Accounting Theory Assignment: Case Analysis of Assurance on Sustainability Reporting

Question

Task: To prepare this accounting theory assignment, you are required to choose a research article related to “Accounting Theory and Contemporary Issues” and analyze the selected research article using Accounting Theory Topics/Concepts.

Answer

Introduction

In this accounting theory assignment, the journal article named ‘Seeking legitimacy for new assurance forms: The case of assurance on sustainability reporting’ has been analysed and discussed. The topic which has been discussed in this research study is the process of getting the lawful acceptance of the auditing, assurance and sustainability accounting adopted by the assurance practitioners.

The research study that has been mentioned here will beanalysed from different aspects to understand its objectives, aim, and thetheoretical framework of it, research method and many other aspects like these. In the end, a conclusion will be given,stating the limitations and positive alternatives.

The research objective, hypothesis, research question used and analyze

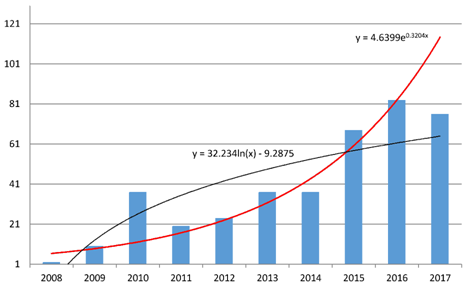

Figure 1: Growth of the sustainability Accounting

(Source: Taken from Zyznarska-Dworczak, 2018)

The research objectives

The research objective of this journal article is to understandhow assurance practitioner in sustainability reporting can and do seek to legitimize the sustainability assurance statements preparation practice with its principal users by collecting theoretical and empirical data .

Research Hypothesis

• The null hypothesis of this research is that the new sustainability accounting, assurance and auditing practices take the lawful acceptance of the different stakeholders of the business through its legitimation process.

• The alternative hypothesis of this research is that the new sustainability accounting, assurance and auditing practices do not take the lawful acceptance of the different stakeholders of the business through its legitimation process.

Research Questions

• In changing and enforcement of the sustainability assurance process within SAT, what is the purpose of the sustainability assurance and assurors’ experience?

• What type of evidence that is collected in the sustainability assurance process?

• How the relationship between client and assuror’s has changed by this process?

• What are the complications arising in the practical use of this process in term of materiality, stakeholders’ response and completeness of the reporting?

• What is the assurance engagement’s decision making process is?

• What is the nature of the drafting process of the assurance statements?

• What is what type of interaction happens between the clients and its stakeholders in post assurance period?

• What type of significant difficulties faced by the interviewees in undertaking the assurance engagements?(O’Dwyer et al., 2011).

Theanalysis of the theoretical framework or models adapted by the research article

The theoretical framework which has been adapted by this research article and being analysed includes making themes about different aspects and point of view of the different expertsabout the sustainability assurance practices which contradict to Power’s (2003a) point of view which found to these sustainability accounting practices to be ineffective for debates and dialogues. The first theme which has been made is called “legitimation of professional (audit and assurance) work inExpansion the jurisdiction of professional practice” and under this theme, the process of the legitimizing the work of this process has been analysed meaning how the work of the professional under this process establishing the cultural authority of the work. The second theme is called “The co-evolution of auditing practice and its legitimation with its stakeholders”which argues one point of view which states that the audit and assurance services and securing their legitimacy cannot be separately considered as they co-evolve. The third theme, called “clients legitimation seeking process’” stated that the financial auditing practice development and its progress had been affectedmainly by the attempts made to secure its legitimacy with the clients. The fourth theme is called “internal world legitimation seeking processes” and this stated that the getting legitimacy from the internal stakeholders wouldalso beingcritical for the assurance and auditing services. The fifth theme is called “Seeking legitimacy with the ‘non-client external world’” which states that the audit report plays a vital role in getting the legitimacy of the external stakeholders about sustainability reporting. The sixth theme is called “Refining the concept of legitimacy” which has defined legitimation as meeting the expectations of the social system value, beliefs and norms. The seventh theme of this research study is called “Types of legitimacy" which stated that the legitimacy could be of three types which are pragmatic, moral and cognitive. Then the last theme used in this research study is called “new practice legitimation process”, and this theme has identified different strategies which are used to get legitimacy and these strategies ranges from the conform, selection and manipulation.

