.plos.org/plosone/articleid=10.1371/journal.pone.0216651