Cash Generating Units in Business Accounting

Question

Task: Explain the various cash generating units in business accounting.

Answer

Part A: Impairment Laws

Introduction:

In terms of assets and cash generating units, Impairment loss may be defined as the different between carrying amount and reclaimable amount. The carrying amount can be calculated by subtracting the amount of depreciation from the asset value to be recognized in the company's financial report. Similarly, the amount to be reclaimed is calculated by subtracting sale price of asset from its fair value. This can also be measured by value being used, which is expected to result from the sale of assets in future cash flows. AASB 136 governs the totality of impairment loss, the calculation of impairment loss value and the necessary audits (Vanza et al., 2018).

Discussion: Companies that make profits are expected to adhere to the requirements of AASB 136 and IAS 36 to identify and document loss of impairment Whereas, non-profit organizations may refuse adherence with IAS 36 to acknowledge the asset's impairment loss. Impairment loss accounting standards apply to all of the companies' fixed assets, including goodwill (Sedki et al., 2018). The assets must be in the form of the system which are cash generating unit and excluding inventories, deferred tax capital, investments Assets and cash generating units must be impaired by the businesses if any sign of damage is expressed in the yearly valuation. These indices could be obtained externally, internally, or any appropriate affiliate or associated firms indicators. Externally originated indices include a steep drop in the asset's current value. If the materials technology, industrial market, economic situation and corporate laws are adversely affected, then the organizations are needed to impair the assets. In addition, if rate of interest or return are increased, firms must also acknowledge the reduction of impairment of resources and cash generating units (Sacer et al., 2016). External origin metrics that allow companies to impair assets which would include financial results or asset status are worse than anticipated. If the asset is permanently impaired, or if the whole item is redundant, then the lack of impairment must be acknowledged. Another measure of internal impairment is if the asset is not in working shape or in functional state. Therefore, if the number of liabilities shown in the independent balance sheet exceeds the figure shown in the consolidated balance sheet, the parental organization is needed to assess and accept the risk of impairment Therefore, if the volume of the dividend is greater than the "total overall profit of the division" then the entity is expected to calculate the setback of impairment in compliance with AASB 136 (Carlin & Finch, 2011).

The company is expected to determine the retrievable cost of the impaired property before assessing the impairment damage. Moreover, impairment in every fiscal year has to be investigated for impairment in the case of fixed assets that may have a useful life to an indeterminate period of time. In fact, in the situation of welfare, for every fiscal year, the impairment must be checked if its service life is reduced or limitless (Bond et al., 2016). Retrievable cost is deemed to be greatest among the value in use and the fair market value minus selling expenditures. In addition, the cost of the impairment damage is measured by subtracting from its retrievable sum the bearing cost of the property. If the bearing number exceeds the retrievable amount then the discrepancy value is called a loss of impairment It is reported for the assets that were reassessed in the accounting records in the financial statements. In addition the level of impairment loss must also be modified to the deterioration or amortization valuation of the asset (Maffei, 2016)

Since it is not possible to evaluate the retrievable value of the assets, the calculations to find the loss of impairment assets are done. In this scenario, the retrievable sum can be calculated by taking into account the cash-generating unit for the same asset (Linnenluecke, et al. 2015). As example, the goodwill that companies acquire as a culmination of mergers and investments must be transferred to the cash-generating unit The calculation of impairment losses of cash-generating unit resources is comparable to those for all depreciable working capital. Upon reducing the amount of impairment deterioration, the resources in the cash generating unit must be distributed proportionately (Schwarzbichler et al., 2018)

To complete the analysis of the asset impairment factors, the companies also had to evaluate the indices to mitigate the impairment loss. This analysis shall be carried out at the investigating date with the exception of the goodwill review. If the criteria that assess the state of impairment appear to have changed then only acknowledgment of impairment or restoration can be extended to the resources. The company is expected to quantify the amount of reversing and remove the same which was previously recorded (Vogt et al., 2016).

Following AASB 136 standards and regulations, organizations are mandated to disclose the details on loss of impairment as per paragraph 126. In the financial reports, transparency about the category of every asset, extent of impairment loss and level of reversing needed. The firms also had to report the incidents and factors that caused the assets to be affected along with the details about the asset's existence. In fact, the companies are also mandated to submit assessment methods of tangible and intangible assets reporting the life span of such resources (Schatt et al., 2016)

Conclusion

It can be inferred from the analysis of impairment loss that it represents the substantial economic productivity of the businesses ' resources. Because the asset's productivity and usefulness decreases with the continuous use in business operations, calculating this value is essential. Correspondingly, "AASB 136 on asset impairment" governs the measurement of impairment loss as well as the criteria of considering impairment loss assessment. During the financial year, organizations should assess and report the impairment loss metrics taking into account the external and internal factors. Business accounting assignments are being prepared by our accounting assignment help experts from top universities which let us to provide you a reliable online assignment help service.