The case study of this research study and the data basis used by the research for analysis

The case study in this research article includes analysis of the legitimation process of the auditing, assurance and sustainability accounting practices in the four professional service firms which are coded as SAT. The basis of the data that has been used by the research includes the responses that have been recorded in this research methodology from one specific professional firm of the four professional firms coded as SAT in this research and in that assessment three senior partners at first interviewed jointly twice which helped to make the framework of the research and then separate twelve interviews has been conducted between the researcher and the SAT staffs who are from different levels of management in the sustainability sections.

There are many strength and weakness of the data basis of this research, and these strengths and weaknesses will be discussed here. First of all, discuss the strengths of the data basis of this research. The first strength is that the in-depth interviews of the respondents have been taken in this research which reduces their point of view being manipulated or wrongly interpreted. The second strength of this data basis is that the help of the senior partner at SAT has been taken to formulate the framework of this research which can help to make the findings more relevant. On the other hand, there are many weaknesses found in the data basis. The first weakness is that framework of the data collection method of this research is too much influenced by the senior partners who have been interviewed, and this increases the chances of these findings being biased. Then again the sample size used to collect the data of this research’s findings has been very small and this also increases the chances of the finding of this research not being an accurate representation of the actual population in the market(Varoquaux, 2018).

The analysis of the research methods used in the theoretical framework

The research method used in the theoretical framework of this research study includes qualitative data as the qualitative data is appropriate for getting the finding of this case study. The data of this research has been collected by the establishing connection with a senior partner at SAT whom one of the researchersprofessionally. This lead to the meeting between one researcher and two senior partners of the firm who represent the head of departments in the assurance quality review and the Sustainability Section in which the current problem in the sustainability assurance has been discussed. Then another formal follow-up meeting was conducted in which another senior partner of the sustainability section and the two senior partners who were present in the first meeting were present in this meeting also. Then after the formal proposal was sent to the lead partner of the sustainability section, the key SAT staffs in the sustainability section were involved in this research. Therefore, the data collected in this research study is through initial detailedjoint interviews with senior partners and twelve detailed individual interviews with the staffs in the sustainability sections that belong to the different level of the management in the organisation. From the above assessment of the research data collection method, it has been assessed that the research method of this research is inductive in nature. This research is found to be inductive in nature as the basis of the research data has been formed from the detailed two interviews with the three senior partners meaning these senior partners point of view has a significant influence in the formation of the research data or what the research data will include. Therefore, it could be said three specific individuals point of view helped to form a framework which is accepted by the research as the framework which will be accepted by all for the sustainability accountability legitimation process in the market. Also, the data of this research include the response of twelve staffs of one of the professional service firm and this also is means that the response of these twelve individuals has been used to generalize the opinion of the total workforce in the sustainability accounting market. Therefore, the overall research data basis indicates that this research method of this research has been inductive, which mean the generalization of the specific observationsthat happened in this research (Jebb et al., 2017).

The analysis of research contributions the researchers have made concerning the research question and themes

The analysis of the research contributions shows that the researchers havea significant contribution to some aspects through its themes, but some research questions have not been adequately addressed in this research study. Let assess the contribution of the research regarding each of its research questions. The first research question of what is the perceived purpose of the sustainability assurance and assurors’ experience of the changing or updating and implementing of the sustainability assurance process within SAT has been adequately addressed as the overall data of this research has been based on the working of one of the SAT firm and overall process has been recorded in detail in this research study. The second research study which is what type of evidence that is collected in the sustainability assurance process has not been fulfilled in this research study as SAT management has refused to give the client data for further studies due to customer data protection which lead to the researcher not being able to gather much data about this aspect. The third question which is how the relationship between client and assurors has changed by this process has adequately addressed in this research as the process by which the assuror get the legitimacy of the client has been fulfilled analysed and described from different aspects like the legitimacy type that is given by the client is found to be pragmatic under this research, or it has been found that the strategies to gain legitimacy from the client include three types which are manipulation, selection and conform.

