Auditing Assignment Evaluating Sarbanes Oxley Act & Audit Fee Determination Of Woolworths

Question

Task:

Auditing AssignmentSpecifications

This assignment aimsto enhance students’ critical thinking skills and higher order application abilities by researching and analyzing a demand for assurance, audit fees determination and good governance practice. Students will need to propose and document demand for audit and assurance services, explain techniques of determination audit fees and practical application of good governance.

Students will have to research relevant academic literature, including related organisation websites and write intext citations in this assignment. Additionally, they will demonstrate understanding and critical evaluation of the Australian financial governance reporting environment and its currentregulatory framework, and recommend future directions to the Australian governance principles reporting regulators.

Required Task:

Part 1: Demand adequate Assurance:

In 2002, the audit firm Arthur Andersen collapsed following charges brought against it in the United States relating to the failure of its client, Enron. Some other clients announced that they would be dismissing Arthur Andersen as their auditor even before it was clear that Arthur Andersen would not survive.

Required:

a. Explain demand from audit and assurance services under Sarbanes- Oxley Act (2002)

b. Explain auditors understanding of corporate governance revision, update and arguments after SOX Act (2002)

Part 2: Audit Fees Determination and ASX CGC Principles

All companies are required to disclose in their annual reports the amounts paid to their auditors for both the financial report audit and any other services performed for the company.

Required:

a. Obtain a copy of a recent annual report (2019) from ASX Top 50 listed companies list (most companies make their annual reports available on the company’s website) and find the disclosures explaining the amounts paid to auditors. How much was the auditor paid for the audit and non-assurance, or other, services Explain your understanding about demand and supply theories of audit fees from this company

b. Explain your selected company’s (same selected company from question a) application of ASX CGC principles using Corporate Governance Principles and Recommendations (4th Edition) was released on 27 February 2019

Answer

Executive Summary

The report on auditing assignment aims to critically evaluate the Sarbanes Oxley Act and the determination of audit fee of Woolworths. SOX impose different alterations to the governance and regulatory environment through which additional disclosure, reporting of crimes and certification of financial results were focused. In light of this, the demand from audit and assurance is discussed. The second part of the report deals with corporate governance principles, and for the study, Woolworths, a giant retailer listed on the ASX is selected. The information reflects Woolworths' performance in the segment of corporate governance and the benefits it caused to the stakeholders.

Introduction

There has been a numerous corporate scandal that led to weakness in the firm's governance and auditing practice. It projects the weakness and frailties in controlling reliability, as ell integration to the stock market. The scandal led to an immense loss for the investors as the affected companies were eroded from the market. Such happening shook the confidence of the people in the stock market. The Enron Scandal of 2000 was one of the major white-collar crime engraved in American history. The scandal brought many matters to the forefront, and many officials were persecuted for the crime. The unethical policies and manipulation of Enron's documents led to the emergence of the Sarbanes Oxley Act of 2002, whereby the Securities and Exchange Commission enhanced the role. The SOX passage regulated the accounting firms through the management and the establishment of the internal control with the presence of proper reporting method of the control adequacy.

The report aims to provide an in-depth analysis of Australian financial governance reporting environment and the present regulatory framework. Instead of this, the Sarbanes–Oxley Act passed to restructure the corporate environment is discussed, followed by the determination of the audit fee and ASX corporate governance principles. The report is followed by the conclusion whereby it is known that the introduction of SOX leads to enhanced financial disclosure and corporate responsibility.

Part a

a. Demand from audit and assurance services under Sarbanes- Oxley Act

Corporate scandals and frauds led to the emergence of Sarbanes- Oxley Act that created radical and comprehensive changes in the public traded companies and strived to safeguard investors, thereby promoting the accuracy of disclsoures, hence signifying more record-keeping requirement and criminal penalties for the defaulters. Demand from audit and assurance service can be stated as the maximum under the provision of SOX (Setiany et al 2017). The major provision Section 404 needs companies to ensure that they have proper internal control over financial reporting and those that are properly tested, verified, and hence it signifies effectiveness. The external auditor is assigned with the responsibility for the approval of the assessment that supports management report concerning internal control over financial reporting.

New practices were brought to the forefront to ensure managers to test their controls and internal audit that has traditionally been the department highlighting the assessment of risk and management in the financial and governance domain. The internal auditor is allocated with the task and aids in the proper control and audit (Oussii&Boulila 2018).The SOX led to the higher demand for audit assurance and services whereby the corporate governance was strengthened. The audit committee attains huge leverage over checking the accounting decision of the management. Greater evidence would be required during the performance of the integrated audit, and hence more emphasis will be required for the effectiveness of control. The evidence can be used to lessen the nature, timing, and level of substantive procedure in performance and conducting the audit (Anderson 2010).

