Accounting Fraud Assignment: Discussion On Main Causes Of Committing Crimes

Question

Task: This assessment is designed to allow students to present and justify appropriate method(s) for a research project designed to address the research question posed. This assessment relates to Learning Outcomes a, b and d.

Based on the Research Question developed in Assessment 2, students should develop a research design aimed at providing insights and/or answers to the question. Students should make any recommended adjustments to the content of Assessment 2, based on feedback provided, prior to including it in Assessment 4.

This assessment requires students to choose and justify the most appropriate research design, clearly explaining WHY the chosen design will best answer the research question and is most appropriate in the specific circumstances. Students should clearly justify their recommended research and analysis methods.

Written Proposal : the proposal will contain the following information :

- Title page : including research title and student’s details

- Abtract : A brief summary of key information about the research (the research questions, the theory used and methodology plan).

- Research Background (revision version of Assessment 2)

- Research Questions and Research objectives (revision version of Assesment 2)

- Literature review minimum 20 peer-reviewd articles (including the four main articles used in Assessment 3)

- Research Design : describe type of research, research approach, type of data, data collection methods, data analysis methods and sampling plan.

- Ethical Consideration : address the five ethical consideration of human research

Note : Ethics Approval Form is not counted toward the word count of the assessment, only fill in this form if applicable. Include this form as appendices.

Answer

2. Executive summary

Employee theft along with corporate accounting and financial fraud is not uncommon anymore within the business units. It has been evidenced in the present report of accounting fraud assignment that such kind of activities majorly and negatively affects the operations and functioning of the company, which ultimately hinders success, growth and expansion of business. The study outlined within this accounting fraud assignment aims to identify the main causes which force the employees to commit such unauthorised crimes. In addition, different aspects of techniques and tools that if effectively integrated would help the management system of the company to promote motivation and encouragement within employees so that they would be dedicated toward the benefits and success of the company while avoiding any kind of unauthorised practices. To do the investigation for sustaining relevant finding, focusing on identifying the reason behind such accounting and financial fraud committed by the employee has been undertaken. Besides, the impacts of corporate accounting and financial frauds have been investigated in a wider manner. To raise the credibility and reliability of the study, both primary and secondary method associated under mixed methods of collecting data has been conducted. The ways in which the employees are motivated to execute accounting and financial fraud as well as unauthorised activities and how that leads the company to encounter with bad decision, which renders questions on the ethical consideration of the company in the market, will also be evaluated herein.

3. Research background

Introduction to the topic

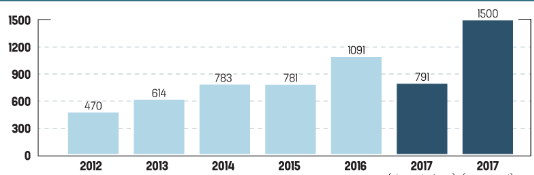

The accounting fraud assignment examines that words of van Ruth et al., (2017) that corporate fraud is determined as unauthorised activities and illegal practices committed either by the company’s employees or else by the company in order to sustain a large percentage of profit. In the context, Halbouni et al., (2016), states that under the laws of Companies Act 2012, any such illegal practices can attract legal actions, penalties, or both. Besides, company can eventually deteriorates its reputation in the market. However, the percentage of corporate accounting and financial fraud is increasing in a dynamic manner making it an interesting topic to be discussed and investigated herein accounting fraud assignment. As opined by Peters and Maniam, (2016), corporate accounting and financial frauds are determined as deceiving activities, which drastically affects the financial position of the company.

Figure 1: Statistics showing increasing rate of corporate fraud

(Source: Peters and Maniam, 2016)

It has been observed by Harjoto, (2017), due to the establishment of diverse acts to omit increasing percentage of corporate fraud by the government, it has been an essentially necessary for the companies to incorporate with those policies or else they would be penalised.

Rationale of the research (Problem that the research seeks to solve and the reason for its importance)

There are different kinds of corporate accounting and financial fraud, like falsified accounting, leaking confidential information to the outsourced, legitimate business practices along with exchanges for disguising any illicit activities. However, the unauthorised practices of the management system, including segmentation of the duties in an inappropriate manner, leads to de-motivation among the employees. Corporate accounting and financial frauds usually occur owing to a number of motivational factors and, with advancements in technology, become all the more undetectable. Thus, a study developed within the accounting fraud assignment regarding the probable motivational factors driving corporate fraud as well as the strategies that can be taken up for the mitigation of the same is essential to be executed, in the current business scenario.

