Accounting Assignment: Contemporary Issues at Commonwealth Bank of Australia

Question

Task: This accounting assignment covers the application of contemporary theoretical accounting concepts and accounting theories on various organisational issues or contexts identified related to a corporation of your choice.

Task Details: To complete this assignment task, you need to choose a company from the ASX listed in Top100 and critically analyse the application of Accounting Theories and concepts.

In your analysis you need to demonstrate strong understanding of accounting theories and theoretical concepts by applying them onto the current circumstances, initiatives, and issues of your chosen company. Students are required to prepare a comprehensive report directed at their chosen company detailing a critical analysis of the application of accounting theories and effectiveness of the company to meet its obligation of conceptual framework of accounting.

Answer

Background of accounting assignment

Financial accounting is defined as the procedure of recording, summarizing and reporting of financial transactions undertaken by the business resulting from the business operations over the period. The financial transactions are summarised for preparing the financial statements that involves balance sheet, income statement and the cash flow statement for recording the operating performance over the specific period (Thompson, 2018). In this report, the contemporary issues in accounting and accounting theory related to Commonwealth Bank of Australia is studied. It shows the issues currently faced by the company and how it undertakes to prepare its financial report using the accounting framework.

Contemporary issues in Accounting and Accounting theory

In the present era of modern accounting, it is pervasive in nature which is generally classified as personal finance and business finance. In both the cases, there are certain contemporary issues that has become biased and unethical to deviate from the ideal attributes and neutral decision making of the accounting process. These contemporary issues are faced by Commonwealth Bank for manifesting its generalised aspects in terms of social, cultural and political nature of principles of accounting (Byrneand Lees, 2018). The cultural biasness is determined as the primary culture of accounting is to report and monitor the financial transactions and other relevant accounting details as well as business transactions. In this regard, there are specific contemporary issues raised in the ideal culture of the accounting equation especially on the perception of the people who are involved in maintaining the principles of transparency and accuracy in the accounting study.

Conceptual Framework of FRS

The conceptual framework for financial reporting is a body of interrelated objectives and fundamentals (Al-Dmouret al., 2018). The aim of the conceptual framework is to identify the objectives and purpose of financial reporting as well as the fundamental underlying the concepts to help the business in achieving the organisational objectives. Commonwealth Bank of Australia has prepared its financial report for the FY 2020-21 as the general purpose financial report. All the financial statements of the company have been prepared in accordance with the interpretations of Australian Accounting that is adopted by the AASB and the IFRS which are issued by the IASB. The basis of accounting used in preparing the annual report of CommBank is in accordance with the requirements underlined in the Corporations Act 2001. The financial statement of the entity is prepared on the basis of Australian dollars or A$, which is regarded as the functional and presentation currency of the entity with all the values rounded to the nearest $ in millions with regards to the ASIC Corporations Instruments 2016/191 (CommBank, 2021). The conceptual framework prescribes the inclusion of transactions relating to foreign currency within the annual report that are converted into the functional currency using the prevailing market exchange rate on the date of the transactions. The AASB governs the financial reporting system of CommBank to be prepared as a going concern basis using the historical cost basis and eliminate few of the assets and liabilities like derivatives and stock market instruments which are measured according to the fair value.

(Source: Oshoand Ayorinde, 2018)

Accounting Theories

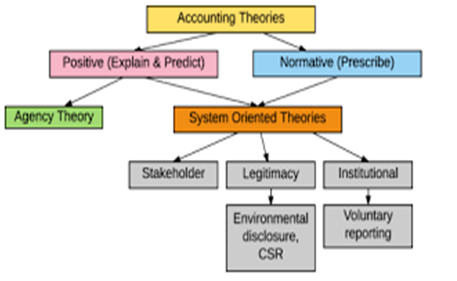

Normative accounting theory seeks to provide a basis of accounting measurement specifying about the accounting procedures and the contents available in the financial report. The normative accounting theory commences with a theory and deduce down to specific policies established from the theory by making it the best option for assuming the future financial sustainability of the business and advising on how to plan for the future events (Stolowyand Paugam, 2018). On the other hand, positive accounting theory emerged in the late 1960s as a process that seeks to use the understanding, knowledge and ability of accounting policies that are most suitable in dealing with the present conditions in the future. Positive accounting theory is more practice and based on the current events, whereas normative accounting theory is a theoretical approach that ensures evolving of accounting practices on a daily basis and does not diverge from the suitable economic concepts.

(Source: Mormann, 2021)

CBA has opted for positive accounting theory or “practical approach” that hunts for the current banking practices prevailing in the Australian Banking industry and its cold and hard statistics (CommBank, 2021). This approach is used by the CBA financial managers in bookkeeping and collecting financial data. The positive accounting theory thereafterscrutinises the actual banking transaction of the CommBank and compares the inflow and outflow of cash to equate any kind of discrepancies (Hanet al., 2018). The positive accounting approach is used by the accountants of CBA to verify the cash flow position of the entity through matching the cash inflow and outflow. This theory provides the accountants a framework for CommBank to predict how the company shall record its transactions as a going concern. Theoretically, CBA is viewed as an entity inclusive of the total contracts entered by the business (CommBank, 2021). The positive accounting theory posits that the Australian banking company fundamentally operates in relation to the contracts that dictate the business operations as the core driver for maintaining company success as efficiency. This requires minimising the costs of the contracts for unlocking the most value extracted from the business operations.