As seen from the discussion, SOX's presence led to the emergence of higher financial disclosure and hence, the demand from audit and assurance enhanced. The accuracy, as well as financial report validity, resides upon the internal control mechanism. Disclosures of transaction linked to management and stockholder are mainly needed that leads to complete transparency, and the principles have highlighted the same. Further, the principle consists of corporate fraud accountability and hence to attain this high level of audit and assurance is vastly needed. The act identifies the offences and leads to individual penalties. Therefore, it brings a vast group of change because strengthening the penalty is ultimately linked to higher audit and assurance services (Parker 2019). Thereby, SOX's introduction is related to higher demand for audit and assurance and the short revision of the guidelines. It emphasises that the adjustment is made to present the financial statements properly and fairly. The stringent control brings a higher level of disclosure and presentation of the information in an appropriate way. Going by the new Sarbanes–Oxley Act, the audit firm must turn around the audit partner every five years (EY 2015). Hence, Section 103 of the Act leads the public accounting firm to maintain and prepare a period that is lesser than seven years. On the other hand, section 104 provides the advisory board to maintain and review all papers of audit for five years from the fiscal year-end (Gay &Simnett 2018). Hence, it is clear from the discussion that the SOX lays adequate emphasis on the audit and assurance, thereby leading to more demand.

b. Auditors understanding of corporate governance revision after SOX Act

Sarbanes-Oxley has completely restructured the concept of corporate governance. Regulation compliance, related costs and enforcement have a far-reaching influence on the public corporations. The major changes appeared to be beneficial, and with the new requirements, the negative consequences are overcome. One of the noteworthy changes seen in the international companies is that there have been changes in the public offering; hence only the genuine companies can undertake the public offering. Corporate governance is the mechanism whereby the corporation is managed in a manner that helps to operate it successfully, with the introduction of SOX< Section 409 was introduced that forces the public companies to report all information that is material to the shareholder, as well as the public. The said includes research and development irrespective of the success (Gay &Simnett 2018). Weak or failure projects were not reported by the public companies and hence it lead to inaccurate disclosure. The responsibility has now transferred to the private companies that are limited by less capital and low resources. SOX has led to stringent requirement, and that has ultimately influenced the process of corporate governance (Grayston 2019). Even private companies are needed to understand the rules and regulations if they hope to go public in the upcoming future. If it is foreseen that the private company will be merged with public, then compliance is of utmost necessity. Government contract even requires compliance that has raised the level of corporate governance. Hence, with the introduction of SOX, there has been a higher level of reliance on the process of compliance.

The initial is the corporate law that concerns self-dealing, transaction of a related party, setting up of executive compensation, and the extraction of private advantage from the management position (Grayston 2019). For instance, the chief executive of a prime Company sells the personal business which he owns. ABC company law does not restrict the transaction but needs that to be true and fair. Post SOX, the governance changed that involved financial disclosures and other investors. Better information leads to better performance among the investors where the buy and sell were more refined. There were fewer bad decisions and fewer scandals. Many new rules altered the requirement of disclosure and hence strived to provide more effective action. The new governance standards strived to provide better accuracy and efficiency and the director incentives were provided to act in a diligent manner. The feedback received is used to adjust and improve the performance. Such principles help the directors to perform the functions effectively and not just related to evaluation and misbehavior (Guszcza et al 2020). Further, the SOX led to the emergence of new listing standards that need public companies to have a composition of independent directors on the board. Additionally, the new rules introduced key committees like an audit committee, compensation committee and a nominating committee. Hence, the introduction of SOX or the aftermath of the SOX led to the refinement of the corporate governance principle and practices (KMPG 2020). However, the SOX is not free from error because some of the costs were one time like recruiting independent directors and hiring law firms. Some expenses were incremental in nature like holding regular session of executive, the independent director and requirement to pay the directors for heavy workloads and perceived risk. The costs applicable to large accounting firms from lucrative to normal audit service are huge, and the compliance with the regulation of 404 regarding internal control is dramatic. The SOX-linked corporate governance alterations might threaten the important role of boards as management participants against evaluation, but it is clear that the results are equally divided between the pros and cons.

