Analysis for Tesco using performance measurement assignment stratogies

Question

Task: How to assess Tescos using performance measurement assignment research methods?

Answer

Introduction

This performance measurement assignment focuses on critically analysing Tesco. Tesco is a British multinational company that is headquartered in Welwyn Garden City. It is the third largest retail company in the world of groceries and other merchandises in terms of gross revenue and overall income. The company is listed on the London Stock Exchange. The company was founded in 1919 and since then it has been in operations. It has more than 3000 outlets all over the world and has diversified into a large number of products over the years like clothing, footwear, furniture, toys etc. In this assignment we will discuss about the performance measurement strategies of Tesco (Abdullah & Said, 2017).

As per performance measurement assignment findings, Previously Tesco used to follow the balance scorecard performance measure method to assess its overall performance, however in 2013 it changed to a new strategy that is known as the Big 6 KPIs method for performance measurement. A balance scorecard is a strategic measurement technique that helps the companies to identify and improve their internal controls, that will help them in generating external outcomes. It helps the managers in keeping a track of the internal steps that are taken by the employees and then accordingly they can manage the outcomes. The balance scorecard strategy is divided into four sections that includes – financial, customer, internal business, and innovation. The overall performance of the company is measured on the basis of these four categories and necessary steps are taken to improve the overall performance of the company based on these four measures. It is a well structured and is used worldwide by the managers to get better insights into the internal controls of their companies and it also helps in taking better decisions in the future (Alieid, 2016). It also used the steering wheel along with the balance scorecard that had a 90-degree arc that represented the four balance scorecard areas of focus. Tesco use to use this technique previously in order to access their overall performance and take steps accordingly however in 2013, their mid-year profit showed a downfall of more than 23% and since then Tesco changed its strategy and started using the Big 6 KPIs in order to access their performance.

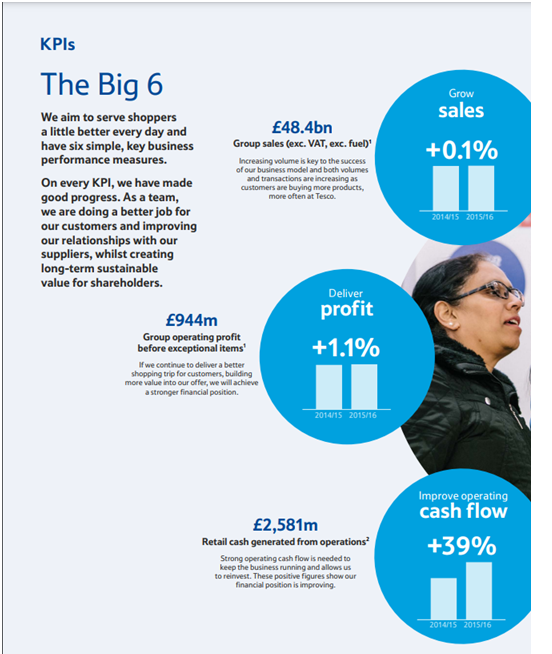

The Big 6 KPIs included six key performance indicators that measured the entire performance of the company. The key performance measurement assignment indicators are values that measures the overall effectiveness of a company in terms of achieving its business objectives. In case of Tesco, the 6 KPIs are – Sales, Profit, operating cash flow, customer that recommended the company and came back again and again, colleagues that recommend the company as a great place to work and shop, trusted partnership. After the company switched from the balance scorecard approach it started using these key parameters to measure the performance of such a big organisation all over the globe (Alkan, 2021). Now a detailed analysis on why the company made the switch and how was it beneficial for them in the long run is given below.

Analysis

In case of the balance scorecard the key metrics of the balance scorecard was further divided into sub-metrics for Tesco.

These metrics were-

Financial Perspective – growth in sales, maximisation of profit, management of the overall investment of the company.

Customer Perspective – pricing strategy, meeting customer demands, and quality over quantity.

Community Perspective – Being fair honest and responsible in its approach, environmentally friendly practices.

Operations Perspective – delivering consistently every day, better workplace practices.

People Perspective – Good team management, good leadership etc.