Outline for the structure of the proposal

Investigation has been done on the respective topic like corporate accounting and financial fraud in the context of accounting fraud assignment, what leads to encourage employees for committing such unauthorised practices along with the impacts of such activities. Besides, what steps and practices can be integrated by the management system to encourage and motivate employees to focus on the betterment of the company has been discussed.

Aim of the research

Aim of the present research on accounting fraud assignment is to investigate the factors of motivation for committing accounting and financial fraud along with the obtained prevention measures for controlling similar kinds of fraud within the corporate field.

4. Research questions and objectives

Research Questions on the case scenario of accounting fraud assignment:

- What is corporate accounting and financial fraud?

- What factors are known to motivate the employees to commit fraudulent behaviour?

- How does accounting and financial fraudulent behaviour impact an organisational performance?

- What measures seems to be effective for controlling fraud?

- What policies have been formulated by the Australian government regarding accounting and financial fraud prevention?

Research objectives:

- To explore the concept of corporate accounting and financial fraud

- To investigate the motivational factors of the employees and techniques used for commending accounting and financial fraud

- To evaluate the impact of fraudulent behaviour on organisational performance

- To examine the measures of controlling accounting and financial fraud

- To analyse the policies of Australian government for accounting and financial fraud prevention

5. Theoretical background/ Literature review

Introduction

According to Lee and Fargher, (2015), this section provides a survey for scholarly articles for a specific topic. This is known to provide an overview regarding the key findings along with concept development in accordance with the research questions and problem as well. Thus, the present section of accounting fraud assignment highlights a concrete and critical discussion about the particular topic through the help of several secondary sources such as scholarly articles; journals; business magazines; books and thesis as well.

Concept of Corporate fraud

According to Kakati and Goswami, (2019), corporate fraud is generally referred to as the activities that are undertaken through an organisation or rather any individual which seems to be performed in an illegal way and however, are designed for providing benefit for the organisation. The schemes of corporate fraud are found to go beyond a scope for a stated position of an employee along with being marked through the economic impact as well as complexity upon their business; other parties and employees as well. There are several types of fraudulent activities mentioned herein accounting fraud assignment that are practiced in the corporate field such as misrepresenting products and services; falsified accounting and similar others as well. Corporate fraud is often performed through the benefit for confidential information and access for sensitive assets regarding gain. This type of fraudulent behaviours is generally hidden beside the legitimate practices of business along with the exchanges for disguising any illicit activities.

As per different fraud activities, accounting records based on any organisation might be altered for presentation of an image associated with higher profits and revenue as compared with any financial results. As opined by Said et al., (2019), these types of actions can also be taken for hiding the shortcomings like slow revenue, net loss, hefty expenses and declining sales as well. This type of falsified accounting is generally performed for making an organisation much more attractive to potential investors and buyers. On the other hand, in the case of misinterpretation of any product and service, a company generally hides their flaws along with the defects. Besides investing within refurbishing; repairing and redesigning of any product, companies often are found to disguise the respective issues. This is usually performed when an organisation consists of controlled finance and budget as well.

Nature of fraud offences

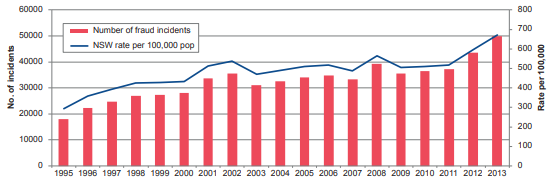

According to an Australian Bureau of Statistics survey, it has been evidenced for an increase within the reported fraud, which seems to be starting for acceleration. As per the views of Anindya and Adhariani, (2019), it can be stated within this accounting fraud assignment that there are certain types of frauds who has been known to the police which has been unlikely for representing an entire spectrum based on different fraud types. However, increasing personal victimisation of fraud within the Australians who has been aged above 15 years through 5.0 percent to 6.7 percent within the year of 2007 to 2011 has been observed in this section of accounting fraud assignment. Within this, the increase in rate of financial loss of the individuals has been evidenced, which has been driven through the rise in frauds for credit cards along with taking scams as well. On the other hand, the Australian payments clearing association is also known to found about the increase within fraudulent transaction of cards. This has increased up to 50% within 5 years.