Part 2: Audit Fees Determination & Corporate Governance

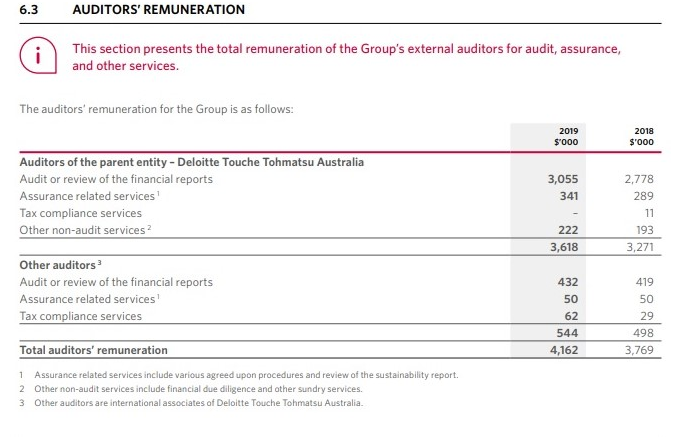

a. Non-audit services

During 2019, the company auditor that is Deloitte Touche Tohmatsu Australia has performed various ancillary services apart from the statutory duties. The services were conducted by intimating the board during the period, and the normal benefits of the auditor was not hampered in the process. The auditor role and conduct were in tune with the Code of Conduct APES 110 Code of Ethics for Professional Accountants as there was no involvement in evaluating the review of the auditor's own work (Woolworths 2019). The details of audit and non-audit services with amount are given:

(Woolworths 2019)

The demand for audit services is a direct result of the involvement of the external stakeholders in the company. The stakeholders always vouch for accountability from the company in return to their devotion to the company.

Hence, the auditor's information should not be a disappointment nor vastly exceed the shareholder expectation. It suggests that the main function of the audit is to infuse credibility to the financial statements. Hence, the main service that the auditors are selling is credibility. The clients demand credibility and therefore are higher in demand. Audited financial statements supply depends on the auditors as it is upon them to check the credentials(Woolworths 2019). The users gain benefit from the audited financial statements and hence is highly demanded. The quality of decision making is vastly improved with the services; thereby it is much in demand.

b. Corporate Governance of Woolworths

The Corporate governance statement emphasizes the main corporate governance principles and practices of the group during the year 2019. Woolworths has adhered to all the ASX Corporate governance principles and Recommendation recommendations throughout the entire period (Woolworths CG 2019). Moreover, the same has been provided on the company’s website.

• Lay solid foundation for the Board

The Board role is to project the sustainable long term interest of the company. In this manner, the Board will be able to function with preciseness. This way, the board can be accountable to the shareholders for undertaking strategic decisions and enhancing the group's performance. At Woolworths, the Board is well aware that the development of sustainable growth strategy followed by the long term shareholder value needs goodwill, trust, team members, suppliers and support of the communities under which it operates.

• Structure the Board to be effective and add value:

The Board at Woolworths is of appropriate size and collectively contains the skills, knowledge and commitment of the industry under which it functions that helps it to discharge the duties that help to add value. The Board consider the fact that a variety of skills, background and experience among the directors is essentially needed for dynamic decision making and strong corporate governance. Considering the current and future strategic plans followed by the opportunities and challenges for the group, the Board evaluates the skills and experience of directors (Woolworths CG 2019). The Board even highlighted in the annual report of 2018 that an access to higher operating experience it the area would help the Board in attainment of the strategic aim of the group. Some of the major strategic aim followed by the company is:

(Woolworths CG 2019)

• Instill a culture of acting lawfully, ethically and responsibly

It is essential for a listed company to instill and enforce a culture that is based upon genuine law and act in an ethical manner. Woolworths is exposed to different strategic, operational and other risk related to finance (Woolworths CG 2019). To ensure that the group performs with effectiveness, the group has established an enterprise risk management framework which is linked to governance structure and provides a strong framework in the management of the material risk of the company. The risk management structure reflects the total principles and the roles of the risk management of the group.

• Safeguard the integrity of corporate reports: The company comprises of the audit committee that looks after the integrity of the financial reports. The corporate reporting process of Woolworths is laid as such that it looks after the internal control structure followed by the entity’s financial statement that projects the committee’s understanding and provides a genuine view of the financial information together with the company’s performance. Further, the committee deals with the accounting judgement appropriateness and choices exercised by the management in the preparation of the financial statement. Moreover, the appointment of the external auditor is made by the committee, followed by the fee payable to the auditor for audit and non-audit work.

• Timely and balanced disclosure

A listed company is needed to provide adequate disclosure of matter pertaining to the business and that which will influence the decision making of the investor. At Woolworths, the group provide the shareholders and the market with proper access to the desired information.

The disclosure policy of the company strives to attain compliance with proper disclosure on the regulatory needs, clarification of the accountability of the senior executives of the Woolworths Group, promotion of the investors’ confidence in the securities of the company. Further, the disclosure policy is regulated and ascertained ensuring that the correct information is provided to the public at large. Hence, it is clear that the entity ensures the board provides all correct material market information in a prompt manner.