As per the performance measurement assignment research the CEO states that a steering wheel use to create a way of thinking that was common all through the organisation, and it gave a common blueprint for action all across. It helped in measuring the performance all across the organisation right from the leaders to that of the employees. Each store had its own steering wheel that helped in engaging the frontline workers in various corporate objectives. It helped in making strategy a part of everybody’s job, even the staff felt that they were part of the corporate performance measurement structure and tried to go above and beyond their jobs to solve in performance appraisal. In case of the steering wheel, it consisted of more than 40 KPIs and then they were further grouped and categorised under broad segments and responsibility and authority was segregated among different people for attaining these objectives (Bromwich & Scapens, 2016). However, when in 2013, the company’s half yearly profit fell by more than 23 percent, the management took a decision to reduce the number of KPIs so that they can focus on what will matter to them most and what is more crucial for the success of the company. The company felt that since there were so many indicators in the steering wheel it had become very complex, and it was difficult for the management to keep a note of all of them. At the end of the year reviewing each and every parameter was also a big task for the company and thus they thought that due to loss of controls and effective measures the company was suffering huge losses and in this way it was not doing well organically also and thus it made the switch to a simplified measure of performance measurement in which the number of indicators were less and they can easily check and decide which are the areas in which they need to put more effort so that overall results are positive and overall performance also improves. It helps in putting focus on what will matter most in future and also in the present (Lee, 2019).

The new KPIs that are introduced are very simple and broad, like sales, profit, cash flow that takes into consideration the growth in terms of numbers and helps the company in understanding what are the areas in which they need to look in if there is any depletion in the overall profit or sales of the company (Yeates & Keoghan, 2019). Thus, on this performance measurement assignment we establish Tesco is focusing on what will eventually matter to any organisation that is to earn profit and create wealth for its shareholders. The other three KPIs focuses on customer, colleagues, and trusted partnership that the company has built during that year. Every company must be customer centric as that forms the base of any organisation, thus in this category the company focuses on how they can improve the performance of the company, how many repeated customers are they having, how many customers are recommending them, all this will help in the growth of the company and is an important parameter for success of the company (Michaela, 2017). The next category is of the colleagues, it is important to have a great employer employee relationship, good working environment, and then only employees will work diligently for the company, various parameters are accessed in this category like employee retention ratio, how many employees are referring others to work for the company, other redressal and appraisal policies that would help the employees to put forward any issues that they face in the company. The last category is of trusted partnership, it is important to build such partnership that would help in strategic and organic growth of the company which will include mergers and acquisition, joint ventures, working with other trusted outsourcing companies etc. Thus we see building good partnerships are extremely important for the success of the company as that would help in achieving organisational growth. This is what we have seen in the case of Tesco where they have shifted their focus from small parameters that were extremely complex to such broad parameters that covers the whole organisation and takes into consideration both the qualitative and quantitative aspect for the success of the company (Sherwood, 2019). All these parameters are important for the success of the company and hence this shift was considered to be fruitful for the company as in the coming years we saw that the net profit also increased, and the management was able to have a better insight into the internal controls of the company.

Along with pros identified on this performance measurement assignment there are certain cons also of having this strategy in place which includes that since it is very limited in number, the overall control is also very high level that is needed. The main challenge is to communicate all this throughout the organisation. For example: The aim of the company is to improve the cash flow, this will be important for the board members, but for people who are working at the down of the ladder, this will not make any sense because they will not understand how they can contribute in improving the cash flow for the company. The same thing will apply in case of building good partnerships, because an employee who is working at the store will not understand what such partnerships are and how can he be pivotal in helping the company to achieve that (Yadao, 2018). Thus, we see that the level is high, hence the management needs to put more effort in communicating the same to members and employees even at the lowest level of the ladder, because for achieving the long-term objectives of the company all the employees even though they are at the manager level or at the store level, they need to work together. The overall operational objectives are also less in such KPIs and hence people who are more motivated when they work for certain targets will not be as concerned to achieve these KPIs, as long-term goals will not be attractive for them, they will not understand how customers recommendation will play an important role for the company as it is of no use for them. It is the operational objectives that will help in getting the stuff done (Wang, 2019). So these are few of the drawbacks in comparison to the old steering wheel strategy of the company. It can also be seen that steering wheel was more visually appealing as it captured all the key objectives of the company in a single picture and hence all the employees, managers were aware what do they need to do, it was easy to communicate and understand. It was a great visual reminder of what was important for the organisation, for the employees and even the results can be show cased in the same manner in that organisational chart and even that helped in understanding what are the areas in which the leadership needs to put more efforts. If we see the overall effect of the changes it was seen that long term goals were clearer, and the management did not had to spend time on achieving or looking after smaller objectives that did not matter in the long term. Even policy formation was easy even though the process took a long time now because the horizon was boarder but it had to be segregated into few categories only so it was easy to divide the responsibility and authority among the leaders that would help them be to be responsible for their own sector and set benchmarks or criteria that the management or the employees need to achieve at the end of the year (Werner, 2017). Every year in the annual report of the company, there is a separate section highlighting the KPIs of the company and the year end results in comparison to the previous year are also highlighted. This helps the management and the users of the financial statements in understanding how well the company has performed, what are the areas in which it might need changes and what are the areas in which it has improved in comparison to the previous year. A snapshot from the annual report has been attached on this performance measurement assignment for better understanding.