Figure 2: Rate of Fraudulent activities

Source: (Astutiet al., 2019)

However, in some other countries such as Wales and England, there has been particular offence for fraud whereas the other jurisdictions consists several crime ranges which entails with the element for dishonesty. For instance, as stated by Astriana and Adhariani, (2019), there seems to be above 300 criminal offences which can be charged within the connection along with the acts of any dishonesty which is referred to as the key attribute which is known to distinguish any fraudulent through the innocent conduct. Fraud can be compared with an increase of technological advancements such as the increased use; additional challenges which are presented for attempting regarding the prevention for controlling the fraudulent activities.

Motivational factors and techniques leading to fraudulent activities in corporate area

Fraud seems to be a bigger deal for any kind of business. As per the result of association of certified fraud examiners, an average of the organisations are found to lose 5% based on its yearly revenues regarding fraudulent activities. Based on the views of Fidelis-Nwaefulu, (2019), internal fraud is considered to be something which must be kept in mind each and every time. While things go well, people never think anything about fraud which creates a good opportunity for based on several motivated people for committing fraud. It has been evidenced in the context of accounting fraud assignment that greed; need and vices are the prime factors for motivation within an organisation or an individual for fraudulent activities. These factors are interrelated together within a cycle and are also progressive through an activity to another activity as well.

Pressure for committing fraud

Employees going through stressful situations might view fraud as an easy process for elimination of the problems. Pressure might be caused due to other people as well. Pressure is able to force various human responses and at times might lead for an internal fraud as well. Stealing the funds of business seems to be common for a fraudulent activity however, other types of frauds that can be involved through pressure are internal theft for business property; claiming benefits which an employee is not entitled; and similar others. As evidenced by Muñiz, (2019), it can be stated herein accounting fraud assignment that an employee who endures for enough pressure might be driven for illegal activities whether this can be stealing of money along with abusing any internal systems as well.

Capabilities for committing fraud

As opined by Black, (2010), capability; rationalisation and attitude are found to different characteristics for becoming warning signs regarding fraud. Poor coordination within the top management of an organisation; lack within the internal control; weaker ethical culture; inadequate supervision and training along with ineffective programs of anti-fraud can lead to fraudulent activities within the corporate areas. Thus, there are six capabilities through which an organisation or individual can perform these types of illegal activities such as position of an individual in an organisation might create an opportunity for activities related to fraud. On the other hand, study of Malimage, (2019) also clarifies herein accounting fraud assignment that perfect individuals who consist of strong confidence and ego cannot be detected as fraud and seems to be smarter for exploiting the weakness of internal control along with using function; position along with an authorized access resulting in an advantage. However, successful fraudsters consist of the capability for coercing others to conceal any fraud and can also lie consistently as well as can deal well with their stress.

Techniques of corporate fraud

As per the views of APCA (2013), corporate accounting and financial fraud can result in being challenging for preventing and catching. Through the creation of effective policies, system checks along with balances as well as physical security, an organisation might limit an extent through which this activity can come up. This seems to be a white-collar crime. As per the techniques used for fraudulent activities, employees make use of asset misappropriation, which indicates the fraud schemes. For instance, check tampering where an employee can alter a payee along with the amount and similar other details for a check that tend to create unauthorized checks as well. The accounting fraud assignment also explores the readings of Pramana et al., (2019) that cash theft on the other hand are common within the retail industries which indicates cash exchanges which simply covers stealing of cash; returning fraud where employee seems to collude with other people for fraudulently returning the goods regarding any refund. Other than this, it also involves removal within the hard currency. However, an employee, for misusing the services of the company, also uses service theft.