Part B: Journal Entries

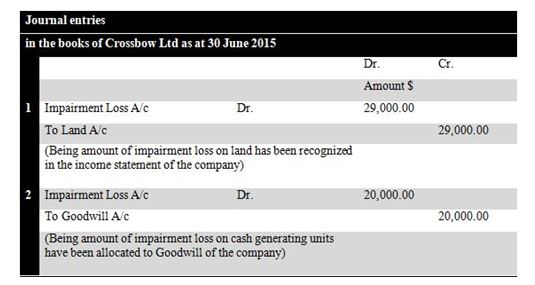

Table 1: Journal Entries

(Source: Made by Author)

Working

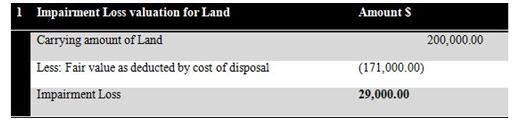

Table 2: Impairment Loss of Land

(Source: Made by Author)

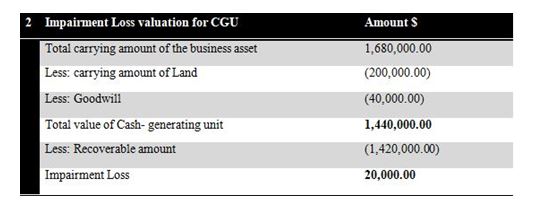

Table 3: Impairment loss on CGU

(Source: Made by Author)

Important Points

There are measures of impairment as determined by AASB 136 on Impairment on Assets dependence on impairment. Therefore, in the current case, as of 30 June 2015, Crossbow Ltd evaluated measures impairment; the standards of ASSB 136 are relevant for assessing and acknowledging the effect of the impairment on assets.

By subtracting the retrievable cost from the bearing sum, impairment loss is assessed as per the AASB 136. In addition, the retrievable sum is measured as greater in use-value or as a fair value minus the disposal value (Zhuang, 2016).

The cost of property use is not given in the case of Crossbow Ltd., so the fair value diminished by the sale expense is regarded as a retrievable value. In addition, the bearing amount of land on June 30, 2015, is greater than the retrievable cost, so it is important to consider the impairment loss.

The guidelines in AASB 136 specify the level of impairment for the cash generating unit to be accepted and the quantity of loss to be distributed on an equitable manner. Nonetheless, the amount of the deficit is first assigned to Goodwill and afterwards the amount of the surplus to be distributed towards the other asset depending on its bearing cost (Saggu et al., 2016).

At 30 June 2015, the gross bearing value of Crossbow Ltd's capital rose to $1,680,000 which should be decreased by Land and Goodwill. The impairment loss would be based on the cash-generating unit's net value which is greater than the firm's projected retrievable value. In addition, the sum of $20,000 impairment loss would first be assigned to Goodwill, but since the whole impairment loss has also been assigned to Goodwill, the allocation for certain assets could not be made.

References

Bond, D., Govendir, B. & Wells, P., 2016. An evaluation of asset impairment decisions by Australian firms and whether this was impacted by AASB...

Carlin, T.M. & Finch, N., 2011. Goodwill impairment testing under IFRS: a false impossible shore? Pacific Accounting Review, 23(3), pp.368-92.

Maffei, M., 2016. Amortization and Depreciation. Global Encyclopedia of Public Administration, Public Policy, and Governance, pp.1-7.

Sacer, I.M., Malis, S.S. & Pavic, I., 2016. The Impact of Accounting Estimates on Financial Position and Business Performance–Case of Non-Current Intangible and Tangible Assets. Procedia Economics and Finance, 39, pp.399-411.

Saggu, R. et al., 2016. Astroglial NF-kB contributes to white matter damage and cognitive impairment in a mouse model of vascular dementia. Acta neuropathologica communications, 4(1).

Schatt, A., Doukakis, L., Bessieux-Ollier, C. & Walliser, E., 2016. Do goodwill impairments by European firms provide useful information to investors? Accounting in Europe, 13(3), pp.307-27.

Schwarzbichler, M., Steiner, C. & Turnheim, D., 2018. Impairment of Assets (Fixed Assets and Goodwill). In Financial Steering, pp.343-70.

Sedki, S.S., Posada, G.A. & Pruske, K.A., 2018. Differences Between US GAAP and IFRS in Accounting for Goodwill Impairment and Inventory: Tax Treatment Under the Internal Revenue Code. Journal of Accounting and Finance, 18(4).

Vanza, S., Wells, P. & Wright, A., 2018. Do asset impairments and the associated disclosures resolve uncertainty about future returns and reduce information asymmetry? Journal of Contemporary Accounting & Economics, 14(1), pp.22-40.

Vogt, M., Pletsch, C.S., Morás, V.R. & Klann, R.C., 2016. Determinants of goodwill impairment loss recognition. Revista Contabilidade & Finanças, 27(72), pp.349-62.

Zhuang, Z., 2016. Discussion of ‘An evaluation of asset impairments by Australian firms and whether they were impacted by AASB 136'. Accounting & Finance, 56(1), pp.289-94.

Get Top Quality Assignment Help and Score high grades. Download the Total Assignment help App from Google play store or Subscribe to totalassignmenthelp and receive the latest updates from the Academic fraternity in real time.