The fourth research question which is what are the complications arising in the practical use of this process in term of materiality, stakeholders’ response and completeness of the reporting has not be adequately addressed in this research as the research has been unable to gather working papers of SAT and this lead to the research not being effectively achieving this research question. The fifth research question is that what the assurance engagement’s decision making process has also not fulfilled fully as again working paper would have helped to understand what type of decision the assurance engagement requires. The sixth research question is what type of interaction happens between the clients and its stakeholders in post assurance period have not been focused upon in this research. Therefore, this research question has not to be achieved in this research. The seventh research question, which is what type of interaction happens between the clients and its stakeholders in post assurance period, has not been discussed in detail. Therefore, it is concluded that the research question has not to be met. The last research question which is what are the significant difficulties faced by the interviewees in undertaking the assurance engagements has been achieved through the article themes are the different issues faced by the assurors has been identified in this research and how these issues are addressed have also been discussed through the legitimacy strategies of this research study. Therefore, it can be seen that some research questions have been addressed in this research, and some have not.

The analysis of the research gaps

There is a significant research gap in this journal article, and the research gap of this journal article is that this research focused on mainly three elements or stakeholders of the sustainability assurance which are clients, external world excluding client and inside the world. These categorizations may seem to be useful, but these categorizations are generalizing very dynamic and different groups of people into one category, and this lead to this finding of this research not being adequate.

Another research gap of this research is that this research has only focused on the four significantprofessional service firms process of the legitimation of the assurance and auditing process, but the roles of the other small professional services firms have been ignored, and this increases the chances of the findings of this research being biased(McCudden et al., 2018). Also, in the current assurance and auditing service market shares in the global market shows that other than the four professional service firms discussed, some other firms are existing in the market which is increasing their presence and giving high competition to the discussed four professional companies which have been code SAT. Some of the new companies which have increased their presence significantly are Grant Thornton International Ltd, Moore Stephens International Limited, RSM International Association, Nexia International Limited, Binder DijkerOtte (BDO) Global and Mazars(Grandviewresearch.com, 2020). Therefore, the exclusion of these firms createsa significant gapin the findings of this research. The third gap of this research study is the lack of use of the quantitative data in this research study and this again create significant gaps as the quantitative measures could have helped to understand the quantify the different aspects of this legitimation process and help in better understand how different factor influence this process(Harding, 2018).

Discussion of the different concepts of legitimacy examined by the researchers and how they relate to the article themes

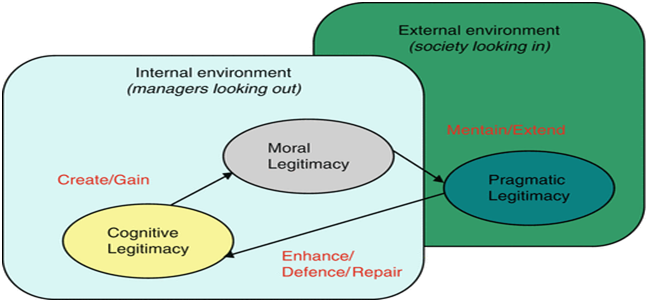

Figure 1: Legitimacy theory

(Taken from Deegan, 2019)

There are two different types of legitimacy examined by the researchers in this research study, and these three types of legitimation will be discussed here. The first type of legitimacy which has been discussed in this research study is pragmatic legitimacy, and under this legitimacy, the emphasis on the self-interest of the organisation constituencies are given meaning actions and behaviour of the organisation is taken into consideration to understand the impact of it(Adrot and Figueiredo, 2019). This type of legitimacy can be linked with the article's themes which are being made to understand the legitimacy process of the sustainability accounting among client like “Seeking legitimacy with ‘clients’” which stated that the financial auditing development had been profoundly influenced to get the legitimacy of the client. Also, this type of legitimacy has been linked with the interrelationship of getting approval from the inside world. The pragmatic legitimacy use with relation to the internal world can is linked with the research article theme called “Seeking legitimacy with the ‘internal world” which stated that getting the approval of the internal stakeholders is essential for auditing and assurance processes.