Capital Markets Research and its impact for Accounting

The capital market research in accounting is a research-based phenomenon that investigates the connection between the accounting information and the key capital market variables like the share price of the company, the rate of return on shares for years and the systematic risks. Accounting is essential for capital markets as financial information is required by the investors for making decisions about investments and therefore, high quality accounting standards are critical (Consoni et al., 2017). Accurate and useful financial information helps in the creation of suitable capital formation environment that sprouts for growth. The capital market performance of CommBank is predicted from its Cash NPAT which is recorded as $922 million in FY 2021 as compared to FY2020 as $633 million (CommBank, 2021). The Institutional Banking and Markets 9IB&M) business segment of CommBank serves as the commercial and wholesale banking entity for large corporate, government clients and institutional agents across a wide range of financial services solutions. It involves accessibility of debt capital markets, transaction banking, working capital and risk management through dedicated product and industry specialists. The company is listed in ASX and regularly trades in the stock markets using a variety of stock market instruments. The capital market operations for CBA deals with channelizing the savings and investments between the suppliers and borrowers of capital to be used for lending and investing purposes (CommBank, 2021). The suppliers of capital markets are usually the banks like CBA, whereas the investors are the people who seek capital to be used for business growth, government and individuals.

Earnings Management and Quality

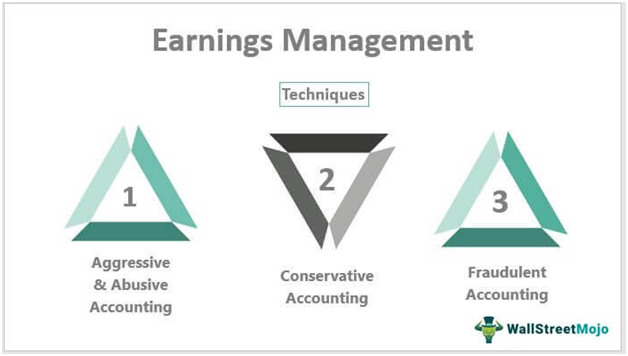

Earning Management is defined as the use of a large variety of accounting techniques that produces financial statements which can present an overly positive view about the business activities and financial position of the entity. Most of the accounting rules and regulations require the management of the company to make judgement based on these principles. There are two types of earnings management and quality- adjusting the individual accounting policies and using the different accrual methods (Moratisand van Egmond, 2018). CommBank withheld itself from using earnings management and prefers depicting the actual financial health to its stakeholders rather than misinterpreted version of the financial report. CommBank does not initiate itself into activities like misrepresenting the share prices of the company, usually by increasing or decreasing the same once the announcement is made from the end of the business (CommBank, 2021). Such earnings management practices are undertaken to meet the earnings forecasts on behalf of the business which has failed. The management tries its best to influence the accounting practices by meeting the earnings estimates and holding up the share prices. The most common strategies implemented by businesses are earnings-focused decisions, biased accounting judgments and altering accounting principles. The decisions to carry out earnings management strategies are carried out by the management to focus on the meeting the earnings estimates. Some activities - such as research, advertising or employee training - may be suspended. The company will stop these activities for a short period of time, provided that the business develops better in the future, and the suspended activities can be resumed thereafter. However, in well-positioned companies, management focuses on the company's long-term success and usually does not resort to artificial profit increases.

(Source: Sanadet al., 2019)

Recommendation and Conclusion

It is recommended that the accounting principles must be re-designed and implemented for maintaining objective, transparency, critical and accurate assessment of the financial events and transactions for the business operations. It shall thereby help in securing the purpose of attaining the effective financial management. This shall be used for monitoring and evaluating critically the relevant changes and its related effects to the present business conditions and enabling to make a concerned managerial impact for making decisions about the most suitable accounting approach towards developing the accounting procedures for the banking company. However, the practical implications of the accounting concepts address the biasness and disparities that raises the concerns of the investors towards the true and fair view of the financial report presented by the business. It is mainly due to the fact of human factors on the given case.

Reference List

2021 Annual Report - CommBank. (2021). Retrieved 9 December 2021, from https://www.commbank.com.au/about-us/investors/annual-reports/annual-report-2021.html

Al-Damour, A., Abboud, M. and Al-Balqa, N., 2018.The impact of the quality of financial reporting on non-financial business performance and the role of organizations demographic attributes (type, size and experience).

Byrne, D. and Lees, D., 2018. Finance and Accounting—Beyond the Numbers with Self-Leadership. In Contemporary Issues in Accounting (pp. 167-186). Palgrave Macmillan, Cham.

Consoni, S., Colauto, R.D. and Lima, G.A.S.F.D., 2017. Voluntary disclosure and earnings management: evidence from the Brazilian capital market. Revista Contabilidade & Finanças, 28, pp.249-263.

Han, J., He, J., Pan, Z. and Shi, J., 2018. Twenty years of accounting and finance research on the Chinese capital market. Abacus, 54(4), pp.576-599.

Moratis, L. and van Egmond, M., 2018. Concealing social responsibility? Investigating the relationship between CSR, earnings management and the effect of industry through quantitative analysis. Accounting assignmentInternational Journal of Corporate Social Responsibility, 3(1), pp.1-13.

Mormann, F., 2021. Beyond Algorithms: Toward a Normative Theory of Automated Regulation. BCL Rev., 62, p.1.

Osho, A.E. and Ayorinde, F.M., 2018. The General Tenets of Positive Accounting Theory Towards Accounting Practice and Disclosure in Corporate Organizations in Nigeria. Journal of Economics and Sustainable Development ISSN, pp.2222-1700.

Sanad, Z., Shiwakoti, R. and Kukreja, G., 2019. The Role of corporate governance in mitigating real earnings management: Literature review. KnE Social Sciences, pp.173-187.

Stolowy, H. and Paugam, L., 2018. The expansion of non-financial reporting: an exploratory study. Accounting and Business Research, 48(5), pp.525-548.

Thompson, D., 2018. Contemporary challenges in audit.In Contemporary issues in accounting (pp. 125-143). Palgrave Macmillan, Cham.