Impact of fraudulent behaviour on organisational performance

Fraud scandals consists of the ability for creating incentives that can change managers within one attempt for improving the performance of an organisation; recovering the lost capital of reputation along with limiting the exposure of the organisation for liabilities which can be raised through fraud. However, it also seems to be possible for the revelation based on fraud creating incentives for changing of composition as per the organisational board, which leads to improvement of external monitoring performed by the managers. As opined by Shao, (2019), besides these types of claims, it is known to be systematic evidence, which has been suspected by an organisation through fraud, which consists of higher turnover within the directors and the senior managers. Nevertheless, as evidenced by Agrawal et al., (2019), it has also been evidenced in the context of accounting fraud assignment that the organisation, which commits fraud, comprises of higher directorial and managerial turnover.

On the other hand, it has been known that the top managers of organisations committing accounting and financial fraud can also lose their positions and jobs. Therefore, fraud might cause failure within an organisation along with the relationship within the customers and the organisations. An increase within fraud through employees can impact the operations which can in turn, leads to the opportunities of cost for lower sales; capital as well as the decrease within the employee morale.

Measures taken by the organisations for controlling fraud

As per the views of Sagar, (2019), “Control frauds” are known to be the legitimate entities that are controlled through the people, which can use them as a weapon of fraud. On the other hand, most of the organisations are found to make use of whistle blowing for detecting fraudulent activities. For providing effective whistle blowing system, it has been expected about the organisations, which can provide the employees along with a higher level of a disclosure as per the respective process. This has been termed as a measure for the implementation of this process. According to Cronin, (2018), this particular process examined herein accounting fraud assignment is also known to associate positively with the anonymous reporting as well as organisational support with the help of external directors upon the shareholdings and audit committee as well.

However, establishment and an effective maintenance of internal control can result in specific designing for detection and prevention of fraud. Nevertheless, adoption for code of ethics regarding the employees and the management can also be efficient for controlling these types of behaviours or rather activities. According to Spink et al., (2019), implementation of an employee reporting system like anonymous hotline can also be helpful for a workplace as per controlling measures of fraudulent activities and can also uncover fraud as well.

Policies for fraud prevention taken by the Australian government

According to the Australian government, for controlling fraudulent behaviour through the fraud control plan for dealing with certain identified risks. This seems to be significant for the plans of fraud control for emphasizing upon prevention and these are generally encouraged for being available as well as accessible regarding the officials. This plan is able to integrate through the strategic planning of an organisation and can also be encouraged for being made for the areas regarding a higher risk into an entity. This plan can also be documented as per the approach for controlling the fraudulent activities for operational; strategic along with a tactical level as well as encompassing the awareness for investigation of the measures leading to prevention.

However, as stated by Garbowski et al., (2019), Australia also focuses upon a commonwealth fraud-control framework, which outlines the requirements of Australian government. This involves the requirements as per the government entities, which consists of fraud control program, whichcan cover detection, prevention, reporting and investigation strategies. The instance covered in this section of accounting fraud assignment signifies that accounting and financial fraud rule highlights section 10 for public performance; governance as well as accountability rule as well which seems to be the legislative instrument, which helps in binding with the commonwealth entities that sets out with key requirements regarding the fraud control. On the other hand, as opposed by Ramos Montesdeocaet al., (2019), public governance; performance and accountability act 2013 seems to be the key for legislation that underpins the financial framework of Australian government. This is generally known to be associated with the guidance and policies that tend to set out regulatory framework regarding the accurate use as well as management for the public resources through the entities of commonwealth.

Literature gap

As per the above literature illustrated within this accounting fraud assignment, discussion has been conducted through secondary resources which consists of several gaps and loopholes based on the specific topic like reasons for commending fraud by the employees; risk factors related to corporate fraud; financial fraud and similar others has not been covered within the above discussion. Hence, not considering these factors has created a gap within the discussion, which has also created an opportunity for future research as well.

Summary

As per the summarization of the present section on accounting fraud assignment, it has covered a concrete literature regarding the concerned topic. Concept of fraudulent behaviour along with the policies undertaken by Australian government for prevention of these fraud activities within the corporate field has been analysed and the measures for controlling fraud has also been evaluated. However, the impact of fraudulent behaviour along with the techniques used for performing these activities has also been highlighted in the present section.

6. Research design and Methodology

Research design

According to Mora et al., (2019), research design is referred to as the framework for methods as well as techniques that are chosen by a researcher for combination of different components based on a research through a logical and reasonable manner for handling the research problem in an efficient manner. This is known to provide insights regarding the way for conducting a research with the use of any specific methodology. Three types of research design is known to exist such as exploratory, descriptive and causal. For the present research on accounting fraud assignment, the use of descriptive research design will be most appropriate as it helps in describing the characteristics based on the phenomenon and population.