The second type of legitimacy which has been discussed is the moral legitimacy which emphasis on the fact that whether the action of the organisation is morally right or not to give legitimacy to a process(Reuber and Morgan-Thomas, 2019). The type of legitimacy has been used to understand the process of getting legitimacy from the external world excluding clients and this type of legitimacy can be linked with the article themes like “Seeking legitimacy with the ‘non-client external world’” which stated that the audit report plays a vital role in getting the legitimacy of the external world excluding the client as this can be related to the moral legitimacy as the audit report help to assess whether the organisation has behaved in the interest of its principal which are investors. The moral behaviour of an organisation will include the organisation behaving in the interest of its principal (Melé and Armengou, 2016). In this way, moral legitimacy is linked with the article themes which are related to the external world, excluding client.

The analysis of the mathematical or sociological models used

This research study has not used any mathematical model as the data of this research study is qualitative, but the sociological model has been used in this research study. The sociological model that has been used in this research include three elements or stakeholders of the sustainability accounting, auditing and assurance services which are clients, external world excluding clients and inside the world(Birdi and Ford, 2018). The sociological model used by this research includesanalysis of the different aspects of the legitimation process related to three elements of sustainability accounting like the type of legitimation, legitimation strategies adopted for the three different elements, action taken to implement the legitimation strategies and impact of those legitimation strategies. All these aspects include the sociological model used in this research study.

Conclusion

There are some significant limitations identified in this research study,and these limitations will be discussed here. The first limitation that the very small sample size has been used to gather the research findings and this small sample increase the chances of the research findings of this research being skewed or biased. The second limitation is that all research question solution cannot be achieved in this research study. The third limitation is the lack of quantitative data use which could have helped to better the finding of some aspects. The positive alternative which will be proposed to conduct further research on this topic is a mixed methodology which there will be the balance of both quantitative and qualitative data and also will include a bigger sample size for data analysis. It has been found out that the auditor or assurors gain legitimacy in different way from the different stakeholders. It has also found out that these stakeholders have high influence on the auditing process. After assessing the different aspects of this research, it has become doubtful what is the real goal of the assuror to get the legitimacy of different stakeholders including management and do an unbiased auditing and assurance service of the firm as both factors can be highly conflicting in nature(Talab et al., 2018).

References

Adrot, A. and Figueiredo, M.B., 2019. “Lost in Digitization”: A Spatial Journey in Emergency Response and Pragmatic Legitimacy.In Materiality in Institutions (pp. 151-181). Palgrave Macmillan, Cham.

Birdi, B. and Ford, N., 2018. Towards a new sociological model of fiction reading. Journal of the Association for Information Science and Technology, 69(11), pp.1291-1303.

Deegan, C.M., 2019. Legitimacy theory. Accounting, Auditing & Accountability Journal.

Grandviewresearch.com. 2020. Financial Auditing Professional Services Market | Industry Report, 2025. [online] Available at:

Jebb, A.T., Parrigon, S. and Woo, S.E., 2017. Exploratory data analysis as a foundation of inductive research. Human Resource Management Review, 27(2), pp.265-276.

McCudden, C.R., Jacobs, J.F., Keren, D., Caillon, H., Dejoie, T. and Andersen, K., 2018.Recognition and management of common, rare, and novel serum protein electrophoresis and immunofixation interferences.Accounting theory assignment Clinical biochemistry, 51, pp.72-79.

Melé, D. and Armengou, J., 2016. Moral legitimacy in controversial projects and its relationship with social license to operate: A case study. Journal of business ethics, 136(4), pp.729-742.

O’Dwyer, B., Owen, D. and Unerman, J., 2011. Seeking legitimacy for new assurance forms: The case of assurance on sustainability reporting. Accounting, Organizations and Society, 36(1), pp.31-52.

Reuber, A.R. and Morgan-Thomas, A., 2019.Communicating moral legitimacy in controversial industries: The trade in human tissue. Journal of Business Ethics, 154(1), pp.49-63.

Talab, H.R., Manaf, K.B.A. and Malak, S.S.D.A., 2018. Ownership Structure, External Audit and Firm Performance in Iraq. Social Science and Humanities Journal, pp.343-353.

Varoquaux, G., 2018. Cross-validation failure: small sample sizes lead to large error bars. Neuroimage, 180, pp.68-77.

Zyznarska-Dworczak, B., 2018.The development perspectives of sustainable management accounting in Central and Eastern European countries.

Sustainability, 10(5), p.1445.