• Respect the rights of the shareholders

Woolworths has been a forerunner in the transparency terms as it provides clear information on the corporate governance section supplied on the company's website. Hence, the shareholder's rights are valued as they can access the information about the entity and governance, proper communication and facilitation of the security holder meetings. Secondly, the company provides all the announcements to the ASX hence stressing upon the policy of disclosure, it provides notice of meetings to the security holders and other important documents (Woolworths CG 2019). Such information of the company is available at the website for a reasonable time span. Moreover, Woolworths have an investor relation program that aids in two way communication with the investors. The company has such an effective communication process that helps to receive and send information of the valuable information.

• Recognition and management of Risk

Woolworths is vulnerable to different risk in the area of operational, finance and compliance-related risk. The risk management framework contains the group policy of risk management and the ERM framework. The Risk management policy of the group projects the total principle of Woolworths approach to risk management (Woolworths CG 2019). As seen Woolworths sets, as well as communicate expectations for the framework of risk management and provides an oversight of the risk exposure followed by the risk-taking capacity of the group.

• Remunerate fairly and responsibly

The board of Woolworths has framed the remuneration committee that has three members and chaired by the independent director. It helps in the sound framework and leads to management of the material business risk. Remuneration is a major driver, and the committee helps to attract high quality directors and attract them. Further, the incentives for the executive directors and other senior officials influence them to help in the growth of the company without conducting any reward (Woolworths CG 2019).

Conclusion

It was not accounting that led to the major scandals such as Enron, Satyam and WorldCom rather, it was the set of unreliable financial statements ad fraud that led to the downfall. Amidst all these, the real loophole was missed. Reliable financial statements completely depend upon the effective internal control mechanism however; the effective internal control is also dependable on reliable management followed by a strong corporate governance mechanism. The aftermath of SOX led to enhanced disclosure and better compliance system. The benefit of SOX was seen in terms of managers accountability to act in the interest of the shareholders however the increased disclosure is coupled with higher compliance cost. On an overall basis, the SOX support the governance mechanism and helps in better performance of the firms. The selection of Woolworths and its performance in the field of corporate governance indicates that the recommendation laid down by the ASX corporate governance council is followed in a stern manner as all the principles are followed. Hence, it clearly emphasizes that the aftermath of the SOX led to more concentration on the corporate governance principles and the same has been highlighted in the annual report of Woolworths.

References

Anderson, A.W 2010, A practical approach to understanding audit risk, Account-Ability Plus, viewed 29 December 2020 https://www.kscpa.org/writable/files/AndersonAuditExpress/apracticalapproachtounderstandingauditrisk.pdf [22 April 2020]

EY 2015, Key Audit Matter: What they are and why they are important, viewed 14 September 2020 https://www.ey.com/en_gl/assurance/key-audit-matters--what-they-are-and-why-they-are-important Gay, G and Simnett, R 2018, Auditing and Assurance Service in Australia, McGraw-Hill Education (Australia)

Grayston, C 2019, Audit quality: is it time for a different approach viewed 14 September 2020 https://www.intheblack.com/articles/2019/02/01/audit-quality-time-for-new-approach

Guszcza, J, Rahwan, I, Bible, W, Cebrian, M and Katyal, V 2018, Why we need to audit algorithms. Auditing assignment Harvard Business Review, viewed 14 Septemberhttps://hbr.org/2018/11/why-we-need-to-audit-algorithms

KMPG 2020, Regulatory Audit, viewed 29 December 2020 https://home.kpmg/au/en/home/services/audit/regulatory-audit.html

Oussii, A.A. &Boulila, T.N. 2018, Audit committee effectiveness and financial reporting timeliness, African Journal of Economic and Management Studies, vol. 9, no. 1, pp. 34-55.

Parker, D 2019, Seeing audit quality in Australia in a new light. viewed 29 December 2020 https://www.intheblack.com/articles/2019/10/01/seeing-audit-quality-in-australia-in-a-new-light Setiany, E., Hartoko, S., Suhardjanto, D. &Honggowati, S. 2017, Audit Committee Characteristics and Voluntary Financial Disclosure, Review of Integrative Business and Economics Research, vol. 6, no. 3, pp. 239-253.

Woolworths 2019, Woolworths 2019 annual report & Accounts, viewed 29 December 2020 https://www.woolworthsgroup.com.au/icms_docs/195582_annual-report-2019.pdf

Woolworths CG 2019, Woolworths CG 2019, viewed 29 December 2020 https://www.woolworthsgroup.com.au/content/Document/2019%20Corporate%20Governance%20Statement.pdf