Research approach

Based on the views of Hoddy, (2019), research approach is identified as a procedure along with a plan, which comprises of certain steps based on broader assumptions for detailed method regarding data gathering; interpretation and its analysis as well. This depends upon the nature for the analysed problem of the research. Hence, there are several research approaches such as quantitative, qualitative and mixed approach. For the present research on accounting fraud assignment, the use of mixed approach will be considered as mixed methods are generally useful within the understanding of contradictions between the qualitative findings as well as quantitative results as well. This method provides a voice for the study participants along with ensuring the findings of the study which has been grounded for the experiences of the participants.

Type of data

As evidenced by Newman and Gough, (2019), the process of data gathering is referred to as the measurement of information upon the variables of interest within the established systematic fashion, which helps in enabling one for answering the stated questions of research; evaluating outcomes and testing the hypothesis as well. Hence, for the present study provided in the accounting fraud assignment, the researcher will consider the use of both primary and secondary data. Primary data gathering seems to be a process for collecting the data through surveys; experiments and interviews. On the other hand, secondary data are referred to as the information which is collected through secondary resources such as journals, articles or newspapers and similar others.

Data collection technique

The topic is very uncommon and hence the data and relevant information has been collected using mixed methods. According to Nawawi and Salin, (2018), mixed methods are a method that includes both primary and secondary methods of collecting data. In the matter of primary method, online survey for all those associated with the corporate sectors will be conducted. In contrast, adequate support from the secondary sources that includes collecting information from the latest published journal and articles has been considered. The topic corporate fraud examined in the context of accounting fraud assignment is a wider concept and hence to portray the concept in an appropriate manner, mixed method is considered as most suitable.

Population and sampling

As opined by, (2017), sampling techniques is a concept that indulge diverse methods that can be integrated by the researcher to conduct their research for sustaining relevant finding. There are two kinds of sampling techniques. While conducting the research on the following topics of corporate frauds conducted by the employees and companies as well to sustain profit through illegal practices, both probability sampling techniques along with the non-probability sampling technique would be considered. Probability sampling technique will be used during the time of conducting online surveys in which 100 individuals associated with the corporate sectors can participants and review their evaluation. Besides, non-probability sampling technique will be considered for the secondary research, which includes thematic analysis, as the research would be selecting the relevant sources to sustain information.

Process of data analysis

For conducted the given research on accounting fraud assignment combination of both primary and secondary methods under the mixed methods of collecting data has been collaborated. Quantitative data analysis under the primary methods for online surveying the 100 candidates associated with corporation will be conducted. Besides, thematic analysis under the secondary aspects of collecting data will be conducted.

Ethical concern

As opined by et al., (2017), it is necessary to consider the following ethical consideration while conducting the research or else the information collected would fail in maintaining credibility and reliability of the research. For the following topic examined in the segments of accounting fraud assignment, the researcher will integrate with the Data Protection Act 1998, in which no information of the respondents will be leaked or discussed to any outsider. Integrity and autonomy will be maintained which will determine that the candidates are free to leave the survey as per their will. Besides, authenticity will be followed that states that the information collected from the online survey will be handled and accessed only by the authorised person. Justice will be maintained throughout the research on accounting fraud assignment by asking all the participants the same question and treating them all alike, with importance. Confidentiality of information will be maintained by storing the data related to research in password-protected systems and ensuring no person without authority is able to avail the same.

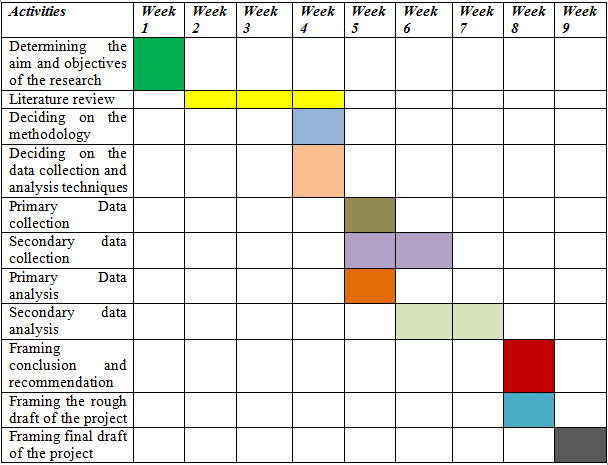

Fig: Timeline of the research

(Source: Developed by the learner)

7. References

Agrawal, A., Jaffe, J.F. and Karpoff, J.M., 1999. Management turnover and governance changes following the revelation of fraud. Accounting fraud assignment The Journal of Law and Economics, 42(S1), pp.309-342.