Source : Tesco Annual Report 2016

Source : Tesco Annual Report 2016

Thus we see that the users of the financial statements and the stakeholders have a clear picture of how the company has done in the current year in comparison to the previous years and the management also have a clear picture on the areas in which they have failed, and they need to put more efforts and check controls so that long term goals are achieved and the objectives of the company is fulfilled. It also provides an insight on the efficiency of the management which is important for long term survival of the company (Werner, 2017).

Conclusion and Recommendation

Based on the above analysis, it can be said that both the performance measurement strategies are good and effective but what matters is what is the goal of the company. Every company has different goals and the level of every company is different, for small companies adopting a balance scorecard is easy and more economical as it will provide clear picture of what needs to be done and even people at the lowest level will know how they can contribute to make the company a success. For companies like Tesco in which the area of operation is so huge it is not possible to align each and every employee or every store to achieve some common goals and having so many parameters creates a lot of issues and is very time consuming and complex, thus it is good to have broad categories with fewer parameters so that end goals are achieved and even the management has a clear perspective and accordingly they have devote their time. Fewer categories also means better controls, better regulations and that would be extremely helpful in the long run for increasing the overall profitability of the company and achieving the end goals of the company. Thus it can be said that Tesco as a multinational company has done a great job by shifting their strategy and that would help them in the coming years in better performance evaluation and these categories can again be streamlined as and when needed. So we see that long term goals are achieved and the overall profitability has also increased since 2013. The company made this switch as per performance measurement assignment guidelines thus making this switch was beneficial for the organisation and other companies can also resort to the same in case they want to increase their overall efficiency.

References

Abdullah, W. & Said, R., 2017. Religious, Educational Background and Corporate Crime Tolerance by Accounting Professionals.

State-of-the-Art Theories and Empirical Evidence,performance measurement assignmentpp. 129-149.

Alieid, E. E. M., 2016. The Role of Accounting Information Systems in Making Investment Decisions. Internal Auditing & Risk Management, 11(2), pp. 233-242.

Alkan, B., 2021. Real-Time Blockchain Accounting System As A New Paradigm. Journal of Accounting and Finance, pp. 41-58.

Bromwich, M. & Scapens, R., 2016. Management Accounting Research: 25 years on. Management Accounting Research, 31(1), pp. 1-9.

Lee, K.-J., 2019. The effects of social responsibility on company value: a real options perspective of Taiwan companies. Economic Research-Ekonomska Istraživanja , pp. 3835-3852.

Michaela, R., 2017. Contemporary Issues in Accounting. second ed. London: Wiley.

Sherwood, R., 2019. Intellectual Property And Economic Development. Newyork: Routledge.

Wang, D., 2019. Association between technological innovation and firm performance in small and medium-sized enterprises: The moderating effect of environmental factors. International Journal of Innovation Science, performance measurement assignment pp. 20-28.

Werner, M., 2017. Financial process mining - Accounting data structure dependent control flow inference. International Journal of Accounting Information Systems, 25(1), pp. 57-80.

Yadao, J., 2018. Forensic accountants and big data.

Yeates, C. & Keoghan, S., 2019. Big banks and accounting firms defend auditors' independence. Banking and Finance, 3 August, performance measurement assignment pp. 2-8.