Anindya, J.R. & Adhariani, D., 2019. Fraud risk factors and tendency to commit fraud: analysis of employees’ perceptions. International Journal of Ethics and Systems, 35(4), pp.545–557. Available at: http://dx.doi.org/10.1108/ijoes-03-2019-0057.

APCA, 2013.Explanation of Cheque Fraud Categories.Payment Fraud Statistics.APCA.

Astriana, D.V. and Adhariani, D., 2019, July. Investigating Employees’ Views on Fraud Awareness and Anti-Fraud Strategy. In Asia Pacific Business and Economics Conference (APBEC 2018).Atlantis Press.

Astuti, S., Marita, M. and Heriningsih, S., 2019. Analysis Factor Triggers Fraud And Corporate Governance On Indications of Fraudulent Financial Reporting Using the Pentagon Fraud Theory Approach. Eksis: JurnalRisetEkonomidanBisnis, 14(1), pp.47-54.

Black, W. K. 2010. Epidemics of “Control Fraud” lead to Recurrent, Intensifying Bubbles and Crises, working paper, University of Missouri-Kansas City, SSRN-id 1590447.

Buccirossi, P., Immordino, G. & Spagnolo, G., 2017. Whistleblower Rewards, False Reports, and Corporate Fraud. SSRN Electronic Journal. Available at: http://dx.doi.org/10.2139/ssrn.2993776.

Shao, S., 2016. What are Some Best Practices for Internal Controls to Prevent Occupational Fraud in Small Businesses? Available at: http://dx.doi.org/10.15760/honors.306.

Fidelis-Nwaefulu, M., 2019. Tax Practitioners’ Perceptions Regarding Fraudulent Earned Income Tax Credit Claims accounting fraud assignment (Doctoral dissertation, University of Phoenix).

Riccardi, L., 2015. Accounting Standards for Business Enterprises No. 38—Initial Implementation of Accounting Standards for Enterprises. China Accounting Standards, pp.299–305. Accounting fraud assignment Available at: http://dx.doi.org/10.1007/978-981-10-0006-5_42.

Halbouni, S.S., Obeid, N. & Garbou, A., 2016. Corporate governance and information technology in fraud prevention and detection. Managerial Auditing Journal, 31(6/7), pp.589–628. Available at: http://dx.doi.org/10.1108/maj-02-2015-1163.

Harjoto, M.A., 2017. Corporate social responsibility and corporate fraud. Social Responsibility Journal, 13(4), pp.762–779. Available at: http://dx.doi.org/10.1108/srj-09-2016-0166.

Hoddy, E.T., 2019. Critical realism in empirical research: employing techniques from grounded theory methodology. International Journal of Social Research Methodology, 22(1), pp.111-124.

Kakati, S. and Goswami, C., 2019. FACTORS AND MOTIVATION OF FRAUD IN THE CORPORATE SECTOR: A LITERATURE REVIEW. Journal of Commerce & Accounting Research, 8(3).

Lee, G. and Fargher, N., 2013. Companies’ use of whistle-blowing to detect fraud: An examination of corporate whistle-blowing policies. Journal of business ethics, 114(2), pp.283-295.

Malimage, K., 2019. Application of Underutilized Theories in Fraud Research: Suggestions for Future Research. Journal of Forensic and Investigative Accounting, 11(1).

Mora, L., Deakin, M., Reid, A. and Angelidou, M., 2019. How to overcome the dichotomous nature of smart city research: proposed methodology and results of a pilot study. Journal of Urban Technology, 26(2), pp.89-128.

Muñiz, J., 2019. Transformational Study of High-Net-Worth Individuals' Rationalizations, in the Absence of Need, when Committing Fraud (Doctoral dissertation, Northcentral University).

Nawawi, A. & Salin, A.S.A.P., 2018. Employee fraud and misconduct: empirical evidence from a telecommunication company. Accounting fraud assignment Information and Computer Security, 26(1), pp.129–144. Available at: http://dx.doi.org/10.1108/ics-07-2017-0046.

Newman, M. and Gough, D., 2019. Systematic Reviews in Educational Research: Methodology, Perspectives and Application. Accounting fraud assignment In Systematic Reviews in Educational Research (pp. 3-22).Springer VS, Wiesbaden.

Cronin, A., 2018. Concluding thoughts: corporate fraud and the way forward. Corporate Criminality and Liability for Fraud, pp.164–176. Available at: http://dx.doi.org/10.4324/9781315179605-8.

Peters, S. and Maniam, B., 2016. Corporate fraud and employee theft: Impacts and costs on business. Journal of Business and Behavioral Sciences, 28(2), p.104.

Pramana, Y., Suprasto, H.B., Putri, I.G.A.M.D. and Budiasih, I.G.A.N., 2019. Fraud factors of financial statements on construction industry in Indonesia stock exchange. International journal of social sciences and humanities, 3(2), pp.187-196.

Ramos Montesdeoca, M., Sánchez Medina, A.J. and Blázquez Santana, F., 2019. Research Topics in Accounting Fraud in the 21st Century: A State of the Art. Sustainability, 11(6), p.1570.

Sagar, A., 2019. The Concept of White-Collar Crime: Nature, Causes, Political and Legal Aspects in Accountability and Way Forward. Journal of Political Studies, 26(1).

Said, J., Asry, S., Rafidi, M., Obaid, R.R. and Alam, M.M., 2019. Integrating Religiosity into Fraud Triangle Theory: Empirical Findings from Enforcement Officers. Available at: http://dx.doi.org/10.31235/osf.io/wcyg4.

Spink, J., Chen, W., Zhang, G. and Speier-Pero, C., 2019. Introducing the food fraud prevention cycle (FFPC): A dynamic information management and strategic roadmap. Accounting fraud assignment Food Control, 105, pp.233-241.

van Ruth, S.M., Huisman, W. and Luning, P.A., 2017. Food fraud vulnerability and its key factors.Trends in Food Science & Technology, 67, pp.70-75.

8. Appendix

|

Student Details |

||

|

Name |

: |

|

|

Student Number |

: |

|

|

|

: |

|

|

Subject (Code/Name) |

: |

|

|

Supervisor Details |

||

|

Name |

: |

|

|

|

: |

|

|

Proposed Research Details: |

|

Topic: |

|

Summary of the proposed research project, including brief description of methodology. For conducting the respective research, both primary and secondary method under the mixed methods of collecting data will be conducted. Quantitative analysis under primary method along with thematic analysis under secondary methods will be considered. |

|

Ethics Checlist (Participants) |

|

How do you propose to select your participants? Online portal will be used that can be accessed by 100 candidates associated with corporate sectors. Hence, candidates from the age of 20-55 are allowed for the survey. |

|

Will your research on accounting fraud assignment involve adults who might be identified by you or anyone else reading the research? (Yes/No). If yes, how will you obtain their consent? No, no one’s identity will be disclosed |

|

Does your research involve children under eighteen years old? (Yes/No) No |

|

Ethics Checlist (Participants) |

|

Will your research on accounting fraud assignment take place in an institution? (Yes/No) NO |

|

Are in a position of power over participants? (Yes/No), if yes, describe any ethical implication and how you deal with them No |

|

Describe any risk or harm to participants which might be associated with yoru research and how would you propose to minimise these risks No risk and harm will be rendered as necessary ethical consideration will be followed by the researcher while conducting the research |

|

Privacy and Confidentiality |

|

How will you protect the confidentiality and privacy of your participants? By following Data Protection Act 1998 |

|

Will it be possible to identify participants from published data? (Yes/No), if yes, is there any ethical issue which may arise from such identification. NO |

|

Data Collection and Storage |

|

Who will have access to the data? Information collected will be assembled only by the authorized person. |

|

How will you store the data in order to ensure its security Technical hardware like pen drives will be used to ensures the information |